Adviser-to-client template: Minimising the effects of the investor return gap

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

“The investor’s chief problem—and even his worst enemy— is likely to be himself.” – Benjamin Graham

Something I’ve come across a lot in my day-to-day conversations is the concern that short-term market moves can derail an investor’s goals – or indeed that short-term wins dictate future success. While market corrections can be scary, investing, at its core, is about the long game. Patient investors are rewarded, while those who take the short-term view, more often than not, sabotage their financial futures. This can show up in a few ways, whether that’s by chasing yesterday’s winners, attempting to time the market and therefore buying and selling assets at the wrong times, such as pulling out during volatility, or succumbing to headline noise about the latest ‘hot’ stock.

Understanding the impact of the investor return gap

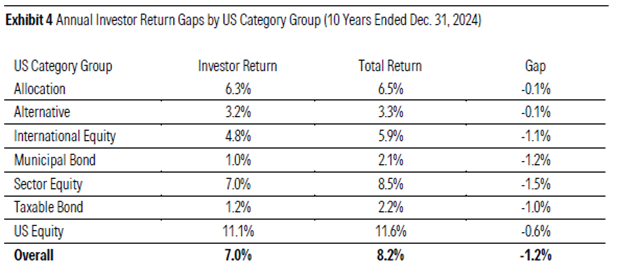

It’s these types of moves that can result in what our investment manager, Morningstar’s, behavioural finance team refers to as the ‘investor return gap’. A study recently completed by Morningstar in the US was found to ‘estimate the average dollar invested in US mutual funds and exchange-traded funds earned 7.0% per year over the 10 years ended Dec. 31 2024 (“investor return”). Sound all right? Well, that’s about 1.2 percentage points per year less than these funds’ 8.2% aggregate annual total return over that time, assuming an initial lump-sum purchase.

In practice, that 1.2 percentage point investor return gap, which is explained by the timing and magnitude of investors’ purchases and sales of fund shares during the 10-year period, is equivalent to around 15% of the funds’ aggregate total return. Which is to say, it’s a gap that most investors would prefer to pocket rather than sacrifice. The table below shows what this looks like by category group.

How do you mitigate this gap?

Put that way, the prospect of the investor return gap is a scary one. But understanding how short-term or panicked moves can set you back is also a useful tool for ensuring that a long-term view is crucial to financial wellbeing. Familiarity with the inevitable fluctuations of markets is also something that can alleviate stress when these conditions occur. Morningstar’s portfolios are constructed to withstand tricky market conditions that prompt these sorts of loss-aversion behaviours, providing a margin of safety. By sticking to your plan, staying invested, and having your money compound, you’re already well on your way to minimising the effects of the investor return gap.

If you have any more questions about how your Morningstar portfolio is positioned, or if you’d like to walk through some common behavioural responses and how to alleviate them, I’m always happy to talk. I look forward to chatting soon.

Regards,

Adviser

Important Information

As noted previously, this document is intended to support your service proposition to clients and the commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use.