Even Advisers Aren’t Immune to Overconfidence Bias

By Samantha Lamas, Behavioural Researcher

We are all constantly making predictions about our lives, both professionally and personally. For financial professionals, predictions can have a drastic impact on a client’s financial success. This tends to show its prevalence during the so-called outlook season, when industry figures share their forecasts for the year ahead.

The overconfidence bias is just one of the many biases we face, but it can be especially difficult to accept. No one likes to hear that they are overconfident, let alone someone who has spent years building up their expertise. But when professionals open up to the idea that overconfidence bias can impact their business, it may help them better serve their clients and avoid the well-known traps that trip people up as they grapple with persistent uncertainty.

Defining Overconfidence Bias

Many people are familiar with a classic study of overconfidence that finds that the vast majority of people think they are above average in terms of their driving skills, but overconfidence also shows up in many other aspects of life.

Overestimation—People think they are more skillful than they actually are.

The better-than-average effect—People think they are superior to most others in a reference group.

Miscalibration—People are more confident in their judgments and predictions than they should be given their accuracy.

Although all forms of overconfidence are pertinent for financial professionals, miscalibration can be especially harmful. Financial professionals are often asked to predict the future—What is this fund going to do next? What about interest rates or the economy?—and, usually, a lot is riding on those judgments and predictions. Given the stakes, it is important for professionals to not only make accurate judgments but also to understand the justifiable degrees of confidence in their judgments. Unfortunately, research shows that many financial professionals, like experts from many fields, suffer from varying levels of miscalibration and overconfidence.

Among the dark clouds, there is a silver lining in making appropriate and responsible predictions for a living. Meteorology is one profession identified as being by and large well-calibrated in this regard. The success of meteorologists doesn’t imply they are omniscient or perfectly accurate; instead, it means that, for example, when a weather forecaster says she is 70% sure of the weather tomorrow, there is actually a 70% chance she is right. Good calibration is about properly understanding the limits of what one knows and being able to consistently identify when high confidence is warranted and, conversely, when humility is necessary.

Predicting the Weather vs. Predicting the Markets

Just like financial professionals, meteorologists undergo rigorous training to prepare for their role. However, meteorologists face a very different environment compared with financial professionals. When it comes to predicting the weather, past data can be reliable (to some extent) in predicting the future, and quick feedback is available.

The financial markets, on the other hand, aren’t as easily predictable nor as easy to learn. When it comes to investments, past performance does not necessarily predict future performance. Many forecasts take long time spans to unfold, some forecasts can influence market behaviors, and massive price swings can come from the most unexpected of places (remember GameStop?).

Regardless of the environment, there are still adaptable techniques financial professionals can use to combat overconfidence bias.

How to Combat Overconfidence Bias

Here are six steps you can take to be better calibrated and avoid overconfidence bias:

1) Establish deep domain knowledge.

Any good prediction must start with the right information and knowing what to pay attention to (and just as important, what information to ignore).

2) Adopt the right mindset.

The best forecasters view their “beliefs as hypotheses to be tested, not treasures to be guarded.” Adopting a how-might-I-be-wrong mindset can act as a buffer against overconfidence. It may be helpful to engage in a “what if” exercise where you consider what evidence it would take for you to change your mind and make a substantially different forecast.

3) Think in ranges (and bets): Define confidence level and range of outcomes.

Some predictions are amenable to using ranges. For example, consider the phrase “I am 90% confident that the price of XYZ will be between $18 to $21 per share at the end of the second quarter.” Notice how this prediction avoids fuzzy phrases like “strong possibility” or “real chance” and the forecaster pins herself to being 90% sure and using a range of values to express her confidence—also known as a confidence level. If she made 100 of these kinds of “90% sure” predictions, we would expect her to be right (within range) 90% of the time. Using a confidence level to express confidence in a prediction enables it to be recorded to establish a track record that validates one’s accuracy.

This format also makes it easier to “think in bets.” If a person is 90% sure of something, they should be willing (if not eager) to take a 1:8 payoff bet (they put $8 on the table—if they are right and the prediction is in range, then they get their $8 back plus earn a dollar; if they are wrong, then they lose their $8). If they are well-calibrated, they’ll make money in the long run. Now imagine you encounter a person who says he is 90% sure of something but would only be willing to take a 1:2 payoff bet. Something doesn’t add up. By no means are we advocating rampant gambling, but there is power in participating in some low-stakes and relatively safe risks to help people discover how confident they really are and reconcile that with the level of confidence they portray.

4) Aim for precision.

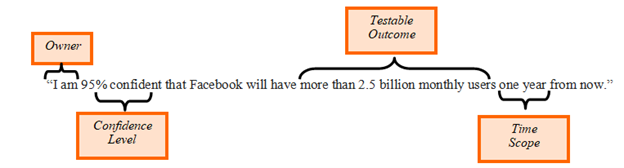

Precise and clear statements can be tested. When making a prediction, be sure it has the four key elements:

Owner

Confidence level

Quantitative outcome

Time scope

For example, the statement below states who is making the prediction, the exact level of subjective confidence, a testable count of monthly users (which could eventually be determined as right or wrong), and a time scope. This is a testable prediction and can be a useful statement.

5) Keep quantified and dated records.

Consider writing down a testable prediction, the time frame, and the confidence levels you assign to each possible outcome (you can also use ranges if that works better for the type of forecast). Try to also include some notes of how you reached that conclusion—what process did you follow, what sources did you include in your research, who did you consult for contradictory opinions, what evidence would it take to change your mind, and so on.

After the time scope and the outcomes are known, go back and record what happened, alongside your original prediction. Over time, you’ll be able to see the accuracy of your forecasting abilities and the tactics/process that led to well-calibrated predictions.

6) Surround yourself with diverse perspectives.

Because of our biases, we tend to seek out and pay more attention to information or opinions that support our own. We may be inadvertently discounting a whole side of information because it doesn’t match what we already think. To avoid this mental trap, we must surround ourselves with diverse perspectives and opinions. Moreover, we must foster an environment where constructive criticism and deferring beliefs are encouraged and taken seriously. There’s no room for egos here.

Professional Demands and Good Calibration

Individual investors generally expect their advisors to be confident—few clients would want to hear their advisor say something like, “I genuinely have no idea what the returns will be for this fund in the next six months …” But it is worth being mindful that there is a difference between exuding professional confidence and being overconfident. Financial professionals can establish justifiable confidence about long-term investing strategies and well-established principles from investing research. They can also redirect their client’s attention away from what is likely unknowable (for example, how will the price of this exchange-traded fund move in the next month?) toward things that are better known (for example, which asset class can expect more volatility in the next 10 years?). Fortunately, successful investing does not require being able to predict the future.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.