Adviser-to-client template: Lessons from 2025

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

We say it every year, but 2025 has gone quickly! From tariff announcements in April to talks of AI bubbles now, it’s been a long and sometimes trying year in investment markets. But these events have also served to remind us of the core principles of sensible investing: to have a diversified portfolio, to keep behavioural biases in check, and to stay the course.

What can we learn from the year that was?

As we look to 2026, there are some key learnings we can take from 2025. We saw some surprises in the U.S. economy, which remained resilient despite rising import tariffs. A number of factors contributed to this, with many business absorbing the new costs rather than passing them on, which kept prices stable, even if they sacrificed some profits in the process.

However, despite a strong U.S. economy, the country’s equity markets left the pace-setting to others in 2025 (despite largely leading the way in prior years). The Korean market powered ahead, while emerging markets in general enjoyed higher returns. Even the U.K. posted higher returns than the U.S. This change in the year-to-date positions serves as a valuable reminder that the starting point for any asset, and its prevailing price point and valuation, are all-important.

What can we expect in 2026?

Our investment manager, Morningstar, notes that this calm might not continue, and expects tariff effects to continue showing up in 2026, stalling growth and lifting prices. However, they also expect that the AI boom will likely offset some of these effects, particularly as its capabilities become more common and widely used across a range of applications in businesses.

This year also saw some unusually high gains, so for next year, Morningstar anticipates a return to more modest returns. They’re also cautious about companies spending a lot of money on AI, and are seeing better value in markets like the U.K. and Brazil in sectors such as healthcare and consumer staples.

What should you do to prepare?

It bears repeating, but the best thing you can do is nothing. Staying invested is one of the most effective weapons in the investors’ arsenal, and Morningstar’s portfolios are built to withstand turbulent conditions. If you have any questions about your portfolio, please don’t hesitate to get in touch.

Regards,

Adviser

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Don’t Gamble With Your Risk Tool

The best risk-tolerance questions lead to meaningful conversations with clients.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Protected: From the desk of the CIO: What 2025 Tells Us About 2026

From the desk of the CIO: What the gold and AI booms mean for investors

By Matt Wacher

Big market moves are becoming more common, with large gains in September carrying over into October.

This is true for shares, bonds, currencies and commodities, with gold rocketing this year up over 60%. This sharp price is the result of investors and central banks buying to diversify their assets away from US dollars. We’re seeing these moves because of concerns around the high level of debt, deficits and the independence of the US Federal Reserve.

One often overlooked factor is the very small size of gold as an asset class, which can lead to exaggerated price moves in both directions when sentiment changes rapidly. As with all financial assets, huge price rises and frenzied universal popularity don’t bode well for future returns, so investors should take note of the large falls in price that followed comparable episodes in the past.

In equity markets, it’s Artificial Intelligence that is still the key driver of market returns, share prices surging for so-called ‘hyper scalars’, companies that provide global scale data centres. Here, there are clear signs of a change in fundamentals that echo those of the last great IT boom in the late 1990s. Two of note are (1) a step change in capital spending and (2) tie-ups between major players.

Spending on capital expenditure has spiked for firms that had previously sustained high rates of profitable growth without the need to invest a lot of capital. This made them highly profitable and set them apart from more traditional industries, like manufacturing and real estate, that need lots of capital to expand. But now these are spending up large on data centres, servers, advanced computer chips and even nuclear power generation. For example, this year $353bn USD of AI-related capex has been committed by just 4 companies: Alphabet; Amazon; Meta and Microsoft. The investment is of course expected to be profitable but it’s uncertain how long it will take to pay off and what the eventual return on capital will be. Right now, it is very low.

The mammoth scale of investment needed has prompted a coming together of many companies to fund and make what is required. Non-profit entity Open-AI of ChatGPT fame has been at the forefront of dealmaking, buying custom AI chips from multiple chipmakers, and Nvidia committing to invest up to $100bn in it. Microsoft is a key backer of Open AI. While these companies were already connected as suppliers to each other or joint venture partners, this extra step ties their fortunes ever more closely together and creates the conditions for a rise in the correlation of their returns. As these businesses are already large parts of stockmarket indices, investor portfolios are becoming less diversified and more concentrated. A similar dynamic existed during the late 1990s when telecom, media and IT companies became highly correlated.

So what does this mean for investors? Of course, productive investment that pays off will make these companies more valuable, but they are already priced for this. The real lesson from prior technology booms is that they are bullish for high quality bonds because they put downward pressure on global prices. AI is expected to have similar benefits in terms of reducing the costs associated with providing goods and services and improving their quality.

In our portfolios, our focus remains on opportunities and diversifiers that are not driven by the AI boom or still remain out of favour including healthcare, US small companies, UK equities, emerging markets and some traditional consumer names.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Adviser-to-client template: The golden rule

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

I’m betting you’ve seen the news headlines and images of people around the world (including in Sydney’s Martin Place) lining up to purchase gold bullion. No longer just the stuff of pirate legends, speculative assets like gold and cryptocurrencies are seeing increased popularity in light of recent market conditions. But rather than asking if all that glitters is gold, perhaps we should be asking whether this speculation is justified and how investors should respond.

Why are you hearing about gold?

With markets this year characterised by uncertainty and volatility, gold has attracted a lot of attention from investors. These investors are hoping to diversify, find a safe haven in a market that’s consistently been in flux, while taking advantage of rising prices. But can gold deliver on all of these promises?

What should investors be wary of?

While these assets can be tempting, it’s important to approach them with caution and a clear understanding of their risks. Yes, gold could potentially hedge against inflation or currency devaluation, and could similarly provide short-term gains. However, its long-term value is less certain compared to traditional investments.

As gold is a small asset class, its price can move dramatically in both directions when sentiment changes. And with all financial assets, these large price rises (not to mention hype) don’t bode well for future returns. In the past, where we’ve seen comparable cases, they’ve typically been followed by large falls in price – a pattern that’s well worth remembering as the gold frenzy continues.

Speculation in moments such as these can also lead to emotional decision-making that’s coloured by headlines and herd behaviour, which in turn can lead to increased portfolio risk. And as these assets are highly volatile, they may not align with a disciplined, long-term investment strategy, such as the one deployed by our investment manager, Morningstar. Instead, we – and Morningstar – urge that investors focus on fundamental analysis, diversification, and a focus on generating long-term value rather than chasing trends.

What should you do next?

In short, nothing. A well-diversified portfolio built on sound investment principles is positioned to withstand market volatility. By staying invested, you can avoid impulsive decisions that are driven by market hype.

If you have any questions about gold or more broadly about your portfolio, feel free to get in touch. I look forward to chatting.

Regards,

Adviser

Important Information

As noted previously, this document is intended to support your service proposition to clients and the commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use

Integrating Wellness Into Financial Advice

Financial advisers can create value for clients by incorporating psychological and physiological metrics.

Have you noticed the number of entourage members supporting professional athletes? It takes a team of coaches, doctors, physiotherapists, psychologists, nutritionists, and legal and financial advisors to holistically manage and support an athlete’s health and well-being throughout their career.

Similarly, researchers and advisors are starting to recognize that good financial health and well-being are best achieved through an integrated approach that treats clients’ financial lives holistically. What if the financial advisor was part of an entourage that included a financial health physician, a financial mindfulness coach, and a financial crisis therapist? These professions may be hypothetical, but the thought experiment suggests real-life techniques that advisors can use today.

The Financial Health Physician

We already embrace and incorporate clients’ psychological reactions—such as how they think, feel, and process events and experiences—into financial planning. Yet, we may find it odd to consider doing the same for physiological reactions, such as our fight-or-flight responses, like heart rate, blood pressure, and muscle tension.

What role does physical health have in financial outcomes? Recent interdisciplinary research published in Financial Services Review finds that psychological and physiological responses interact with financial triggers to drive and influence our behaviors and decision-making processes. What may start as physical health stress (like sleep disturbance) can lead to mental stress (like mood swings) and a tendency to make less-than-optional financial risk-taking decisions (like panic selling during market volatility). And this effect can go the other way, too; financial stress can create anxiety, sleep disturbance, and physical unwellness.

How would a professional assist? A financial health physician mightmonitor psychological, physiological, and financial situations together in real time. This would allow them to identify core stressors at an early stage and develop an appropriate strategy to address them. For example, panic selling may be abated with a personal check-in when elevated heart rate and sleep disturbances are detected during volatile times.By attending to physical warning signs, investors could avoid costly mistakes.

The Financial Mindfulness Coach

Mindfulness is the practice of being fully aware and accepting of what you’re presently doing, feeling, and experiencing. It can enhance general well-being by reducing stress and anxiety, increasing focus, and helping regulate emotions. A new psychometric financial mindfulness scale from researchers at Cornell University and Georgetown University attempts to extend the benefits of mindfulness to financial health by focusing on the awareness of your current objective financial state (that is, how much you are spending and your financial balances) and the acceptance of that state (that is, how well you manage your emotions when engaging in financial matters).

What role does mindfulness have in financial outcomes? People can experience a disconnect between how they perceive their finances and their financial reality—you might call it money dysmorphia. This, in turn, can cause investors to feel stress and anxiety due to the perception of not having enough, regardless of their actual financial state. That can lead to clients having unrealistic financial goals, developing an inability to enjoy the fruits of their labor, and even taking on excessive debt, at the extreme.

How would a professional assist? A financial mindfulness coach would help clients identify whether they have a distorted perception of their finances. They could supply investors with appropriate measures to manage emotions and drive positive behavioral changes during periods of financial stress or discomfort. A financial mindfulness coach might also incorporate tracking and budgeting tools to drive awareness and practical mindfulness exercises to drive acceptance. By being better connected to their finances, clients could improve their financial health.

The Financial Crisis Therapist

People often need emotional, practical, or social support to manage and recover from a crisis, whether large-scale events such as pandemics and natural disasters, or personal hardships like divorce or illness. Financial crises can be just as overwhelming, so it makes sense to consider the benefits of a therapeutic approach to helping investors respond.

What role does crisis support have in financial outcomes? In times of crisis, people need support to bolster their capacity to respond to the occasion, as their emotions, thinking, and behaviors can be disrupted. As an interdisciplinary research review in the Financial Planning Research Journal demonstrates, investors look for emotional support as well as information and feedback in a crisis. As a crisis deviates further from typical circumstances, high emotions can negatively affect decision-making abilities. Support during a crisis can help investors stabilize their emotions and develop strategies to move forward.

How would a professional assist? A financial crisis therapist might support a client during a period of financial distress by helping them regain their composure and triage their issues. This kind of support would help investors gain greater resilience and improve their capacity for rebounding from setbacks.

Holistic Personalization

Clients may not be able to turn to an entourage of such professionals to improve their outcomes, but financial advisors can take on some aspects of these roles in their own practices. While you may not be taking a client’s blood pressure or making notes as they lie on a chaise lounge, you can incorporate practical tactics that incorporate mind, body, and spirit. For example, try asking clients to describe the emotions and physical sensations they are experiencing in response to their current financial state, and look for signs of distress or disconnect. Or it can be as simple as checking in with your clients about their health and whether their spending and saving goals are aligned with their values.

This kind of interdisciplinary approach integrates well with the behavioral finance practices that many advisors are already adopting. Advisors who can provide holistic support to their clients can deliver a level of personalization that unlocks not just good financial outcomes, but good life outcomes.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

From the Desk of the CIO: It’s in the price

By Matt Wacher, Chief Investment Officer, APAC

Key takeaways

- Global regional diversification pays off

- Higher US IT valuations raise the bar for expectations

- Favour areas where valuations and expectations are lower

Global diversification continues to pay off for investors with several of our overweight equity positions – Korea, China, Japan and Brazil – performing well. Gains reflect companies and/or broad economic outcomes in these countries surpassing the low bar of subdued expectations.

On the other hand, high expectations tend to be harder to beat, so it’s natural for investors to review the stellar run in US IT stocks and ask if that can continue. Most of the rally in US equities has come from a re-rating of US IT companies which are focused on AI superscalars, strongly supported by blow away earnings results from select majors including Nvidia, and more recently, Cisco Systems. While other sectors have also risen, it’s US IT that has been the key driver of the US market because of its scale.

Morningstar’s recent review of the US IT sector explored in depth the key drivers of the industry’s growth, profitability and whether there is still value. Taking the long view, it is clear that the re-rating – investors paying more per unit of sales, cashflows or earnings – has supercharged returns over the past 5-10 years. Looking forward, the big players in software, hardware, semiconductors and IT services still have a great outlook in terms of the strategic advantages (using Morningstar “MOAT” definitions of competitive strengths) that can support faster growth and higher profitability than peers and other industries.

However, it’s worth noting that uncertainty levels for future earnings growth are also very high in many cases, as AI quickens the pace of change, and poses direct threats to several business models. Seen this way, we find the overall reward for risk not attractive for US IT, given full valuations, the fast pace of change and high levels of earnings uncertainty.

We continue to see better prospects in areas where lower earnings expectations are being priced in, such as healthcare, which have been hurt by US government regulatory changes and potential tariffs. Ultimately, investors must consider what is priced in, as well as what is most likely to occur. On this basis we see less upside for US IT, and more upside for Healthcare and select Emerging Markets equities.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Adviser-to-client template: Minimising the effects of the investor return gap

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

“The investor’s chief problem—and even his worst enemy— is likely to be himself.” – Benjamin Graham

Something I’ve come across a lot in my day-to-day conversations is the concern that short-term market moves can derail an investor’s goals – or indeed that short-term wins dictate future success. While market corrections can be scary, investing, at its core, is about the long game. Patient investors are rewarded, while those who take the short-term view, more often than not, sabotage their financial futures. This can show up in a few ways, whether that’s by chasing yesterday’s winners, attempting to time the market and therefore buying and selling assets at the wrong times, such as pulling out during volatility, or succumbing to headline noise about the latest ‘hot’ stock.

Understanding the impact of the investor return gap

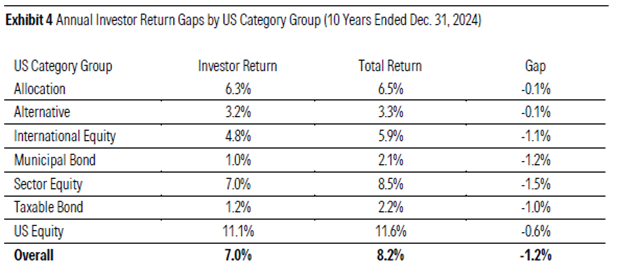

It’s these types of moves that can result in what our investment manager, Morningstar’s, behavioural finance team refers to as the ‘investor return gap’. A study recently completed by Morningstar in the US was found to ‘estimate the average dollar invested in US mutual funds and exchange-traded funds earned 7.0% per year over the 10 years ended Dec. 31 2024 (“investor return”). Sound all right? Well, that’s about 1.2 percentage points per year less than these funds’ 8.2% aggregate annual total return over that time, assuming an initial lump-sum purchase.

In practice, that 1.2 percentage point investor return gap, which is explained by the timing and magnitude of investors’ purchases and sales of fund shares during the 10-year period, is equivalent to around 15% of the funds’ aggregate total return. Which is to say, it’s a gap that most investors would prefer to pocket rather than sacrifice. The table below shows what this looks like by category group.

How do you mitigate this gap?

Put that way, the prospect of the investor return gap is a scary one. But understanding how short-term or panicked moves can set you back is also a useful tool for ensuring that a long-term view is crucial to financial wellbeing. Familiarity with the inevitable fluctuations of markets is also something that can alleviate stress when these conditions occur. Morningstar’s portfolios are constructed to withstand tricky market conditions that prompt these sorts of loss-aversion behaviours, providing a margin of safety. By sticking to your plan, staying invested, and having your money compound, you’re already well on your way to minimising the effects of the investor return gap.

If you have any more questions about how your Morningstar portfolio is positioned, or if you’d like to walk through some common behavioural responses and how to alleviate them, I’m always happy to talk. I look forward to chatting soon.

Regards,

Adviser

Important Information

As noted previously, this document is intended to support your service proposition to clients and the commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use.

3 factors that enable financial advisers to improve returns by 3%

An understanding of how advisers add value allows self-directed investors to set themselves up for success.

Vanguard’s report ‘Adviser’s Alpha’ looks at how much value financial advice can add to investment returns. The report concludes that financial advice improved net returns by 3% for investors.

The report outlines specific areas where advisers are adding this value including overtrading, a tailored plan and technology, tools and knowledge. They serve as pertinent lessons that self-directed investors can take to improve their financial outcomes.

Overtrading

The report calls out the period between February and April 2020 to demonstrate how advisers can add value as a behavioural coach. It quotes statistics from ASIC that showed 5,000 accounts were being opened daily during this period. These new investors only held onto their securities for an average of one day. It wasn’t much better outside of this period. A year prior, it was 4.5 days on average. 80% of these new investors made losses.

Financial advisers can add value as behavioural coaches and stewards of their clients’ investment goals.

Those that sold during March 2020 sold at the bottom of the market. As we all know, markets have recently set record highs—doing more than recovering those losses.

How self-directed investors can prevent overtrading

Overtrading and overconfidence comes from seeking wealth maximisation. That is a focus on maximising your money instead of having a clear goal in mind and working towards that goal.

An investment policy question connects your goals to the actual investments. In addition to specifying your goals, priorities and investment preferences, a well-conceived IPS ensures that you have a set review process that enables you to stay focused on the long-term objectives. This way, you can ignore short-term noise and avoid irrational decisions.

There are six steps to an Investment Policy Statement:

Step 1: Document your goals

Documenting your goals might seem straightforward, but there’s more to this than meets the eye. Quantifying and prioritising your goals is paramount. If you do not quantify, you cannot measure success, and if you do not prioritise, you risk letting a lack of focus hinder you from achieving any goals.

Step 2: Outline your investment strategy

The most successful investment strategies are straight-forward and succinct. For instance, a strategy for those embarking on their investment journey may be as follows: ‘To invest primarily in low-cost passive investments, increasing contributions along with salary increases. Begin with 80% in aggressive assets, and transition to 50% in aggressive assets by retirement’.

An investment strategy for retirees might be: ‘To invest in dividend-paying equities and annuities to deliver a baseline of income; regularly rebalance to provide additional living expenses. Target a 50% defensive/50% aggressive mix.’

Step 3: Document current investments

The next step is document all of your current investments with their recent values.

Step 4: Document target asset allocation

Asset allocation is larger driver of returns than security selection. It is important to align your asset allocation to the goals you hope to achieve.

Remember that assets change in value. Your target asset allocations may be better expressed as ranges instead of a set figure to avoid over-rebalancing and incurring transaction costs. For example, you might have an 80% allocation towards equities, but on any given day that 80% could shift to 75% or 85% of your portfolio. Instead of 80%, express your equities asset allocation as 75%-85%. For major asset classes, stick to a range between 5-10%.

Step 5: Outline investment selection criteria

In your Investment Policy Statement, you must outline your investment selection criteria that will provide guidelines for the types of investments that you want to hold.

For example, if you use Morningstar’s research in your investment decision-making process, you could specify that your equity holdings must have at least 3 stars, or your mutual funds must all be rated Bronze or better. Defining criteria for selecting investing will keep you accountable and focused on what matters.

Step 6: Specify monitoring parameters

Implicit in defining an investment policy statement —from asset allocation to investment-holding specifics—is that you’ll periodically check in on your portfolio to ensure it is still on track to reach your goals.

In this section, you will specify how often you will review your portfolio. Understand yourself, and what works for you—if checking too often will cause poor investor behaviour (such as panic buying or selling), set a less frequent period for review.

This is the crucial last step to avoiding over-trading. It outlines the reasons in which you will buy or sell assets in your portfolio, and at what intervals. You may also buy and sell assets if current holdings do not meet your investment selection criteria anymore.

A portfolio tailored to suit your needs

Your portfolio should be reflective of your own goals. The value that a financial adviser provides is tailoring your investments to you as an individual or family. Financial plans, are by regulation, created in an investor’s best interests by financial advisers.

This can be done by a self-directed investor and requires an investment of time. Many articles, including this one, are general in nature. I write about how a particular stock ticks all of our analysts’ boxes, but it is up to a self-directed investor to decide whether it is in line with what they are trying to achieve. General advice and information do not account for your personal circumstances and requires work from a self-directed investor.

Financial advisers do this work for you.

How self-directed investors can tailor a portfolio to suit their needs

Morningstar is a proponent of goals-based investing. The four steps to construct a goals-based portfolio are:

- Define your goals

- Calculate your required rate of return

- Asset Allocation

- Select your investments

Resisting the temptation to chase a popular or well performing investment that doesn’t align to your goals is challenging. Knowing how your investments are connected to your goals helps to limit poor decisions when emotions are heightened during periods market volatility. An investment in your own education is also needed to understand the foundations of investing and the attributes of individual investments.

Technology tools and knowledge

One of the largest benefits that financial advisers offer is the access to financial technology and tools that can model financial scenarios. These tools allow them to easily determine the best path forward for their clients in a scalable manner. They can model out withdrawal rates, portfolio projections and age pensions. They can then adjust the variables to ensure that they are accounting for a variety of scenarios that may alter the outcomes of the client.

These tools can often be tens of thousands of dollars a year in subscription costs which the adviser can justify as they are using these tools across their entire client base. These tools aren’t as accessible for individual investors.

However, individual investors do not need to worry about a suite of clients. They only need to worry about themselves. They do not need scalable solutions because there is no scale. There are many tools available to retail investors that can help them manage their portfolio. Even without these tools, a spreadsheet can do some of the heavy lifting when it comes to the math behind an investors’ portfolio. For example, my colleague Mark LaMonica has recently put together a spreadsheet that helps to calculate the roadmap to generating $100,000 in passive income.

These tools give advisers an edge in terms of efficiency when putting together portfolios, but that is not to say that self-directed investors do not have edges themselves.

For example, Approved Product Lists. To operate as a financial adviser in Australia, you must be authorised under an Australian Financial Services Licence (AFSL). Some AFSL holders only allow their representatives to invest in a select range of products that fit a set of internally established criteria—limiting the securities an adviser can recommend. As a self-directed investor, you are able to invest in the securities that are best suited to you, without restriction.

I’ve outlined some free tools here for when you are just starting to invest. There are also a multitude of tools on Moneysmart and Noel Whittaker’s website for those that are further along in their journey.

Final thoughts

Ultimately, an adviser’s job is to know what is best for their clients. Their job is to help you reach your financial goals, which involves meeting and maintaining qualification standards. Most self-directed investors are not full-time investors. They are establishing and maintaining their portfolios to reach their financial goals outside of their day jobs. It is hard work.

Self-directed investors may not have the same time to dedicate to learning and understanding the depths of the many aspects of personal finance—tax, estate planning, investments, structuring of assets. Financial advisers usually have a suite of trusted professionals that they team up with to manage these aspects holistically. In the same breath, self-directed investors are not usually fully self-directed. They will outsource some of these aspects to professionals—commonly estate planning or tax.

So, the question is—does the fact that you are able to recreate these advantages mean that you should not get a financial adviser?

Just like many aspects of personal finance it depends on your circumstances. Some individuals have no interest in managing their financial affairs and would rather outsource to a financial adviser. Others will decide that they do not have the aptitude or time to learn. Some are not in the position to afford the financial advice fees.

A large part of the excess returns a financial adviser provides is acting as a behavioural coach and ensuring that their clients make decisions that are in their best interests. More than anything this is a result of the structure provided by the financial advice process.

Some individuals will determine that they are not able to do that without a third party. Some will put the work in to learn about investing and set themselves up for success. Many people will continue to achieve poor outcomes by not bothering to define their goals and put an investment strategy into place and will haphazardly chase strong performing investments. A self-directed investor can achieve great results. It just requires work—and a willingness to do it.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Why getting financial advice is more of an emotional decision than financial

Originally published in FT Adviser, this article was written by Morningstar’s Global Head of Decision Sciences, Ryan O. Murphy.

Clients may not be aware of behavioural science or coaching, but it forms much of what they seek from financial advice and planning. Emotional factors play a greater role in the decision to hire an adviser than practical ones, and continue to play an essential part throughout the relationship.

Used in the right way behavioural science can enhance the value consumers derive from the advice relationship. The actions and principles involved are simple and fit naturally into adviser-client conversations.

Morningstar Investment Management Australia recognised at Financial Newswire Fund Manager of the Year Awards 2025

Morningstar Investment Management has been recognised at the Financial Newswire Fund Manager of the Year Awards. This recognition is a reflection of the expertise, discipline, and collaboration that underpin everything we do. A special congratulations to our CIO Matt Wacher, CAIA, Senior Portfolio Managers, Bryce Anderson, CFA, and Bianca Rose, for their outstanding leadership, and to George Antonas, who leads our Investment Operations with precision and commitment.

The awards included:

– Winner – Managed Accounts Manager of 2025

– Winner – Multi-Sector Growth: Morningstar Multi-Asset Real Return Fund

– Highly Commended – Multi-Sector Growth SMA: Morningstar Growth Managed Account

– Runner-up for the Overall Fund Manager of the Year

Morningstar Investment Management was also nominated for Australian Equities Large Cap (Morningstar Australian Shares Fund).

Awards like this highlight not only individual excellence but also the strength of our collective approach to delivering on behalf of investors.

(From L to R: Noah Kaplan, Bianca Rose, Matt Wacher and Bryce Anderson)

For more details, refer to Financial Newswire.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Adviser-to-client template: A mid-year recap

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

As we move through the second half of the year, we’d like to recap what’s happened so far in 2025, and how your portfolios are positioned for the coming months and years.

Much of the market noise this year has centered around volatility, with U.S. President Trump’s tariff measures kicking off waves of turbulence and, at times, sharp market corrections.

But despite that, it’s been a strong year for equities and bonds. Australian equities are up around 8%, with small caps rebounding after underperformance. Globally, we’ve seen strong results out of Europe, while China and emerging markets have had a mixed response, though the reactions to ongoing tariff announcements have muted somewhat. The U.S., on the other hand, has lagged. April was an interesting turning point, with a sharp sell-off followed by a V-shaped recovery.

A new lease on life for the bond market

Over the past seven months, bond returns have sat around the 3.5%-4.5% range, proving more attractive now than they have been for the last 15 years in the aftermath of the GFC. This also means that government bonds are again offering diversification benefits.

A macro view of Australia and the U.S.

Domestically, growth has been weak, and you’ve likely heard that inflation has steadied, with the Reserve Bank of Australia cutting rates this month for the third time since the rate-hiking cycle began and more being anticipated. Unemployment remains low, and while this stability brings reassurance to many Australians, our investment manager Morningstar cautions that there are still some risks to hedge against, including tariffs, geopolitical tensions, and global slowdowns. Overseas, U.S. CPI data is showing similar inflation to Australia, though the future threat of tariffs may see these numbers climb. And, in a move set to mirror many regions, the U.S. Federal Reserve is also expected to cut rates 2-3 times to encourage growth as unemployment edges higher.

Where is Morningstar seeing opportunities?

So what does this mean in practice? Morningstar are seeing pockets of valuation opportunity in emerging markets (Brazil, China, Mexico), which are offering stronger long-term return potential than developed markets. Conversely, at home, Australian banks have seen strong price gains, which leaves less room for future returns. Morningstar has also identified opportunities in some unloved sectors such as US healthcare and consumer staples.

AI is a long-term theme, but at this stage, valuations are high for the bigger tech companies (Microsoft, Meta and Alphabet). Similarly, there are risks in the supply cycle, such as chip demand, which are making AI less attractive at this point.

Conclusion

As always, Morningstar is taking a long-term view with a strong focus on risk management. They continue to focus on valuations as a guiding principle throughout the volatility, allowing them to build and execute robust portfolios. Diversification, discipline and investor behaviour remain key to navigating uncertainty and staying on track.

If you have any questions about this wrap-up or about your portfolio, please get in touch. I look forward to speaking with you.

Signoff

Important Information

As noted previously, this document is intended to support your service proposition to clients and the commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

From the desk of the CIO: Staying invested pays off

By Matt Wacher, Chief Investment Officer, APAC

Key takeaways

- Staying invested pays off

- S.A pay-to-play policy becomes more prevalent

- Tariff impacts ahead

- Dig deeper and diversify

Investors have benefited from staying invested this year as markets climb a wall of worry. Returns year to date are above long-term averages vs inflation rates and cash returns. As we’ve noted before, the global economy has turned out better than feared, with a rebound in today’s Artificial Intelligence leaders and big gains for the perceived beneficiaries of President Donald Trump’s reign. Stock prices have also risen in response to better-than-expected corporate profits in the face of potential slowing growth. Investors, like us, that look through the nose have benefited handsomely from this environment.

What next? Well, we think investors should expect US government action to continue to surprise and add to market volatility, now that ‘pay-to-play’ policy is being applied more broadly. What started with trade has spread to defence and now the treatment of individual companies.

With trade, foreigners pay Uncle Sam higher tariffs for the privilege of selling into the world’s wealthiest country, though in many cases this catches US companies too because their supply chains are global. Closer to home, the Australian government must now think of its policies not only in the context of what will benefit Australians, but also how they may be perceived in the US. Australian companies are being impacted in ways not comprehended even a year ago. News this week that Australia Post will no longer deliver their goods to the US market, due to the complexity and cost of managing the administration of tariffs on small goods has shaken small Australian exporters, with one major sales channel all but disappearing.

With defence, the price is the cost of buying US manufactured weapons that might have been provided by the US directly via alliances. For example, $1bn will be spent by Netherlands, Sweden, Norway and Denmark to support Ukraine1. In Australia the cost of purchasing US submarines may or may not become more expensive.

With companies, there is now the precedent of explicit payments to get around existing restrictions. Examples include Nvidia and AMD paying 15%2 of their revenues from sales of chips and semiconductor exports to China. It’s an echo of the shift away from rules-based global trade, so backroom bargaining may matter more, though it can of course also be rapidly reversed.

For investors, this is not good news, as it reduces transparency and increases uncertainty, but it does not fundamentally change the longer term economic and market outlook. The biggest impact of ‘pay-to-play’ is the higher tariffs that will, mainly in the US, weaken economic growth and boost inflation, given just how much tariff rates have risen (from 2.4% in 2024 to 18.3% as at August 1 2025 based on US weighted average tariff rate3). But effects are diluted by exemptions and exclusions, the offsetting disinflationary impact of AI adoption and the impacts of changes in interest rates and tax rates. Morningstar’s base case is 1.3% economic growth and 3.2% inflation for the US in 2026, followed by higher growth and lower inflation.

After the mid-year rally, emerging markets still offer better prospects than most developed markets though there are pockets of value such as US smaller companies, beaten up healthcare and consumer staples companies, communication services and the UK. We have been taking profits on China as share prices have risen on the back of firmer economic and profit fundamentals and growing interest from foreign investors. Latin America and Korea both continue to stand out as undervalued opportunities that are in the earlier stages of their recovery. Australia, not unlike the US, looks expensive in aggregate, mainly driven by financials. However, there are some opportunities beneath the surface.

Overall, investors are well served in this environment by digging deeper and diversifying to generate and hold onto returns. We continue to leverage heavily on Morningstar’s bottom-up company research to assess the most likely impact of abrupt changes in US government policy and finding where value lies. Portfolios remain broadly diversified to reduce the risk that come with highly concentrated markets and the potential for shocks from policy changes.

Source: (1) Financial Times, (2) Morningstar Equity Research, (3) Morningstar

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Should Your Clients’ Risk Profile Align With Their Risk Tolerance?

A suitable risk profile balances risk preference with the risk necessary to meet a particular goal.

Pop quiz: What’s the difference between risk tolerance and risk profile?

Risk tolerance and risk profile are often used synonymously yet are distinct constructs when determining suitable risk levels for your clients. On the one hand, our risk tolerance is a psychological trait—it’s how we feel emotionally about taking risk, which tends to be relatively stable over time. On the other, a risk profile describes the amount of investment risk that’s suitable in the pursuit of an investment goal.

Clients may have different risk profiles for different goals, whether it’s retirement planning, for example, or funding a child’s education. Each risk profile is shaped by:

- the investment objectives of the goal

- the circumstances related to the goal

- the personality of the client

Some components vary on a goal-by-goal basis. For example, a client’s capacity to take on risk and how much risk is required to achieve the goal are influenced by the amount of money needed, time horizon, cash flow, liquidity need, and whether the goal is high or low priority.

Other components are personal in nature and reflect an individual’s general underlying comfort and preferences across all investment goals. This includes risk tolerance, financial knowledge, investment experience, and nonfinancial preferences.

The investment risk profile is the aggregate treatment of all these components.

Balancing Goal-Related and Personal Components to Create a Risk Profile

Break down the process of developing risk profiles, so clients (and you) are not overwhelmed by all the moving parts.

Identify each component separately so they can be understood and compared. Goal-oriented components are best defined, stimulated, and stress-tested using robust cash flow modeling where possible. You can kick-start the process with a rough figure and build precision as the client gets comfortable discussing their goals and expectations. On the other hand, personal components like risk tolerance are best measured with validated tools for accurate and reliable results from the get-go.

Account for each component and bring them together in a consistent manner. Effective trade-offs can only be made when the components can be compared on the same scale. Ensure you have a framework for how you map the personal components to the goal-oriented components and be able to demonstrate impact and consequences. For example, how might you demonstrate to clients the impact of low risk tolerance or other adjustments for personal preferences? You want to be confident the framework is defensible and can be applied across different scenarios.

Clarify options, illustrate potential outcomes, and facilitate trade-off discussions. Toggling between different balances of personal and goal-oriented components means clients will be faced with multiple possible risk profiles. Conflicts between alternatives and differences within households are best solved with what-ifs or scenarios modeling. Visualizations can help clients engage with different possibilities and stay committed to the agreed plan.

How Risk Profile Can Differ From Risk Tolerance

Let’s consider a client with a high tolerance for risk who has three goals: an education lump sum due in three years, retirement living expenses in 15 years, and a “nice to have” boat purchase in five years. This simple scenario illustrates the possible range of suitable risk profiles for a single client when their portfolio is bucketed for specific goals.

In each case, the client’s risk tolerance is on the high side, but the capacity for risk varies with the circumstances. The short time horizon for necessary education expenses calls for a conservative risk profile for that bucket. A moderate risk profile is appropriate for the retirement bucket. And an aggressive risk profile might be suitable for the boat bucket, even considering the short time horizon because the goal is low priority.

Alternatively, an aggregate risk profile could be assigned to the whole portfolio by considering how the various components average out across the portfolio.

In any case, it’s prudent to confirm any discrepancies between risk tolerance and risk profile selection with clients. Though clients may need to take on more risk than their risk tolerance assessment indicates, advisors must ensure that clients are doing so knowingly, alternatives have been considered, and not so much risk is being taken on that the client is likely to panic in a major downturn.

By helping clients develop risk profiles that reflect both them and their goals, financial advisors can help clients reach those goals and stay committed to their financial plan throughout the process.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

From the desk of the CIO: Squeeze the lemon dry

By Matt Wacher, CIO, APAC

Key takeaways

- Lower interest rates making cash less attractive than bonds

- Strong emerging market performance

- Knowing when to hold or to fold

- European luxury sector is undervalued

Away from the glare of tariffs, one thing is very clear about 2025: interest rates are coming down, including here in Australia.

Across most of the developed economies, central banks are making money cheaper and decreasing the return available from cash. Interest rates remain above inflation rates in most countries such as Australia, and the pace of rate cuts might have been faster but for the uncertainty about tariff effects. But inflation is not the only potential outcome of tariffs. Weaker economic growth and subdued household spending are likely to give central banks a greater sense of urgency for further rate cuts as we move through 2025.

Source: Reserve Bank of Australia, Federal Bank of St.Louis, Morningstar

Since the beginning of this year, the Australian treasury yield curve has steepened, driven by a decline in short-end yields while the long-end has remained elevated. Long term Australian government bonds offer a decent extra return vs cash and inflation, supporting income seeking investors and those transitioning to retirement seeking shock absorbers to deal with bumpy markets.

After the tariff-induced hiccup in early April, equities have resumed and continued their rally, with 2024 superscalar stars back in the spotlight. The easing of inflation fears and bond yields not rising further has no doubt supported these more highly valued companies and perhaps reduced fears of large inflation/growth shocks from tariffs. At current share prices, the valuation of US equities in aggregate are less attractive than other regions, and we continue to favour opportunities elsewhere that offers better reward for risk.

What’s been notable this year is the outperformance of emerging market equities, such as Korea and China tech. For example, the Morningstar China Index was up 35% for the last 12 months to 30 June. The stimulus measures announced in September last year may not have been a ‘bazooka’ one, but they signaled a shift towards more forceful monetary and fiscal support aimed at lifting the Chinese economy out of its slump. Earlier this year the market was surprised by the ‘DeepSeek moment’ for the pace and capabilities of China’s AI development, leading investors to recognise the relatively cheap valuations of Chinese tech companies versus their US peers. We have held higher quality China technology companies, such as Alibaba and Tencent, in Morningstar multi-asset portfolios for the compelling valuations they were offered prior to the rally.

Getting the most out of investment opportunities is a key element of successful investing, knowing what to invest in, when to buy and when to sell. Overstaying your welcome can lead to large losses but cashing out too early can be just as impactful in terms of missing out on extra gains.

Looking back over the past 40 years, the classic signs it’s time to sell include asset prices rising a lot over an extended time frame to levels that are very high vs metrics like cashflows, dividends and asset values, universally bullish investors with outsized exposures and unsustainably high sales and profits. Examples include telco, media and technology companies in late 1999, emerging market and financial service firms in 2007 and mining companies in the early 2010s during the commodity boom.

Conversely, it’s been better to hold or even add to exposures, when investors are fixated on the downside, fundamentals are improving from a low base, asset price gains are small over longer horizons and prices reflect low rather than high expectations of future profits. Here examples include oil and gas companies in 2020 and IT companies in 2003.

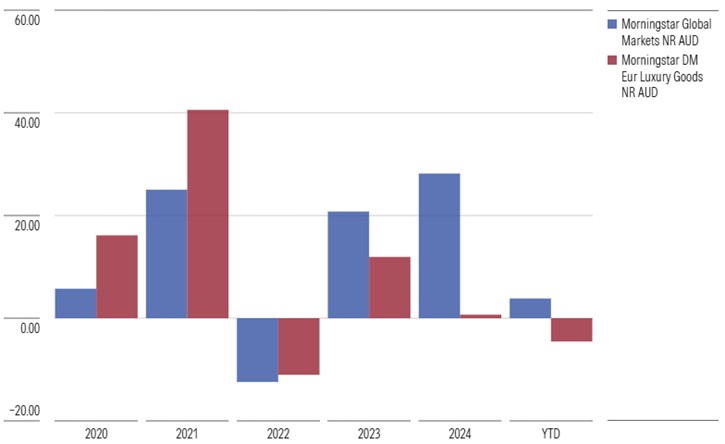

Consumer companies have been facing investor skepticism, with negative sentiment due to noisy macro backdrops and bearish expectations. Over the past two and a half years, the Morningstar Developed Markets Europe Luxury Goods Index has notably underperformed the broader Morningstar Global Markets Index. This underperformance reflects multiple headwinds, including persistent cost-of-living pressures in developed markets, a muted recovery in Chinese consumption, and growing uncertainty surrounding tariffs.

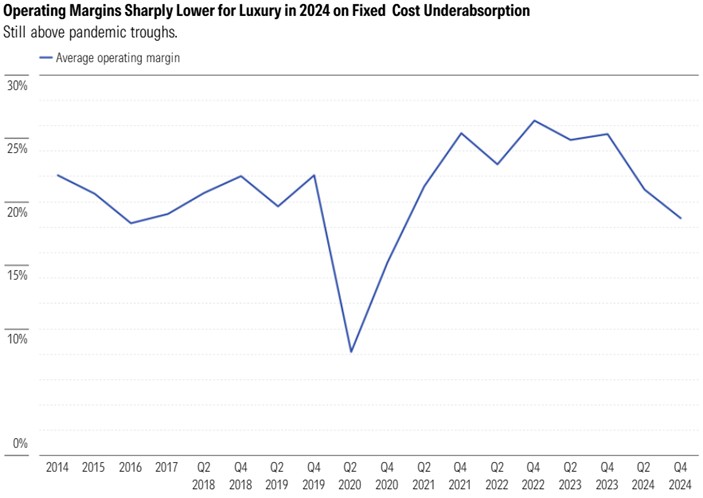

At Morningstar, we believe the luxury sector presents compelling long-term investment opportunities. Valuations of the industry have become increasingly attractive, with certain companies trading at discounts that we view as overly punitive relative to their fundamentals. While near-term demand remains subdued, we do not expect this softness to persist indefinitely. Long term investors should look through the current cyclical weakness and focus on the sector’s enduring fundamentals. Most luxury companies possess strong branding intangibles and pricing power, although under the current macro environment, their high fixed cost structures create near term pressure on profit margins. In our view, disciplined cost control, and the eventual demand normalisation, should support margin recovery over time.

Along with China tech, European luxury is an example of the potential for gains from specialised research and contrarian risk taking. Getting the most out of opportunities while staying diversified remains key to navigating this period of rapid change.