Should your client’s financial knowledge and experience drive risk strategy?

How financial advisers can leverage a client’s sophistication to enhance engagement.

By Nicki Potts, Director of Financial Profiling, and Ryan O. Murphy, Global Head of Behavioural Insights

Global regulatory frameworks stress the importance of incorporating clients’ financial knowledge and investing experience into the advice process, yet research exploring the complex interplay between these constructs, risk tolerance, and risk-taking behavior is limited. Our latest research examines the influence of the factors associated with financial risk tolerance on the portfolio allocation decisions of a globally diverse sample of 1,334 investors. Participants were asked about their financial risk tolerance, experience, knowledge, and cognitive reflection. Portfolio allocation data were also collected at the time of survey completion between February and May 2023 to determine the actual investment risk level of participant portfolios.

We found that the specificity of knowledge and experience matters in risk preferences, and that using a robust risk tolerance measure alone can adequately capture the effect of knowledge and experience in financial decision-making. Does this suggest that knowledge and experience are merely redundant in the risk profiling and advice process?

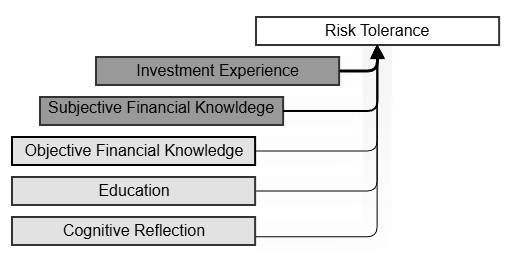

Experience and Confidence Are Key Drivers of Risk Tolerance

Investing experience and financial knowledge are generally linked to positive financial behaviors, such as higher saving rates, market participation, and better debt management, leading to more informed investment decisions. Individuals with more experience and knowledge are also more likely to have higher risk tolerance and hold more risky assets. However, the domain of knowledge and experience matters. We found that broad factual knowledge alone, such as traditional education, general cognitive ability, and, to a lesser extent, general financial literacy, while useful in helping individuals conceptualize financial decisions, is less effective in helping them engage with the specific demands of financial decisions despite their analytical skills.

On the other hand, direct stock and mutual fund experience and subjective financial knowledge (self-evaluations), which are closely associated with perceived financial decision-making confidence, are shown to have the greatest influence on risk tolerance. These factors are directly related to the cognitive and emotional aspects of financial decision-making. It turns out these factors are more related than general traits such as cognitive ability or education, thus making them better predictors of financial risk tolerance. The emerging research on the importance of subjective financial knowledge, and its mediating relationship with investing experience, suggests that confidence can assist individuals in navigating complex financial situations, even when their objective knowledge is lacking, and that enhancing investing experience can further support the effect of confidence on risk tolerance.’

Practically, this means that interventions aiming to enhance risk-taking behavior may be more effective by combining opportunities for experiential learning with traditional structured learnings. For example, the use of gamified virtual portfolios to stimulate market movements might allow investors to develop a better understanding of risk and composure, increase their familiarization with the stock market, and boost their confidence. Similarly, starting new investors with a small “learning portfolio” allows them to consolidate passive learnings with firsthand experience and develop the emotional discipline that is required when real money is at stake.

Integrating Robust Risk Measures With Personalized, Context-Sensitive Advising Strategies

In our analysis, risk tolerance, when measured using a robust tool, emerged as the primary predictor of study participants’ actual allocation to risky assets, further highlighting the predictive effectiveness of closely aligned factors. That said, while the impact of knowledge and experience on risky asset preference appears to be limited once risk tolerance is accounted for, it would be imprudent for advisers to overlook the role of knowledge and experience in personalizing client engagement and advice strategy.

Advisers who adapt communication style, product offerings, and guidance strategies to the client’s level of knowledge and experience can foster greater understanding and trust in the adviser-client relationship, enhancing confidence in the advice process and investment journey. Simple changes like using more qualitative and affective framing (descriptive and context-based narratives rather than precise statistics and probabilities) and focusing on investing principles rather than products may better serve those just starting on their investing journey to better evaluate risk and rewards.

Further, clients with limited knowledge or experience may benefit from starting discussions and their investment journey with less complex financial products that better align with their knowledge and experience without necessarily altering their investment risk strategies. A suitable plan that aligns with the client’s risk tolerance and capacity, and financial goals, comes first in the investment guidance process. Then, the composition of the investments selected for implementation can be fine-tuned to the client’s level of experience and knowledge. This hierarchical approach is sensible and consistent with existing know-your-client and suitability obligations.

As financial decision-making grows more complex, the future of effective advice lies in distinguishing between what determines risk preferences and what enables clients to live with market volatility. Risk tolerance remains the most reliable predictor of risky asset ownership, but experience and confidence shape how clients perceive and interpret volatility, uncertainty, and advice itself. By prioritizing rigorous risk profiling while deliberately cultivating experience and confidence through personalized engagement, advisers can bridge the gap between optimal portfolio design and sustainable investor behavior. In doing so, they move beyond compliance-driven profiling toward advice that is both empirically grounded and retains the human touch.