![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

The reaction to Donald Trump winning the Presidency and the Republicans reclamation of the Senate has been emphatic. In general, risk assets are rallying aggressively. The S&P 500 Index closed 2.5% higher, while the NASDAQ Composite moved up approximately by 3%, and small-cap Russell 2000 Index closed 5.8% higher. Australian equities also rallied yesterday, though not to the same extent. The wildly positive reaction is being driven by the belief that the Republicans will take actions that are supportive of corporate earnings and stock price appreciation—examples include extending corporate tax cuts that are set to expire, decreased regulations leading to cheaper expansion and elevated merger and acquisition activity, and a general business-friendly mindset.

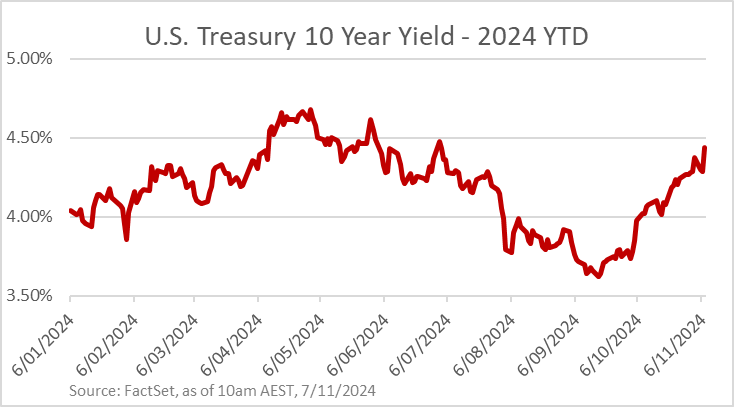

The U.S. Dollar is gaining value relative to developed country currencies (including the AUD) in conjunction with the move up in yields.

The ASX 200 rose 0.8% on Wednesday, while international equity markets had mixed reactions.

Asia: The Japanese Nikkei Index rallied 2.6% while Hang Seng Index (Hong Kong) fell by 2.2% in conjunction with the Shanghai Composite Index declining slightly by 0.1%. Chinese equities are lagging as Chinese Imports have been the primary target of Trump’s tariff narrative all throughout his campaign.

Europe: The FTSE 100 Index fell by 0.1% with the DAX Index down by 1.1%.

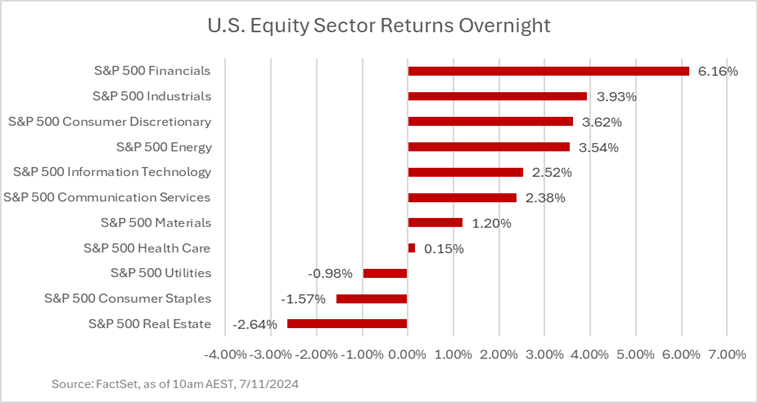

All but three of the U.S. Equity Sectors were positive on the day:

While the majority of U.S. sectors moved higher overnight, they were not all for the same reasons. Some are just participating in the broad-based equity rally, but other like Financials, Energy, and Technology are likely to benefit from Republican control. Financials, specifically Banks, stand to benefit from decreased regulatory restrictions and a steeper yield curve which makes their lending activity more profitable. Energy companies will look forward to less regulation and looser restrictions on drilling and exploration. Highly profitable technology companies will benefit more than others from no increases in corporate tax rates. U.S. small-caps rallied aggressively as they stand to benefit meaningfully from decreased regulation and increased merger and acquisition activity. Small-caps are often acquisition targets of larger companies that are willing to pay a premium for buying their business—this makes up a component of the return small-caps have generated historically. Regulatory hurdles and costs can have an outsized impact on smaller companies as the incremental costs are often harder for them to overcome to compared to larger scale counterparts.

Growth companies across all sizes are benefiting as the business-friendly mindset Trump carries will support their growth initiatives in a variety of ways. Growth companies will also benefit from the lower corporate tax rates Republicans are likely to maintain.

Some takeaways, lessons, and reminders from today’s market reaction:

Even if an investor had high conviction that Trump would defeat Harris and Republicans would take the Senate, the scale of the market moves would likely have still been surprising. To fully benefit an investor would have been required to make large one-way bets. We can never know what would have occurred if Harris had won, but the benefit of making short term one-way bets is almost always not worth the risk as the cost of being wrong is so meaningful. Imagine if an investor believed Harris would triumph and positioned in a way that missed out today’s rally. This further supports our Prepare, Don’t Predict approach driven by fundamental analysis, scenario analysis, and robust portfolio construction.

Most initial reactions align with conventional wisdom and expectations—higher interest rates, Chinese equities lagging the rest of the world, and U.S. small-cap exceptionalism are not surprising.

Reminder that historical analysis of market performance based on election outcomes is imperfect, at best. Today’s massive rally highlights the risk in that as the rally is technically occurring under Biden’s Presidency but is clearly being driven by Trump’s victory. Time will tell how durable today’s moves are. I view them as a resetting of the baseline and in the near future investors will turn back to conventional factors such as earnings, economic data, and interest rate policy to drive their decisions.

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.