![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

By Matt Wacher, Chief Investment Officer APAC, and James Foot, Head of Research, APAC.

Key Takeaways

China’s latest economic woes is a stark reminder that investing is complex. Here is a quick update of the main issues dominating media coverage:

Let’s remind ourselves that China worries are not new. Every few years, we seem to go through a new wave of unease about developments in the region. In 2015/16, we saw Chinese economic weakness, financial panic, and a strong policy response. In 2018, we faced “trade wars” with Donald Trump. In 2019, we had the Hong Kong protests. In 2020, we had the Covid outbreak in Wuhan, with years of lockdowns and economic instability. And now again in 2023, we have a new wave of Chinese concerns.

This confuses the average investor, with a constant tussle between the pros and cons of emerging market investing. Here is just one example:

|

Recent Positive Article |

Recent Negative Article |

|

“Emerging markets lead the way in the battle against inflation” – Investors Chronicle, 2nd August 2023 |

“China’s downside risks are growing, and its economy is less likely to reach 5% this year” – CNBC, 16th August 2023.

|

In truth, investors have always lived with this uncertainty. Many will have been burnt by sudden economic and policy shifts at some point in their investing life—perhaps more commonly in emerging markets, but also developed markets. This doesn’t make a market uninvestible, but it does mean we need to be ready for future shifts when estimating cashflows and valuing assets, applying a margin of safety. In this regard, valid concerns have been raised about weaker shareholder rights and protections in China compared to typical ordinary shares in developed markets.

That said, every asset has a price. Sometimes, it can make sense to buy unloved assets (with the appropriate sizing) that can become wonderful investments, despite not meeting the standard perceptions of quality. In our recent “Global Convictions” document in July 2023, we said the following about China and emerging markets more broadly:

Global Convictions – Views of China and Emerging Markets

China—the largest emerging market—has observed a bumpy economic recovery since the government abandoned strict COVID-19 measures late last year. Initially, optimism soared but that optimism has cooled off. The Chinese economy is decelerating after a strong first quarter. Consumption remains the key focus this year, and the data continues to indicate the Chinese consumer is cautious.

Broadening out, the structural story around emerging markets remains intact. A burgeoning middle class continues to develop in emerging markets and should present interesting opportunities for investors, albeit with higher volatility.

We retain our conviction at Medium to High[1]. We consider emerging-markets equities to be among our preferred equity regions (alongside selected European equities). We also need to remember that emerging markets are heterogeneous. Investors tend to bucket emerging markets as one, but often the real opportunities present themselves at a country, sector, or regional level. For example, despite the many challenges confronting Chinese equities, both the absolute and relative valuation remains attractive.

The framework to decide if China is a good investment

The big question is what investors should do in response to the bad news? This is quite a delicate one to answer. For example, do these developments mean an allocation to China is less attractive or more attractive versus other equity markets? Does it have the hallmarks of a great buying opportunity or a value trap? Would a change in exposure enhance the total portfolio outcome or bring unwanted risks?

China currently has some, but not all hallmarks, to make it a contrarian opportunity. Our experience of prior pariahs—where we have made high returns for clients in our multi-asset portfolios—include Korea and energy equities. The common features of these contrarian opportunities included (1) terrible economic or corporate news (2) sustained selling (3) 50% + falls in share prices (4) extreme lows in price versus fundamentals, using historic and a range of potential scenarios, and (5) alarm, disdain and pessimism from the investing community.

China meets conditions 1, 2 and 5. It is also on the edge of 3, depending on the index, with MSCI China down approximately 55% from its 2021 peak and the Hang Seng down approximately 45% from its 2018 peak[2]. However, point 4 is less convincing, despite several companies sitting at multi-year lows versus current fundamentals. Importantly, property developers are now a small part of the Chinese market, so direct exposure is less of a concern.

Looking to the downside, a checklist for value traps should include technological obsolescence, government policy shifts, and excessive leverage at an industry or country level. Despite some concerns around Chinese debt levels, for the most impacted companies, we can probably rule out the first and third given many of the biggest Chinese companies are leading or benefitting from technological changes and are not heavily levered.

It is always worthwhile thinking about who is on the other side of any trade. At this stage, the most vocal bears on China have warned of further adverse policy shifts impacting profits. This is a fair concern and should be part of any investor’s scenario analysis. China does not have the democratic processes that slow down and make more transparent, big policy shifts. But this is not new. Additionally, many of the underlying government concerns, such as the power of big tech, are common in other countries where regulatory and tax shifts are also taking place. As we look at the range of potential scenarios, our valuation analysis suggests this is not a value trap, unless your central case is one of extreme economic policy.

Are Chinese stocks worthy of portfolio positioning?

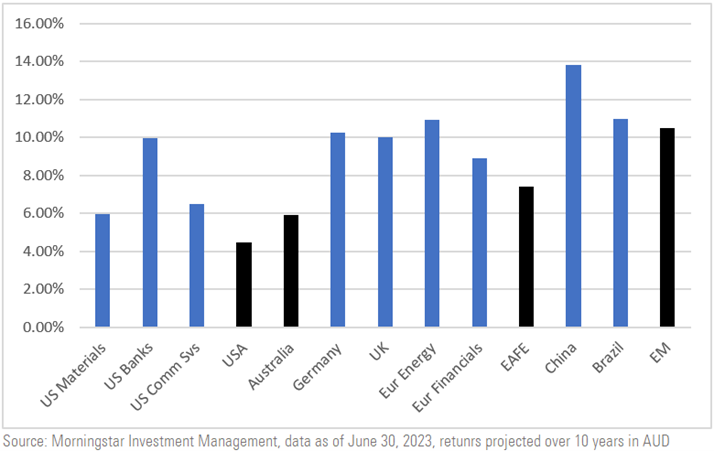

From a long-term valuation driven perspective, China offers strong absolute and relative value, even allowing for potential further shocks. As you can see below, Chinese equities rank strongly compared to key equity markets based on our return assumptions.

Exhibit China has a high “valuation-implied return expectation”[3] compared to a list of major markets.

=

=

Our portfolios reflect this assessment: we have been topping up exposure and rebalancing our holdings. That said, we are mindful to keep position sizing at sensible levels. We continue to monitor developments closely and stand ready to move with the environment, ensuring we adapt to changes in market conditions. As Howard Marks famously said, “In order to outperform, by definition, you have to depart from the crowd”. Our views are steeped by an enormous body of research, plus we have the resolve to do what we believe is right by our investors. If you have any questions regarding any of the above, we welcome you to reach out to your Morningstar representative.

[1] In assigning an asset class conviction, an analyst trades off the aspects of an investment opportunity that argue for and against it, culminating in the expression of a conviction level. The conviction level is expressed on a five-point scale (Low, Low to Medium, Medium, Medium to High, and High), and serves as a key input into our asset-allocation process. Our conviction scoring system is based on four criteria: absolute valuation; relative valuation; contrarian indicators; and fundamental risk.

[2] As of 23 August 2023

[3] Valuation-implied returns are specific to the current valuation and could be expected to revert over the medium-to-long term (we typically define this as a 10-year horizon). According to Morningstar’s extensive research, we believe the most reliable way to identify the valuation-implied return of an equity asset class is based on the following equation: Valuation-Implied Return = Expected Change in Valuation + Growth + Total Yield + Inflation.

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.