From the desk of the CIO: Overreaction is never the right reaction

Disliking risk is only human but overreacting to short-term market noise usually does more harm than good.

By Matt Wacher, Chief Investment Officer, APAC

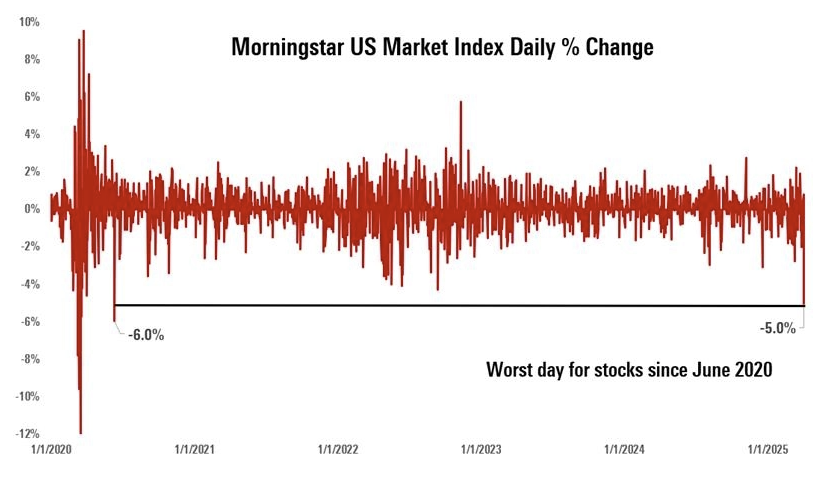

As President Trump stood on the White House lawn to announce sweeping new tariffs for almost every country in the world, the initial reaction was one of shock and uncertainty around the potential economic effects—which almost immediately drove widespread market volatility.

In fact, on 3 April 2025 markets experienced their worst day since the height of the COVID pandemic and the Morningstar US Market Index fell 5%, its worst single day since June 2020. In the 3 trading days between 3 April and close of 8 April the Morningstar US Market Index fell 12.4% and the Morningstar Australian Market Index fell 7.2%.

Figure 1: Daily US market moves from April 1 to April 14 2025. Source: Morningstar Direct.

We all have embedded biases and risk aversion, and not wanting to lose money is one of them, therefore the natural reaction of any investor is to metaphorically run for the hills—or practically exit the markets and go to cash. This overreaction is invariably the wrong thing to do.

It didn’t take long for investors to find this out. On 9 April 2025 President Trump announced a 90-day reprieve for most countries and, bang, the Morningstar US Market Index was up 9.6% and Morningstar Australian Market Index was up 4.6%. While the temptation to overreact is high, history shows that staying disciplined through market shocks is key to long-term investment success.

As the chart below shows, April has been a bumpy ride. We’ve seen markets dip and rally in a direct response U.S. to President Trump’s on again off again tariff announcements. The uncertainty, potentially more than the tariffs themselves, has meant markets have remained volatile with the fallout continuing to alarm investors.

Figure 2: US and Australian daily equity returns April 1 to April 15, as measured by the Morningstar US Market NR USD and Morningstar Australia NR AUD. Source: Morningstar Direct. Note: Past performance is no guarantee of future results. Indexes are not directly investable.

At first glance this is understandable—in the words of Morningstar’s Chief Economist Preston Caldwell: “This kind of regime shift is so unprecedented the historical data and models derived there from are only a best guess.” This is because when you put up trade walls between multiple countries, you hurt the efficiency of all of them. And in doing so, there will likely be cascading effects. We don’t exactly know what those effects will be, but if you’re a business that’s unsure about things, you might pause hiring because you’re questioning your profitability—which has downstream effects that can hurt employment and ultimately flow through into less consumer spending. If companies can’t plan and seem to not know what to do, how can investors make appropriate decisions.

However, while economies may undergo some structural change and some companies may come under pressure economies and the firms that drive them have proven remarkably resilient delivering reasonably consistent returns to investors over the long term. So potentially the ‘noise’ that we are experiencing around theses tariffs is just that and investors must resist the inclination to overreact stick to their investment process and seek out the opportunities presenting to investors who stay the course.

Diamonds in the rough?

Given the context of the tariffs some of the opportunities may seem scary. At face value, it certainly appears that US apparel and furniture retailers were dealt a major blow. We can see the impacts of the tariff changes on some of these companies. Most of their supply chains are overseas. Nike, for example, does nearly 50% of its manufacturing in Vietnam. Because of that, these stocks came under significant fire.

Figure 3: Selected US apparel stocks daily return on April 3. Source: Morningstar Direct. Note: References to specific securities not an offer to buy or sell. Past performance no guarantee of future results.

These companies are a microcosm of a bigger issue—companies scrambling to figure out what to do next and how to invest. Imagine the conversations happening at the highest levels of these companies: if they move manufacturing to other locations, it could take years to build and get production ramped up to the required levels.

In short, there are so many unanswerable questions at this point, and markets never wait around for the answers to develop—they start pricing in an unknowable future immediately.

That’s what’s being observed in stock prices. Markets and businesses can remain resilient through a lot, but they hate uncertainty. Uncertainty removes predictability and confidence. That’s what we’re seeing right now.

However, these companies have the potential to be great long-term investments. If investor behaviour (in this case, the urge to get out of the market) has pushed prices to extremes, then it’s a possibility we can take advantage of this mispricing. It won’t always be the case, but if we focus on the fundamentals of the company and shock those fundamentals with a range of onerous scenarios then we may well find some diamonds in the rough. Often a company being less bad than the market is pricing leads to exceptional returns—and we then take advantage of the markets’ overreaction.

Why it remains important to block out the noise

At Morningstar Investment Management, we focus on the long term and our valuation-driven approach allows us to block out the noise we’re hearing from every angle. While the macro environment can seem scary and overwhelming, we continue to zoom in on the fundamentals. We are guided by an investment process that always considers the long term, prioritises resilient portfolios, and prepares for volatility knowing that it’s an inevitable part of investing. As Warren Buffet says, ‘be fearful when others are greedy, and be greedy when others are fearful’. When others overreact, we like to use that opportunity to be greedy.

We focus on end investors who are not day traders punting on every market move—most are people investing for a happy retirement. For that reason, it’s important to provide context on what it means down the road if they were to overreact in the moment. In scenarios like what we’ve recently experienced, overreaction can feel like the comfortable thing to do.

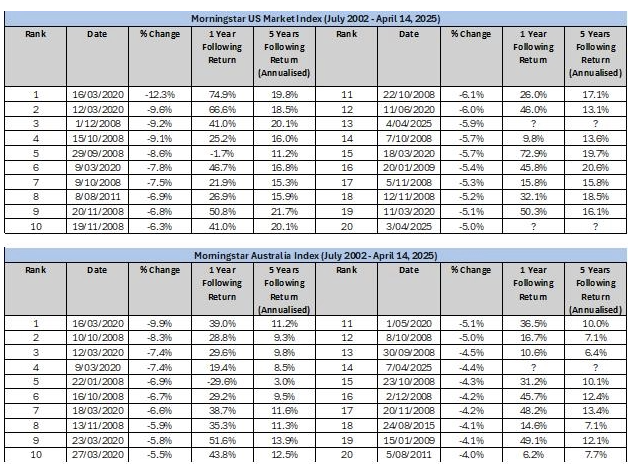

However, we counsel not to be swept up in the frenzy. April 3 was a bad day, but it barely cracked the top 20 worst single days for markets since 2002, coming in at number 19. The charts below show 20 largest 1-day % declines and the subsequent bounce backs for the US and Australian markets.

Figure 4: US and Australia historical returns after large short-term falls. Source: Morningstar Direct, return data represented by the Morningstar US Market NR USD and Morningstar Australia NR AUD. Past performance is no guarantee of future results. Indexes are not directly investable.

Each of these dates represents a point in time where investors likely overreacted, and the long-term consequences were severe in terms of opportunity cost as markets ended up higher in all cases. This list is littered with times when overreacting felt right: COVID, the global financial crisis, the European debt crisis, and so on. Each of these dates represents a point in time where a number of investors likely overreacted, and the long-term consequences were severe in terms of missed opportunities as markets ended up higher in all cases. Morningstar’s behavioural science team has investigated this reaction extensively in their Mind the gap research, which has found a 1.1% annual estimated return gap due to mistimed purchases and sales when investors get spooked and withdraw from the market. 1.1% per annum can be a huge amount when compounded over time.

Being valuation driven investors at Morningstar means that we can be very countercyclical when markets are behaving a little irrationally. We can be buyers when sellers are desperate to sell, and we are happy to sell when markets get a little exuberant. Volatility in markets like we experienced over the first two weeks of April 2025 has allowed this type of investment process to do what it does best–rebalance. In fact, by rebalancing, we’ve been able to take advantage of opportunities to reduce assets that had done well and redirect that capital towards the assets that have been underperforming. This kind of rational investor behavior won’t make Page 1 of the Australian Financial Review but it goes a long way toward potentially increasing future returns as the portfolio moves towards more undervalued assets. It’s not flashy, but it is a tested framework that rewards patient investors.

Put simply, the tariffs saga is messy—and that will likely remain so. A full implementation of tariffs could have severe economic consequences, and we acknowledge that. However, like every other period on the list of the 20 worst days for markets, we eventually recovered to new all-time highs. We have already seen the market rally in response to this dip, and will continue to monitor the situation. What we do know is that markets tend to move up over time, and while we can’t predict exactly when this will happen, we remain optimistic that this pattern will persist over the long term.

We often say that volatility is a feature, not a bug, of investing. And it bears repeating: overreaction is never the right reaction.