![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

Kyle Cox, Investment Analyst, EMEA

Dan Kemp, Chief Investment Officer, EMEA

Key Takeaways

With the Trump administration starting a purported trade war with China on July 5, questions have

grown into fears over how tariffs may affect the global economy. However, we offer a more nuanced

response to the question, posed in the title, which is on many investors’ minds today: We do think U.S.

stocks are overpriced now and believe selling overpriced assets is a good discipline. But selling should

not be driven by fears, macro events, and the like. In fact, over the long run, investors usually perform

better when they ignore these market tremors and stay focused on their financial goals.

A Nasty Trade War Is Possible, But How Likely?

Investors seem spooked by the recently announced tariffs and the possibility that all of this may lead to

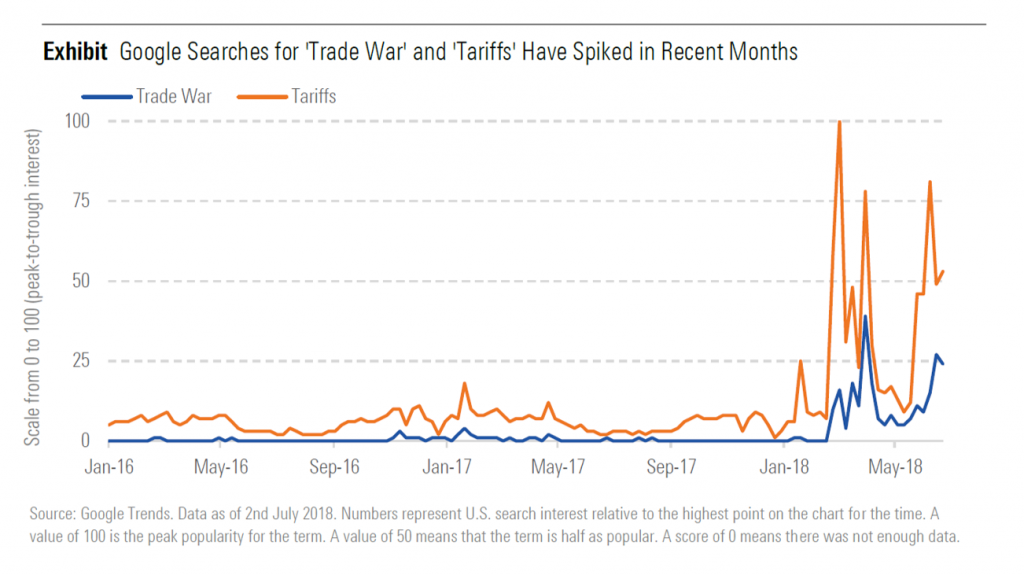

an ugly trade war. The subject has clearly grabbed attention and headlines. As illustrated in the exhibit

below, Google searches in the U.S. for “trade war” and “tariffs” spiked in recent months as the Trump

administration began an effort to renegotiate terms with its trade partners, starting with tariffs on steel

and aluminum announced in March. That move was aimed at China, but also impacted many other

countries.

Unsurprisingly, China prepared countermeasures by proposing tariffs on imports of American soybeans,

sending commodity prices tumbling. Mexico and Canada faced challenges as the U.S. administration

sought to renegotiate the North American Free Trade Agreement. European countries confronted the

U.S. over tariff threats on autos. Retaliatory measures from all sides raised the probability of an

extended conflict that may hamper global economic growth.

We don’t believe that the announced tariffs present a major threat to global economies. The proposed

tariffs are significant and would affect 23% of U.S. imports, primarily hitting auto imports. However, we

believe the U.S. economy, in particular, is large enough and domestically oriented enough to not feel too

much pain from current measures.

Of course, trade tensions and tariffs could become more severe and, at worst, tip the global economy

toward a recession. But getting too focused on a worst-case scenario ignores the possibility that

tensions cool, compromise is reached, and investors go back to focusing on strong earnings. It wasn’t

too long ago that presumed nuclear conflict on the Korean peninsula sent tremors through global

markets, but that seems to have been laid to rest for now.

Should Investors React?

The short answer: no. We focus on long-term valuations—the true and durable value of an asset class,

rather than its market price. Having a long-term perspective makes the next turn in the trade spat less

concerning to us. Instead, we ask, “How might this affect fundamentals over the next several years?”

Investors who trade on emotion and market reactions are more likely to sell when markets are low and

buy when they’re high. We seek to do the opposite, in part by sticking to our principled approach to

investing, which is designed to keep us rational in a sometimes irrational world.

Because we’re defensive now, we are prepared to be buyers if this or other concerns provide an

attractive buying opportunity. That point isn’t here yet. The effects of trade-war fears on U.S. stocks

have been minimal to date, with the post-crisis rally still up 15.3% on average for each of the last eight

years.

This long bull run has made U.S. stocks pricey, we believe, so we’re expecting below-average returns

from U.S. stocks over the next five to 10 years. But that does not mean we would ever sell stocks—or

any asset—based solely on newspaper headlines, the macro view, or fears. In fact, if anything, fearbased

price declines alert us to possible buying opportunities.

What Should Investors Do About Macro Events?

Perhaps the easiest thing to do is to do nothing. Ignore the headlines and stay focused on the long term.

But really the best investment advice is saving advice: develop a plan to reach your financial goals, then

stick to it. When you get an itch to do something different, try saving more—that’s probably the best

move to improve the chances of an investor reaching their goals.

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.