![]()

Receive investment insights straight to your inbox:

By clicking subscribe, you are

agreeing to our Privacy Policy.

Kyle Cox, Investment Analyst, EMEA

Dan Kemp, Chief Investment Officer, EMEA

Key Takeaways

“Stay the course” is a nautical phrase that has been popularised by world leaders, primarily in the

context of battle, according to Wikipedia. According to Stewart Alsop’s 1973 memoirs of a conversation

with Winston Churchill, the British prime minister contemplated towards the end of World War II:

“America, it is a great and strong country, like a workhorse pulling the rest of the world out of despond

and despair. But will it stay the course?”1

We ask the same question today of investors, after what has been an emotive period for financial

markets. From trade wars to Brexit, North Korean tensions to Italian political turmoil, we’ve had plenty of

noise to deal with. So, what do we mean by “staying the course”? It is not always about sitting still

(even though this is often the easiest path to investing success), but rather, to focus on the goal that you

set in the first place and ensure your behaviour aligns with it.

Let’s face it, investors too often redirect their focus from the destination to the journey. Much like in

other walks of life, we can lose focus, making us susceptible to capitulation or giving up at the exact

moments when we require fortitude and resolve. That is, investors are hard-wired to be procyclical,

chasing the winners and selling out of the losers because of a yearning to make money work harder for

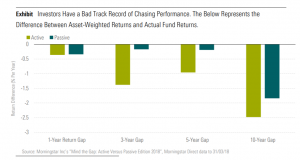

us. This is not just conceptual, we can see it directly in the fund flow numbers.

Therefore, it is vital that as investors we remain vigilantly aware of how animal spirits can drive irrational

decision-making, and that we adopt a reasoned framework for investing. Behavioural errors can wreak

havoc on long-term portfolio returns due to excessive and unjustified turnover.

A Step-by-Step Guide to Staying the Course

The best thing an investor can do when contemplating change is to reflect on their goals. Would the

investment change align with the original investment plan or strategy for reaching well-defined goals?

The key question to ask is whether anything has fundamentally changed since setting the original

strategy or whether it’s just that the client is disappointed with the progress towards goals.

How We Think about Staying the Course

As professional, multi-asset investors, we focus on the investment objective, always bearing in mind the

opportunity costs and risks. We also write down a balanced thesis that ensures we remove any emotion

from our decision-making.

In this sense, staying the course is not idle or passive, but rather about staying aware. Some investors

may look at a recent period of lean returns and, with a hindsight bias and the herd mentality at play, will

fear for the future. Many will further justify to themselves that reward for risk is simply not sufficient

and will consider a change in strategy. This thinking is usually well intentioned, but it is dangerous and

must be thought through with a long-term perspective.

Staying the Course vs. Timing the Market

Investing, like many things, often involves taking the thorns with the roses. Over dozens of years and

through all investment literature there is one golden thread–the evidence clearly favours time in the

market over timing the market.

This can be illustrated in various ways, but one of the most compelling is to simply reflect on the cost of

missing the best days in the market. We show this below, illustrating how an investor can hamper the

likelihood of reaching their goals by overzealously trying to time the market.

1‘A Stay of Execution’ by Stewart Alsop (1973)

![]()

By clicking subscribe, you are

agreeing to our Privacy Policy.