![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

By Sarah Newcomb, Director of Behavioural Science, Morningstar

Year two of the coronavirus pandemic brought with it a massive re-examination of personal priorities. The Great Resignation, more people moving from cities to suburbs and smaller towns, and the dramatic increase in funds directed toward sustainable investment strategies are just three examples of how people seem to be changing how they value trade-offs in their work, home, and financial lives.

All these examples involve money, but money isn’t the only factor. People are choosing jobs that are more fulfilling or provide more balance. They are moving to locales that offer more space, natural beauty, or quiet. They want their investments to make money and reflect their values. Everywhere you look, it seems that people are increasingly focused on maximizing not just their wealth, but their overall quality of life.

These trends illustrate something that I think is important, but often overlooked by financial professionals: Major financial decisions often involve both monetary and non-monetary trade-offs.

For a moment, let’s go back to Economics 101 and the foundational concept of utility. In finance we think a lot about optimising utility, but what is it? Utility is a measure of value, but it isn’t simply dollars and cents. Utility is defined as the total satisfaction that can be derived from consuming a good or service.

It’s tempting to take the mental shortcut of assuming more money = more satisfaction. After all, money is far simpler to measure than satisfaction. But maximising utility is not the same as maximising returns. Utility is subjective and comprises many factors. Ignoring emotional costs and benefits leads us to incorrectly evaluate the total utility of trade-offs.

When we evaluate trade-offs, we perform mental cost-benefit analyses. Which option has the highest value when all is said and done? Which will give us the greatest total return on our initial investment? Some of the costs and benefits we consider are financial. Some are emotional. Some are psychological.

I was once offered a position at a large company that would have meant a significant increase in pay, but the job would have required much more travel and the work wasn’t particularly interesting to me. I declined that offer because when I did the cost-benefit analysis, the emotional and psychological costs involved in the day-to-day work and the increased time away from my family outweighed the additional money. I know I’m not alone in this, and I don’t consider this to be irrational or suboptimal. I was not focusing on maximising my financial returns but on maximising total utility.

Many of us can think of actions that are so abhorrent that no amount of money could induce us to participate. When we evaluate the costs and benefits of the trade-off, the psychological and emotional costs outweigh the financial benefits, and the overall utility of the trade-off is not attractive. Likewise, some trade-offs offer benefits above and beyond the financial.

To quote Oscar Wilde, “A cynic knows the price of everything and the value of nothing.”

Price is not the same as value. Price is what you pay for something; value is what you get. And it’s dangerous to equate these things.

I feel it’s important to note that the prime directive of most people’s lives is not to maximise the market price of their assets. As complex beings, we have goals in life that go far beyond the realm of financial security and freedom. Yes, these things are important, worthy goals, but if financial advisers focus solely on maximising financial returns on investments, they miss the greater purpose of financial planning.

Personal finance isn’t about maximizing the amount of dollars a person collects in their lifetime. It’s about making good choices with our limited resources so that we can live the lives we want to live. I believe that Dr. Brian Portnoy of Shaping Wealth puts it best when he says the true goal of financial planning is “funded contentment.”

I know some of the purists out there will argue that the purpose of financial management is to maximise dollars, because then the client can use those dollars to create the life they want. More money means more ability to create that life, so maximising dollars is the goal of the financial manager, and it is up to the client to use those dollars to maximise quality of life.

To these cynics, I would argue that many financial trade-offs carry with them emotional costs and benefits that cannot be separated from the transaction. In these instances, ignoring emotions causes us to value outcomes incorrectly. I know scores of people who would turn down even triple-digit returns if it required them to directly harm others or significantly deplete the planet of natural resources. To the purist who thinks only in terms of numbers, this is irrational, but to these decision-makers the trade-off is clear and there is no sense of loss or missing out by not pursuing such actions.

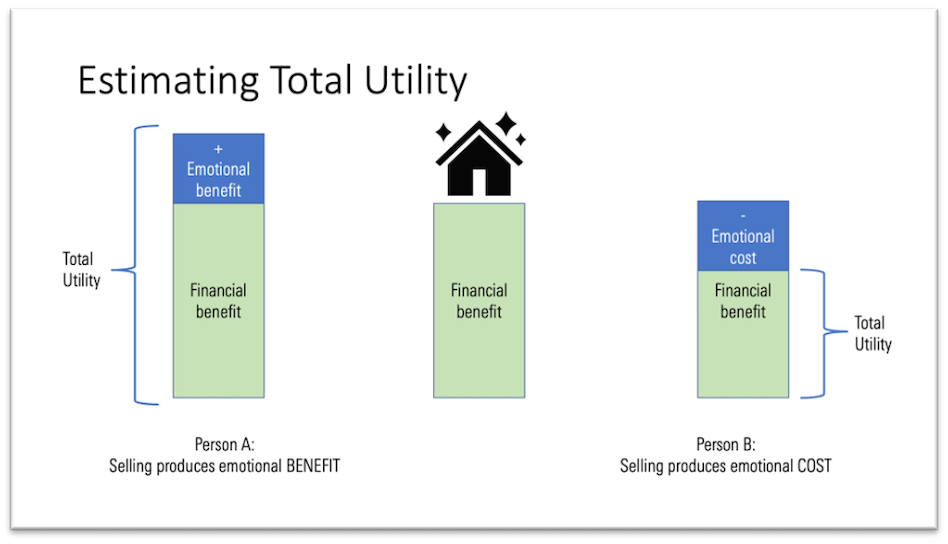

Consider, for example, a person who is thinking about selling their house after a painful divorce. The house is an asset with a specific financial value, and you can easily estimate the financial return that they can achieve through the sale. However, as illustrated below, the emotions they associate with the house will affect the total utility of the transaction.

Source: Morningstar

In this example, Person A associates the house with the negative emotional and psychological aspects of the broken relationship, and so selling the house and moving somewhere new would provide an additional benefit above the financial.

Person B, on the other hand, associates the house with the family they’ve nurtured and the roots they’ve set down. It provides a much-needed sense of continuity and stability in an otherwise tumultuous and uncertain time. For Person B, to sell the house would exact an emotional cost, reducing the overall utility of the transaction.

Thinking about financial trade-offs through the lens of maximising utility allows us to easily explain many human behaviors that don’t make sense through the lens of finance alone. It can also help explain how two people can have wildly different experiences of similar financial transactions.

Crises reveal, and COVID-19 is no exception. This elongated period of uncertainty, stress, and isolation has motivated a major re-examination of priorities for many, and macro socio-economic trends suggest that people are giving more weight to the nonfinancial aspects of their work, home, and investment lives than before the pandemic.

These trends shine a spotlight on the nonfinancial aspects of financial trade-offs, and wise financial professionals will take note. Thinking about financial trade-offs in terms of maximizing utility rather than dollars can help explain why numbers alone are not always convincing to clients.

Advisers who learn to incorporate the emotional and psychological aspects of decisions into their thinking will find that they are more equipped to work side by side with clients to craft strategies that maximise quality of life. Helping clients reach the ultimate goal of funded contentment is a valuable service, indeed.

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.