From the desk of the CIO: Keeping a cool head during geopolitical turbulence

By Matt Wacher, Chief Investment Officer, APAC

The escalation of conflict in the Middle East has unsettled markets as investors reassess the implications. Geopolitics has reemerged as a meaningful driver of returns this year, most visibly through a rotation toward cyclical and commodity-exposed assets. What initially began with US intervention in Venezuela has since broadened into a more complex and interconnected set of geopolitical risks centered on the Middle East.

As always, our focus remains on separating signal from noise and interpreting events through the lens of long-term, valuation-driven investing. Importantly, the recent selloff does not exhibit the hallmarks of a traditional growth shock. Instead, it’s better understood as a supply-side shock centered on the energy complex, with transmission to broader capital markets occurring primarily through the inflation channel.

Before examining the market reaction further, it’s worth reiterating the principles that guide our investment team during periods of heightened uncertainty—principles we most recently highlighted in our 2026 Market Outlook.

First, we avoid overreacting to headlines. Periods of market stress are often accompanied by sharp sentiment-driven selloffs, followed by equally sharp recovery rallies. History is clear: missing a small number of the market’s best days materially impairs long-term outcomes. Over the past 25 years, for example, missing just the ten best market days would have reduced cumulative returns by more than half.

Second, we rebalance portfolios and remain disciplined in our strategic allocations. Headline-driven volatility creates opportunities to rebalance by systematically trimming assets that have outperformed and adding to those that have lagged. This countercyclical process has historically added value during volatile environments.

Finally, we actively seek opportunities where market prices have moved materially ahead of changes in underlying fundamentals. Elevated uncertainty can cause investors to indiscriminately discount certain assets. Our teams take the time to rigorously assess the true impact on corporate earnings and economic fundamentals, building conviction before acting. The tariff-related volatility last April serves as a recent example that created attractive long-term opportunities.

How and why is conflict spilling into markets?

While Iran and the broader Gulf region represent a small share of global economic output and capital markets, their primary connection runs through the energy complex. Several key dynamics are relevant.

Iranian oil exports account for less than 2% of global oil production and, in isolation, are manageable. The more significant risk stems from potential disruptions to energy shipping through the Strait of Hormuz. Approximately 20% of the world’s oil consumption — over 20 million barrels per day — passes through the strait, along with roughly 20% of global-liquefied natural gas. These flows have limited alternative routes, making Europe and Asia particularly exposed. Unsurprisingly, this is where market stress has been most acute.

Rising energy prices have had immediate spillover effects on inflation expectations and, by extension, central bank policy. Brent crude prices moving above $80 per barrel have pushed yields higher across major government bond markets, with European yields experiencing the greatest upward pressure given the region’s heavier reliance on Middle Eastern energy supplies. Precious metals such as gold and silver have sold off as higher real yields increase the opportunity cost of holding nonyielding assets, compounded by technical pressures following strong prior performance. The US dollar has been the primary beneficiary among traditional safe-haven assets, supported by a reassessment of the timing and pace of future rate cuts.

Equity market outcomes have diverged across regions and sectors. Energy stocks have benefited, while non-US equities — particularly when currency effects are accounted for — have faced headwinds. Emerging markets have been among the most impacted, reflecting their higher beta characteristics and strong recent performance. Within US equities, technology and financials have held up better, supported by the currently isolated impact of the conflict. Similarly, credit market impacts have been resilient.

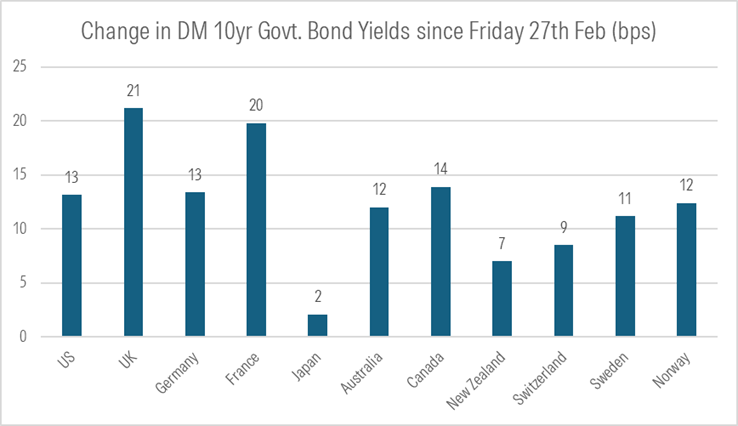

If government bonds were acting as a classic risk hedge, we would expect yields to fall. Instead, yields across most developed markets have risen since late February.

Government bonds have not provided a traditional risk hedge

Source: Bloomberg

What are we watching from here?

The situation is fluid and difficult to predict. Our investment team continues to monitor developments, ensuring portfolios remain well positioned to navigate ongoing volatility while staying anchored to our long-term investment strategy.

Several developments warrant close attention.

First, markets are sensitive to the risk that the conflict broadens into a more sustained regional confrontation. Such an outcome would carry more implications for regional energy infrastructure, extending beyond a temporary or time‑bound disruption to shipping through the Strait of Hormuz.

Related to this is the evolving narrative around the objectives and duration of US and Israeli involvement. Recent communications from the administration have suggested that planned military actions may be limited in scope and duration. However, timelines in geopolitical conflicts tend to shift. A more prolonged engagement would increase the likelihood of sustained pressure on energy prices, raising the risk of broader spillovers.

Thus far, market reactions have remained contained to energy markets and assets exposed through the inflation channel. A prolonged period of elevated energy prices, however, could begin to weigh on the growth outlook and dampen consumer sentiment. To date, there is limited evidence that this is taking hold. That said, upcoming midterm elections add another layer of complexity, as affordability concerns are already emerging as a central theme and may influence policy decisions.

Stay the course

Our investment team stands ready to act should meaningful dislocations emerge, but our primary focus remains on delivering dependable long-term investment outcomes across our strategies.

Risk assets have enjoyed a strong run over the past three years. Against this backdrop, our portfolios are allocated to areas of the market where less optimistic scenarios are reflected in prices.

History suggests that remaining disciplined — especially during periods of heightened uncertainty — has been a sound approach through volatility and beyond.

This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document and the Target Market Determination (TMD). For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 1800 951 999.