![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

by Sarah Newcomb, Director of Financial Psychology

Hetty Green was known as the “Witch of Wall Street.” She earned this moniker partly due to the single, dour, black dress that she wore daily, but mostly for her reputation as a litigious and greedy woman whose miserly ways led to her son losing a leg.

During the Gilded Age of Wall Street, while the Carnegies and Rockefellers were building their fortunes and their mansions, Hetty inherited her own small fortune of $5 million. Through wise investments, she turned this into more than $100 million (more than $2 billion in today’s dollars), making her the richest woman in the world at the time. Unlike her better-known contemporaries who left legacies in business and philanthropy, Hetty left a legacy of tightfistedness and self-delusion.

As the story goes, when Hetty’s son injured his leg, she could have taken him to the best hospitals in the world but chose instead to dress in rags and take him to the free clinics in New York City. In Hetty’s defense, she did take him to the best physicians, but she didn’t want to pay them, instead learning what hours they volunteered at the free clinics and visiting then. The time it took to search for this free treatment led to an incurable case, and rather than heal the leg, the doctors removed it. When she suffered a hernia herself, she refused to have an operation and used a stick to put internal things back in place when necessary.

Hetty built her fortune by buying undervalued assets and holding them until they were in high demand. She sold only when buyers came hounding, and often still turned them away. She also lived an extremely frugal lifestyle. While others built family compounds, Hetty lived in a small apartment. She bought a new dress only when her current one wore out.

Some may see Hetty as a model of clever money management, and she was quite a brilliant investor. By any financial measure, Hetty would be said to have been in excellent financial health, but I disagree. She lived simply, but not contentedly. She spent many years of her life in legal battles with family over assets she believed should have been given to her rather than charity. Although Hetty had objectively more money than almost everyone else in the world, she still believed she did not have enough. She believed it so strongly that she spent her life, and ruined her relationships, in pursuit of more.

I tell Hetty’s story because she helps illustrate an important fact: Financial well-being is not only about numbers. It’s also about the stories we tell ourselves because of those numbers.

The financially healthy enjoy the emotional security that comes from knowing that they have enough to weather life’s storms, to rebound, and, if necessary, to rebuild. On top of basic security and resilience, the financially healthy experience a sense of satisfaction and contentment in their financial lives.

The purpose of wealth is to support well-being, but well-being is not a necessary or guaranteed byproduct of wealth. Yes, financial stability can help reduce all kinds of life stressors, and research does reveal a positive relationship between income and life satisfaction, but it’s not necessarily true that more wealth will bring with it a higher quality of life. The idea that wealth = well-being is a mental shortcut that doesn’t hold up under scrutiny.

To illustrate this point, we conducted a small survey in 2021 where we asked a representative sample of around 500 U.S. residents about their emotional experiences with money. People reported how often they had experienced certain emotions with respect to their finances over a period of three months. There were five positive emotions (joy, peace, satisfaction, pride, and contentment) and five negative emotions (anger, sadness, helplessness, fear, and stress). For each emotion, they answered on a scale from “Never” to “Constantly” with Never = 1, and Constantly = 5.

The responses allowed us to create a Financial Emotions Score that ranged from negative 20 to positive 20. A score of negative 20 would indicate that someone constantly felt all five of the negative emotions and never felt any of the positive ones. A score of 0 indicated equal frequency of positive and negative emotions, and a score of 20 indicated constant positive feelings and no negative emotions with respect to their finances. Using this score, we then looked for financial and mental factors that contributed to net positive emotional experiences with money.

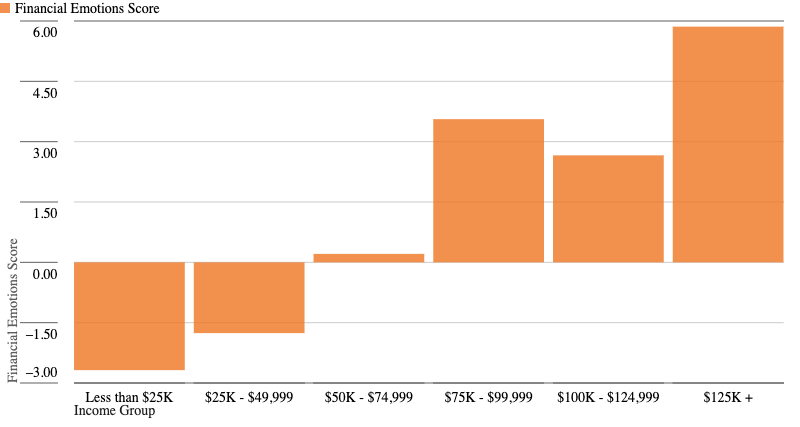

We found that those with higher incomes did have significantly more positive emotional experiences, as shown below.

Financial Emotions by Income Group

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.