![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

“Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.” [1]

— Warren Buffett

Buy Low & Sell High, The Right Way

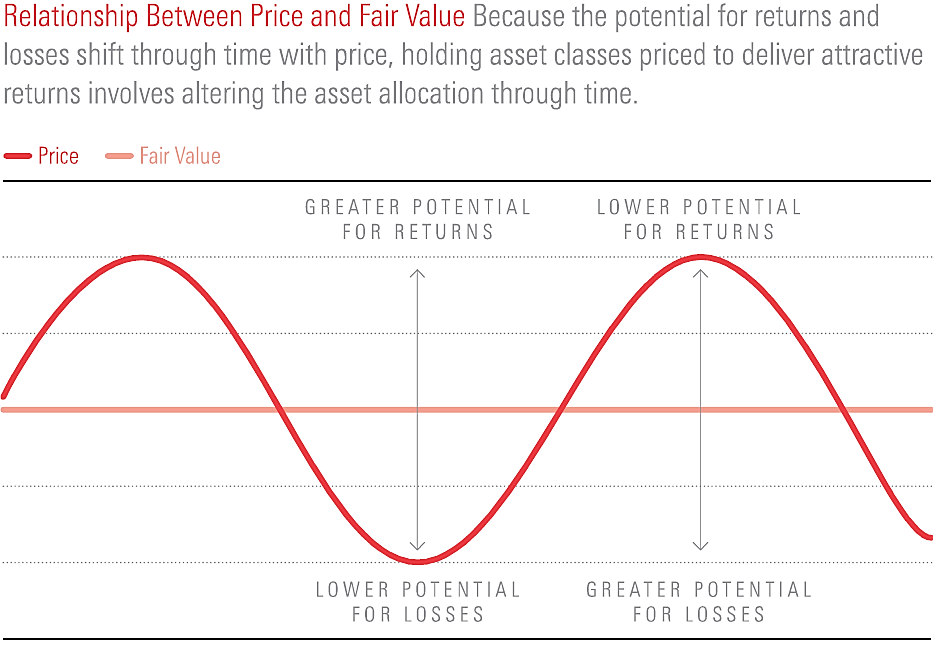

Let’s say you own a great business today and the price falls by 40% tomorrow. Should you buy more of it? All else being equal, you would be foolish not to buy more as long as your conviction in the intrinsic value of the business remains intact. Yet, the process of buying high-quality businesses at low prices is beset with behavioural challenges and something every investor must consider carefully.

Key Takeaways

Identifying Risks When Buying Stocks

Some of the key risks to stock investors tend to cluster around the following situations:

The other, which is likely to have relevance today, is when assets are still expensive. This may not fit the classic definition of a value trap, but an asset going from extremely expensive to moderately expensive is unlikely to make a good investment, even if the price has fallen meaningfully.

Lessons from a Classic Collapse

Some companies can appear strong on face value but tumble into structural decline. Take Kodak for example, where many investors in the 1990’s never anticipated the progression of digital cameras, nor that Kodak would be left behind in that progression. Buying in the dips would have been a terrible idea for most investors, as you would have continually bid up this exposure only to find it halve, halve and halve again.

Underpinning the above risks, a key challenge is that early and wrong can sometimes be indistinguishable in the initial stages of an investment. An investor who is early would likely prefer to increase their exposure as the probability of a turnaround increases (much like a poker player should). However, if that investment becomes wrong (a value trap), they should consider accepting their losses and moving on. It is entirely possible to be both early and wrong if the nature of the asset changes over time.

This is also a warning that cheap assets can get even cheaper, so it isn’t enough to simply buy cheap companies. We need to ensure the quality of their cashflows are sound and that they have durable advantages that allow for the benefits of compounding. For example, if a poor-quality investment falls by 20%, but could fall a further 30%, 40% or 50%, we likely want to avoid going all in.

In principle, if we want to buy high-quality businesses at prices below their intrinsic value, we must conform to the idea that we might be early to the party. After all, you are likely buying the investment today because it is unloved and no one else wants it (yet). By undertaking this exercise, there are no guarantees someone will want it next week, month or even year. Hence the reason value investors often cherish the word ‘patience’.

Our Process When Buying Stocks

Beyond rigorous research and risk management, we face an undeniable truth: buying high-quality stocks at a discount is not easy and we’re very unlikely to get the perfect timing on an investment. If we do, it will require a lot of luck. However, this doesn’t mean we should ignore the opportunity as valuation-driven investors.

To bring this to life, we consider the following as an important checklist. The idea behind this structure is to reduce the likelihood and magnitude of any mistakes, while giving ourselves the best chance of capturing value for our clients and delivering strong long-term returns:

A Buying Checklist

In summary, we like buying into weakness, but only when it makes sense to do so. To our way of thinking, the only way to know if it makes sense is to conduct rigorous checks before every buying decision (such as the checklist above). The key is to leave emotions like fear or greed aside, instead focusing on delivering long-term returns that can help investors achieve their goals.

[1] Source: Berkshire Hathaway 2008 Shareholder letter

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.