By Nicki Potts, Director of Financial Profiling and Planning

Do advisers need a new risk-tolerance tool to help their clients in decumulation?

Transitioning to retirement brings both excitement and uncertainty: The shift from accumulating assets to spending them comes with unique challenges. Are retirees different enough from nonretirees that the industry needs a different set of measurement tools to better understand them? A recent review of retirement income advice by the UK’s Financial Conduct Authority found no difference in how most firms handle risk profiling between the accumulation and decumulation stages. In turn, some advisers have wondered if there should, in fact, be a difference. Would their clients be better served by a distinctive decumulation-focused risk-tolerance assessment? The short answer: In my view, probably not.

The Nature of Risk Tolerance

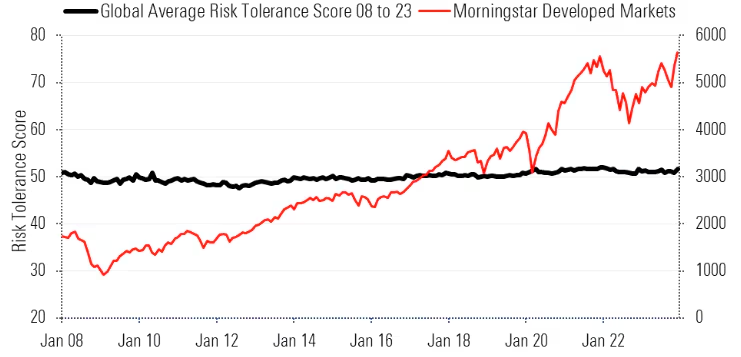

Risk tolerance, or how people feel about taking risks, is a psychological trait. Like many other personality characteristics, risk tolerance tends to be relatively stable over time. Even market conditions only have a small effect on peoples’ risk tolerance, as seen in the chart below. The Morningstar Risk Tolerance Questionnaire shows that the average risk tolerance score has been relatively stable from 2008 through 2023, regardless of whether the markets were up or down.

Investors’ Risk Tolerance Remains Stable Even as Markets Fluctuate

The global average monthly risk tolerance score as measured by the Morningstar Risk Tolerance Questionnaire from January 2008 to December 2023.

Source: Morningstar.

Stable does not mean immutable. Risk tolerance may change for some people, but large changes are not commonplace. For most people, risk tolerance varies little, even as they transition through life stages and events. When we compared risk tolerance scores over several years, we found that 69% of respondents’ scores varied only within 5%, and 90% of people had scores that varied within 10%. For the other 10% of people, risk tolerance varied greatly, but we don’t have a good way of knowing who will be more reactive over time, or what triggers these changes.

For Most People, Risk Tolerance Scores Don’t Vary Much Over Time

The global risk tolerance test-retest score difference as measured by Morningstar Risk Tolerance Questionnaires between February 2018 and June 2021.

Source: Morningstar.

Generally, we do find that risk tolerance declines somewhat with age, in aggregate. Retirees do tend to be a little less risk-tolerant than preretirees. But that’s not true for all. Further, age is just one of the many factors contributing to a client’s risk tolerance at any given time, as shown in the chart below. Moreover, these demographic characteristics still only have a low to moderate association with a person’s risk tolerance.

Demographic Factors Have Only a Moderate Impact on Risk Tolerance

Global average risk tolerance scores as measured by the Morningstar Risk Tolerance Questionnaire from December 2017 to June 2021.

Source: Morningstar. Due to regional income categories, analysis was performed on a global rank order basis where a higher numerical value indicated higher income.

Demographic patterns exist, but that doesn’t mean they should define how we measure something: Their reach is limited and complicated by other factors. It would be imprudent to have a different risk tolerance measure for each stage of life or circumstance—especially when the construct being measured remains the same. Consider measuring weight over a lifetime. People tend to gain weight as they age, but we still use the same bathroom scale to measure weight over time because what we are measuring is the same. The same goes for risk tolerance. The score may change some in decumulation, but the construct of risk tolerance (like weight with a scale) remains the same.

A Holistic Assessment of Risk Tolerance Is Accurate and Powerful

An approach to measuring risk tolerance that focuses only on the decumulation phase of investing would be of limited use. Tools designed for specific situations may inadvertently measure something specific to the situation itself, restricting the generalizability of the results. It would not be possible to discern if a detected change is a result of a change in a tool or a real change in risk tolerance.

There is little evidence that entering the decumulation phase drastically alters risk tolerance for most investors. Meanwhile, assessing risk tolerance holistically produces results that are valid across all financial contexts, whether we are making saving, investing, or drawdown decisions. Regular reviews and reassessments (about every two to three years) are essential to ensure any material change in a client’s profile is reflected in the financial plan. By measuring the same thing using the same benchmark, the results can be compared over long periods of time and across different circumstances. This means real changes for a client can be readily identified, discussed, and addressed. That way, we won’t miss the 10% of clients whose risk tolerance changes materially over time, nor will we erroneously detect substantial changes among the other 90%.

Compared with a decumulation-specific tool, a robust financial risk tolerance tool will best capture investors’ overall risk preference and serve as a benchmark across the long-term advice journey.