Menu

Menu

How Advisers Can Differentiate Themselves From Generative AI Advice

While artificial intelligence tools may replace ‘limited scope’ advice, advisers must do more to stay relevant.

Applications enabled with generative artificial intelligence capabilities may soon become the leading source of retail investment advice. Deloitte forecasts usage shooting up from about 10% in 2024 to 78% by 2028.

This might seem like a scary number for financial professionals, but Deloitte notes that investors’ usage of financial advisers will only drop by about 4%.

In other words, generative AI won’t replace financial advisers altogether. But it may replace “limited scope” advisers—those who only give investment or transactional advice.

That means that to stay relevant, advisers should ensure that they offer more than this limited scope and include holistic, comprehensive advice.

The term more carries a lot of weight here and may not be too helpful on its own. In our research, we defined this term by asking investors what they value in a financial adviser using different measurement strategies.

What we found is good news for advisers. It turns out that much of what investors value in a financial adviser still cannot be fully replicated by generative AI.

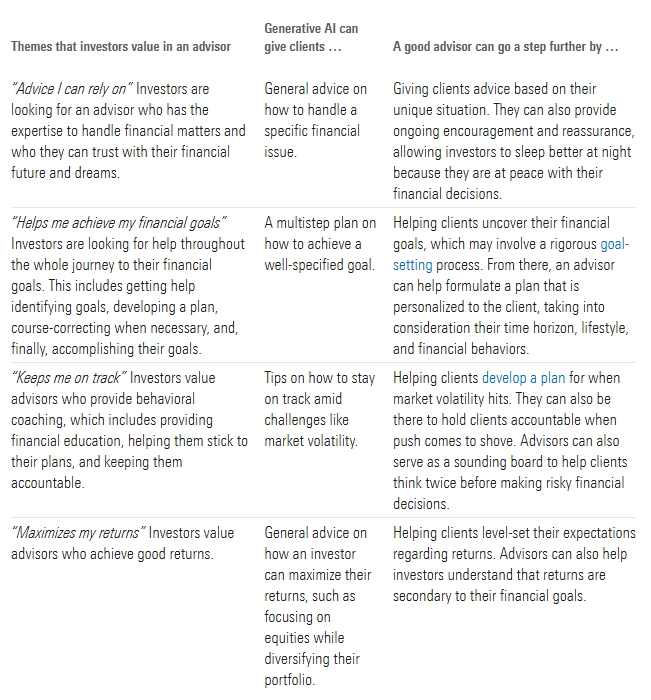

In the diagram below, we illustrate what this looks like.

- First, we asked clients what themes they value in an adviser. In the first column, we map out the four broad themes that we heard most frequently.

- The next column explains how gen AI, in its current state, can manage needs related to these themes.

- The final column shows how advisers can build on the outputs of gen AI, and the value they can provide by incorporating the human element of financial advising.

Wrapping Up

Although generative AI has immense potential in the financial advice sphere, our research indicates that investors greatly value the soft skills that a good financial adviser can bring to the table. Generative AI does a great job of spitting out answers, but it still can’t replicate the social connection inherent in good adviser-client relationships and the quality of advice that can result.

To differentiate themselves from generative AI applications, advisers should consider devoting more time to building a strong relationship with clients—and maybe even using gen AI to free up more time to spend with clients.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

How Financial Advisers Can Improve Their Relationship With An Unresponsive Client

One way to demonstrate your interest in their specific needs.

Every adviser, no matter how experienced or successful, has had to deal with an unresponsive client.

You may have pulled out all the stops—sending them a reminder email, shooting them a text, giving them a call, or even mailing them a handwritten letter—all to no avail.

Whether the client was always a bit flaky or has slowly disengaged over the years, advisers may feel like they’re at a loss. If you can’t reach a client, how can you make amends and improve your relationship to help reengage them?

Diagnosing the Problem Is Difficult

To state the obvious, it would be great to understand what is prompting the lack of responsiveness so you can intervene accordingly. Unfortunately, this is close to impossible given that the client is not responding.

This doesn’t mean that all hope is lost—it just means we have to calibrate our expectations accordingly. Chances are that a client’s unresponsiveness has nothing to do with you and is entirely out of your control. The client may be going through something personal and can’t bear to think about their finances. Who knows?

That said, there’s a chance that the client just needs more of a nudge to reengage with their finances and with you. With this level-setting in mind, one place to start is to change the type of messaging you’re sending to this client. This means incorporating the softer side of financial planning.

How to Try a Different Approach

In our research, we find that investors value advisers not just for their expertise, but also for more psychologically driven reasons. That means investors valued an adviser who helped them better understand their financial goals, made them feel like they had a partner to navigate financial decisions with, and gave them the peace of mind to sleep better at night.

Given these findings, advisers can rework their communication to unresponsive clients in a way that shows the ability to provide the type of advice that can convey these emotions. This task may be easier said than done, so we recommend relying on ready-made exercises that are easy to send via email.

One place to start is by sharing a three-step checklist that we created to help people uncover their true financial goals. Step 1 asks investors to write down their top financial goals off the top of their heads. Step 2 presents investors with a master list of financial goals and asks them to consider each one. Step 3 instructs the client to write down their top three financial goals again, considering their initial answers and the goals in the master list. The key to this exercise is the use of a master list, which aids investors’ decision-making when trying to identify their financial goals, which is a more difficult decision than it may seem.

An email that incorporates the checklist can look something like this:

Dear Client,

Hope all is well.

This is a reminder that our next check-in is coming up on 1/16/2025 at 11 a.m.

During this check-in, I will provide recommendations based on my analysis of your accounts and holdings.

We will also have plenty of time to discuss any changes necessary for your plan. To guide this discussion, I have attached a quick goal-setting exercise for you to complete beforehand. The exercise will help us both get a better idea of any changing priorities or goals in your life that could help us better serve with your financial plan.

All the best,

Adviser

This email may start like any other typical cold reminder email the unresponsive client has received, but some clients may be intrigued by the goal-setting exercise.

Not only does this addition show that you are interested in the client and motivated to better understand their specific needs, but the exercise may also help the client to better understand themselves. In our research, we found that up to 70% of people changed at least one of their top three goals after going through this exercise.

We’ve heard from advisers who have used the checklist this way and that many investors responded positively. Of course, some clients continued to be unresponsive, but others reengaged. These advisers found that the exercise started new conversations and helped them identify new ways to serve their clients.

Wrapping Up

In some cases, an unresponsive client may be out of your control because their lack of communication may have nothing to do with you or your services. However, some clients may benefit from a different approach to your typical email.

Next time you have a client who, despite your best efforts, no longer interacts with your practice, try communicating in a way that taps into the softer side of financial planning.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Risky Play: Trading Platforms Are Gaming Investors Into Bad Decisions

Investors may be nudged to take more risks.

It has never been easier to trade, thanks to ubiquitous online zero-commission trading platforms. The US online trading market is projected to exceed $4 billion by 2029.

On the one hand, this is great news. Stock ownership is positively associated with building wealth and financial awareness, and online trading platforms are leading the charge to find new ways to attract new investors. On the other hand, the introduction of gamelike elements such as leaderboards, badges, and points may be encouraging “gambling” behaviour and leading investors to take on riskier choices.

Gamified Trading

Trading platforms are incentivized through payment for order flow, or PFOF, and advertising revenues to keep investors engaged and trading more frequently.

To achieve these goals, not only have platforms made trading seamless, but they have also introduced gamelike elements to take the fear out of investing and entice novice investors. These features have the added benefit—for the platform, that is—of keeping users trading. The more you trade, the greater the trading value, and the higher your gains, the more positive reinforcements you get in the form of points, badges, and celebratory messages. The problem is consumers are getting caught up in playing the game.

Research shows that people can be negatively influenced by these types of features. Gamified elements are linked to more-frequent trades, speculative herding, and, subsequently, poor returns. Even more worryingly, these features are linked to riskier behaviours such as using higher leverage, trading larger amounts, and selecting riskier stocks.

In recent research, participants in a simulated gamified trading app environment were more likely to invest in risky stocks compared with those presented with a nongamified app. These participants were driven by their goal to win the game or move up the leaderboard, which prompted them to ignore their risk preferences and make riskier choices.

Gamified trading platforms are nudging consumers toward choices they otherwise would not make. Many investors may be distracted by the gamelike features that blur the lines between investing and gambling. In a UK survey, one participant stated that the app “feels more like a sports betting app.”

Gamifying to Invest, Not Gamble

Regulators in the UK, EU, US, Australia, and Canada are taking note, issuing new warnings on design features that may lead consumers to act against their own interests, regulating in-app prompts as advice, and even calling for a ban on PFOF. But until these concerns are addressed through the regulatory system, investors must protect themselves by being aware of how their own behaviours are affected by gamelike features.

When used properly, gamelike features have the potential to help investors. They can generate interest in sound investing and wealth building, even though the rewards may be many years away.

If implemented mindfully, nudges and gamified design elements can motivate actions that drive better outcomes for investors. Such elements include:

- Rewarding points for getting closer to target goals.

- Assessing risk preferences using robust tools rather than assessments that encourage consumers to associate investing with gambling.

- Sending reminders to contribute to savings plans.

- Creating virtual portfolios to simulate market movements and better understand risk and composure.

- Building communities to share advice and experience.

- Giving badges for completing learning modules.

Investors can have fun and make informed investing choices; the two are not mutually exclusive. While many trading platforms currently seem to be designed to encourage frequent trading and other risky behaviour, that does not have to be the case. These platforms have tremendous influence. If they use gamelike features properly to promote positive outcomes, they can transform retail investing for the better.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

How Financial Advisers Can Use Generative AI in Marketing

For advisers looking to use AI now to better serve their clients, our research gives a few suggestions.

Marketing may not be every adviser’s favorite part of their role, but it’s key to growing a business.

That’s why marketing efforts are a prime area for generative AI: They’re a core need for any business, but they can be time consuming. Generative AI is able to help advisers save time and effort here, and investors seem to be receptive to the technology’s use in this domain.

Our research showed that investors largely believe that marketing is an acceptable use of generative AI and that it did not negatively affect their reactions in terms of comfort and perception of their adviser-client relationship. They largely felt this was how technology should be used: to create generic content.

However, one lingering investor concern centered on lack of personalization or a true understanding of an adviser’s desired client base. In fact, concerns over generative AI interfering with personalization and human connection were reoccurring themes in our research.

Although investors are onboard with generative AI helping advisers become more efficient in menial tasks, they also believe that advisers should be careful that the technology doesn’t affect the adviser’s ability to give personalized advice.

How to Use Gen AI for Social-Media Marketing

One marketing tactic that our research suggests may be a good fit for advisers’ use of generative AI: social media.

Social media can be a powerful component of any business’ marketing strategy, whether it’s used to reach out directly to potential clients or stay top of mind for existing clients. And generative AI can help advisers save time and increase productivity when engaging in this area.

For example, say you just read this great post by Danny Noonan and want to share it on LinkedIn for your clients to see.

At this point, you can fire up your generative AI tool of choice and start refining your prompt. There are plenty of resources available on prompt engineering, which all agree on the importance of including as much detail as possible into your prompt.

Here are a few items to incorporate:

- Define the AI’s role. Explain therole you would like the AI to take on—that is, the point of view you’d like the content to be written from. In this instance, the role would most likely be a financial adviser.

- State your audience. Tell the generative AI tool whom you want to reach with this post. Are you speaking to your current clients? Are you trying to reach out to new clients? You can even try incorporating some demographic details here—say, if the post is intended to speak to Generation X prospective clients. However, be careful not to get too in the weeds of demographic details and not to include any actual client data. Our research shows that privacy is a chief concern of investors when it comes to generative AI.

- Define your goal for this content. What is the purpose of this content? Do you want investors to see you as a trusted expert? Grow your following and reach new investors? Build your online brand and voice? Explain that in your prompt.

- Explain the action you would like the AI to complete. Try to incorporate exact instructions for the post, like word count and structure. Also, don’t forget to specify to include a Call to Action for your audience, whether that be to reach out to you directly or engage with the post (for example, Like, Comment, or Share).

- Run the task multiple times. We all know generative AI can produce some lackluster results, so ask the AI to provide multiple iterations. Generative AI can incorporate feedback such as, “Make this a little more casual” or “Make this a little more urgent.”

Here’s an example prompt to get you started:

## Instruction ###

Act as a financial adviser speaking to an audience of individual investors. Your goal is to establish yourself as a trusted expert in financial planning and share pertinent information with investors regarding financial decisions. With this goal in mind, generate a LinkedIn post on the following text. The post should be less than a 100 words long. Be thoughtful, detail oriented, but approachable. Have a clear CTA at the end to message me directly. Generate 3 LinkedIn posts in total. Here is the text:

## Text ##

[Copy and paste text here]

With this draft in hand, an adviser can check the content for accuracy, revise the draft to incorporate their own voice, and make any other edits as needed. In this instance, generative AI has given the adviser the bare-bones content that they can then build off for their own content, essentially giving them a head start.

After trying a prompt for a few posts, feel free to change things up and see what works better for your goals.

For example, maybe ask the AI to write longer posts. That will help you see whether longer or shorter posts seem to connect with your audience better. Or try out different calls to action to see if getting more engagement on a post is more impactful than asking for a direct message.

Developing and testing out different prompts can help an adviser see what messaging and content is most effective while cutting down on the time it takes to develop each post.

The Value of Generative AI for Financial Advisers’ Marketing

Will generative AI solve all our problems and bring about world peace in 10 years? Who knows. Some people seem to think so.

But, for financial advisers looking to use generative AI now to better serve their clients, our research gives a few suggestions. For starters, our results point to the opportunity of using generative AI in creating marketing content. Not only are investors comfortable with this use case, but it’s a key area where advisers can save time and effort. Even so, advisers must be careful of how they use and incorporate generative AI output in their practice.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Does Tolerance for Risk Change in Retirement?

By Nicki Potts, Director of Financial Profiling and Planning

Do advisers need a new risk-tolerance tool to help their clients in decumulation?

Transitioning to retirement brings both excitement and uncertainty: The shift from accumulating assets to spending them comes with unique challenges. Are retirees different enough from nonretirees that the industry needs a different set of measurement tools to better understand them? A recent review of retirement income advice by the UK’s Financial Conduct Authority found no difference in how most firms handle risk profiling between the accumulation and decumulation stages. In turn, some advisers have wondered if there should, in fact, be a difference. Would their clients be better served by a distinctive decumulation-focused risk-tolerance assessment? The short answer: In my view, probably not.

The Nature of Risk Tolerance

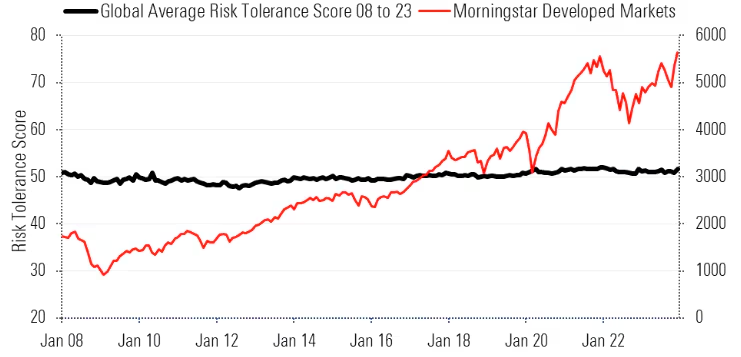

Risk tolerance, or how people feel about taking risks, is a psychological trait. Like many other personality characteristics, risk tolerance tends to be relatively stable over time. Even market conditions only have a small effect on peoples’ risk tolerance, as seen in the chart below. The Morningstar Risk Tolerance Questionnaire shows that the average risk tolerance score has been relatively stable from 2008 through 2023, regardless of whether the markets were up or down.

Investors’ Risk Tolerance Remains Stable Even as Markets Fluctuate

The global average monthly risk tolerance score as measured by the Morningstar Risk Tolerance Questionnaire from January 2008 to December 2023.

Stable does not mean immutable. Risk tolerance may change for some people, but large changes are not commonplace. For most people, risk tolerance varies little, even as they transition through life stages and events. When we compared risk tolerance scores over several years, we found that 69% of respondents’ scores varied only within 5%, and 90% of people had scores that varied within 10%. For the other 10% of people, risk tolerance varied greatly, but we don’t have a good way of knowing who will be more reactive over time, or what triggers these changes.

For Most People, Risk Tolerance Scores Don’t Vary Much Over Time

The global risk tolerance test-retest score difference as measured by Morningstar Risk Tolerance Questionnaires between February 2018 and June 2021.

Generally, we do find that risk tolerance declines somewhat with age, in aggregate. Retirees do tend to be a little less risk-tolerant than preretirees. But that’s not true for all. Further, age is just one of the many factors contributing to a client’s risk tolerance at any given time, as shown in the chart below. Moreover, these demographic characteristics still only have a low to moderate association with a person’s risk tolerance.

Demographic Factors Have Only a Moderate Impact on Risk Tolerance

Global average risk tolerance scores as measured by the Morningstar Risk Tolerance Questionnaire from December 2017 to June 2021.

Demographic patterns exist, but that doesn’t mean they should define how we measure something: Their reach is limited and complicated by other factors. It would be imprudent to have a different risk tolerance measure for each stage of life or circumstance—especially when the construct being measured remains the same. Consider measuring weight over a lifetime. People tend to gain weight as they age, but we still use the same bathroom scale to measure weight over time because what we are measuring is the same. The same goes for risk tolerance. The score may change some in decumulation, but the construct of risk tolerance (like weight with a scale) remains the same.

A Holistic Assessment of Risk Tolerance Is Accurate and Powerful

An approach to measuring risk tolerance that focuses only on the decumulation phase of investing would be of limited use. Tools designed for specific situations may inadvertently measure something specific to the situation itself, restricting the generalizability of the results. It would not be possible to discern if a detected change is a result of a change in a tool or a real change in risk tolerance.

There is little evidence that entering the decumulation phase drastically alters risk tolerance for most investors. Meanwhile, assessing risk tolerance holistically produces results that are valid across all financial contexts, whether we are making saving, investing, or drawdown decisions. Regular reviews and reassessments (about every two to three years) are essential to ensure any material change in a client’s profile is reflected in the financial plan. By measuring the same thing using the same benchmark, the results can be compared over long periods of time and across different circumstances. This means real changes for a client can be readily identified, discussed, and addressed. That way, we won’t miss the 10% of clients whose risk tolerance changes materially over time, nor will we erroneously detect substantial changes among the other 90%.

Compared with a decumulation-specific tool, a robust financial risk tolerance tool will best capture investors’ overall risk preference and serve as a benchmark across the long-term advice journey.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Don’t Make These Mistakes With Generative AI in Your Practice

By Samantha Lamas, Senior Behavioural Researcher

Investors think that generative AI has value—if advisers use it right.

Generative artificial intelligence seems to have limitless possibilities. However, just because generative AI can perform a task doesn’t mean it should do so—especially when it comes to financial advising.

If used properly, generative AI can help advisers take care of administrative tasks and allow them to spend more time on the softer side of financial advising, which is what investors value from a financial adviser.

But how do investors feel about all this? What do they think generative AI can reasonably do for their advisers, and what do they think it looks like to use generative AI “properly”?

In our research, we delve into this topic and provide guidance for how advisers can incorporate generative AI into their practice. In particular, we find some missteps advisers should avoid.

Mistake Number One: Using Generative AI for the Wrong Things

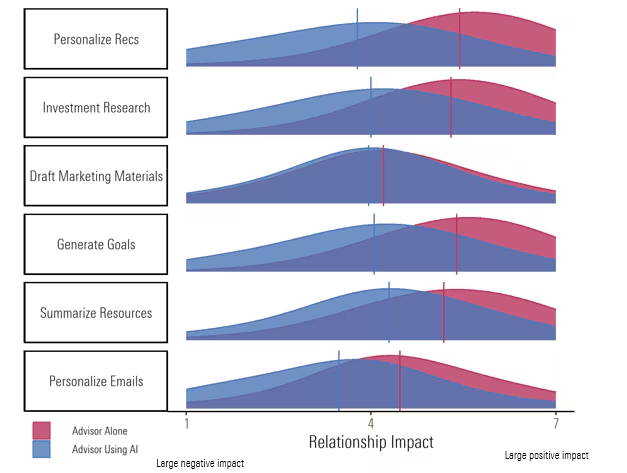

In our research, we presented one group of investors with examples of scenarios where advisers used generative AI. With a different group, we presented the same scenarios but did not mention that the adviser was using generative AI. For example, we posited to the first group, “Imagine a scenario where you are working with a financial adviser [and] … Your adviser uses generative AI when writing marketing content intended for your demographic.” And to the other group, we said, “Imagine a scenario where you are working with a financial adviser [and] … Your adviser writes marketing content intended for your demographic.”

We then compared people’s reactions, as measured by how each use case affected their relationship with the adviser. The graph below showcases the distribution of ratings for each of the use cases, with lower ratings reflecting a negative impact on the relationship.

Investors’ Reactions to Gen AI Use Cases

Simply put, reactions seemed to skew slightly less positive when investors knew that generative AI was used in the execution of a task. Still, most reactions tended to stay in the positive or neutral regions.

However, when it came to uses that required a personal connection or access to personal data, investors noted that generative AI use had a negative impact on the relationship. This included tasks such as “Providing personalized recommendations” and “Generating a personalized email.”

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

From the Desk of the CIO: Matt Wacher Shares What’s Top of Mind, November 2024

By Matt Wacher, CIO, APAC

Key takeaways:

- Market preparation is more effective than prediction for events like elections, ensuring portfolios are resilient to multiple outcomes.

- Historical analysis shows that starting valuations are more influential on long-term returns than the political party in power.

- Efficient markets quickly price in election-related information, making it difficult to profit by speculating on election outcomes.

Donald Trump has won the White House. After months of campaigning, we finally have an answer: The Republicans have reclaimed the White House and the Senate, while control of the House of Representatives remains uncertain.

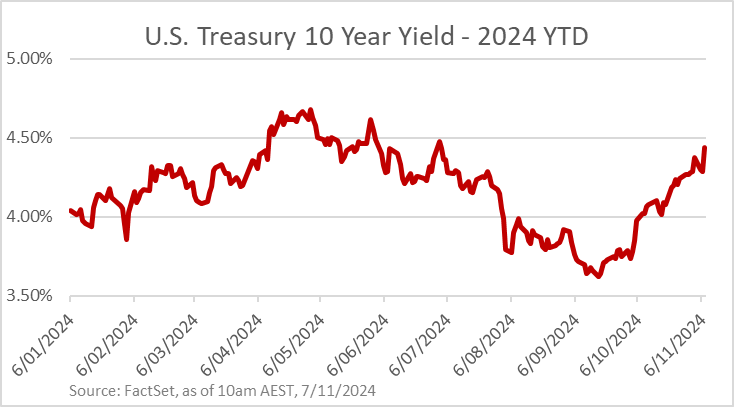

Financial markets have already reacted. US equity market is up by 2.5%, while European and Chinese stocks saw a decline. The US dollar strengthened against major currencies, including the AUD as Trump’s stance on tariffs is expected to put upward pressure on the dollar. Meanwhile, 10-year Treasury yields rose above 4.4%, reflecting the increased likelihood of more fiscal spending if Republicans control both the Senate and the House.

Our approach to this event has been the same as always: Prepare rather than predict.

How do we prepare? By striving to build diversified portfolios that are not overly exposed to any single outcome. As long-term investors, we evaluate assets based on the value of their future cash flows, recognizing that elections often have only limited long-term impact However, now that the election is over, we’re ready to respond. If markets overreact, our decisions will be guided by an assessment of long-term value rather than emotion.

Our analysis of presidential cycles since 1881 shows starting valuations play a larger role in returns than the party in the White House.

Prepare, Don’t Outguess

Investor Howard Marks famously stated, “You Can’t Predict You Can Prepare.” This advice is particularly relevant in investing, especially during events like elections. Presidential elections bring a set of clearly defined outcomes, but they are intensely scrutinized by market participants, so any news about election odds is typically quickly priced into markets, making it unlikely that investors can profit by guessing the outcome.

Preparation, however, takes on a different meaning. For elections, it involves simulating various outcomes and understanding their potential impact on portfolio positions. As fundamental investors, we focus on how election outcomes might affect an investment’s long-term earnings power. For many assets, elections have a negligible direct impact. However, for a subset of assets, public policy-such as regulation or trade policies-can have significant consequences. Election preparation involves conducting scenario analysis to determine how a political party or individual candidate’s policy agenda may impact an assets price, with the goal being to make sure that these risks are well-balanced.

Can You Profit from an Election?

Markets are forward-looking mechanisms that reflect the most probable set of future outcomes at any given point in time.

The notion that markets reflect public information, making them difficult to beat, was popularized by Eugene Fama in his Efficient Market Hypothesis (EMH) in the 1960s. Early work in this field relied on empirical research known as event studies. These studies analyzed well-defined events, such as earnings announcements, and tracked the asset’s price before and after the news became available. In these controlled settings, markets are highly effective at instantly reflecting new information into prices, making it very challenging to profit from short-term news.

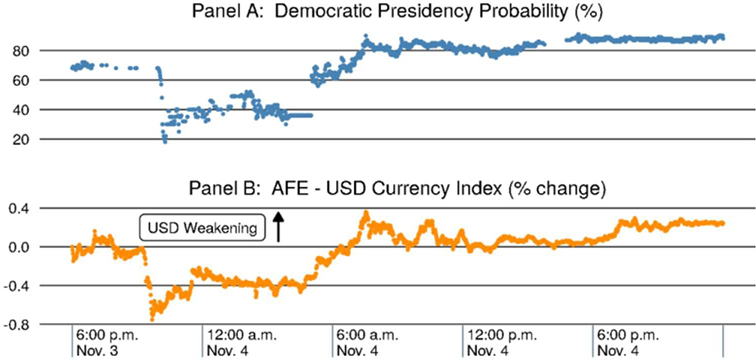

Exhibit 1 illustrates the changing odds of Joe Biden winning the 2020 presidential election according to the betting market Predictlt in Panel A, tracked during the night of the last presidential election. Panel B shows the price of a basket of major currency exchange rates against the dollar, which moved in almost perfect correlation. The odds started around 70%, then dropped to 20% as early results favored Republicans, only to rise back to 90% as more results surfaced.

Prediction markets started pricing in a 90% chance of a Trump victory around 10:30pm Eastern time, well before the outcomes in key swing states were called. Major currency and equity markets also responded instantly to the changes in odds.

Exhibit 1: Instant Pricing of Election Odds

Source: DeHaven et al 12024) “Minute-by-Minute: Financial Markets’ Reaction to the 2020 US Election,” Cornell University.

So, is there any way to benefit from elections? While informational efficiency makes profiting difficult, one of the most common mistakes markets make is overreacting to information. For example, while Chinese stocks were down on news that is expected to Trump win the presidency, we may conclude that the market misjudged the magnitude, providing an opportunity to add to our position.

Elections can, therefore, create opportunities for investors who are prepared to capitalize on market overreactions. Being able to act on these opportunities requires a disciplined process and preparation about an asset’s potential long-term election impact.

Post-Election: Focus on What Matters Most

With the election results pointing to a Republican victory, attention now shifts to the potential impact of the Trump presidency on financial markets. This raises the question: How important is the presidential party in determining return outcomes?

We analyzed data from the past 36 presidential terms, spanning from James A. Garfield’s inauguration in 1881 through Joe Biden’s tenure. Using Robert Shiller’s long-term dataset. we examined US stock market performance incorporating the two months prior to each inauguration to account for the market response to the election outcome.

Exhibit 2 reveals that presidential party affiliation accounts for less than 1% of the variability in returns across presidential terms, indicating a negligible impact. In contrast. starting valuations, as measured by the CAPE Ratio, explain 17.8% of the differences in returns across presidential cycles.

The takeaway? Valuations are a far superior predictor compared to the party occupying the White House.

Exhibit 2: Starting Valuations More Important than Party Affiliation

Source: Robert Shiller data library, Morningstar Wealth analysis.

In the days ahead, predictions will emerge about how a Trump presidency could influence returns. This analysis serves as a reminder that valuations are likely a more reliable predictor than who’s in the White House.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Investment Insight: U.S. Election Market Reaction

The reaction to Donald Trump winning the Presidency and the Republicans reclamation of the Senate has been emphatic. In general, risk assets are rallying aggressively. The S&P 500 Index closed 2.5% higher, while the NASDAQ Composite moved up approximately by 3%, and small-cap Russell 2000 Index closed 5.8% higher. Australian equities also rallied yesterday, though not to the same extent. The wildly positive reaction is being driven by the belief that the Republicans will take actions that are supportive of corporate earnings and stock price appreciation—examples include extending corporate tax cuts that are set to expire, decreased regulations leading to cheaper expansion and elevated merger and acquisition activity, and a general business-friendly mindset.

The U.S. Dollar is gaining value relative to developed country currencies (including the AUD) in conjunction with the move up in yields.

The ASX 200 rose 0.8% on Wednesday, while international equity markets had mixed reactions.

Asia: The Japanese Nikkei Index rallied 2.6% while Hang Seng Index (Hong Kong) fell by 2.2% in conjunction with the Shanghai Composite Index declining slightly by 0.1%. Chinese equities are lagging as Chinese Imports have been the primary target of Trump’s tariff narrative all throughout his campaign.

Europe: The FTSE 100 Index fell by 0.1% with the DAX Index down by 1.1%.

All but three of the U.S. Equity Sectors were positive on the day:

While the majority of U.S. sectors moved higher overnight, they were not all for the same reasons. Some are just participating in the broad-based equity rally, but other like Financials, Energy, and Technology are likely to benefit from Republican control. Financials, specifically Banks, stand to benefit from decreased regulatory restrictions and a steeper yield curve which makes their lending activity more profitable. Energy companies will look forward to less regulation and looser restrictions on drilling and exploration. Highly profitable technology companies will benefit more than others from no increases in corporate tax rates. U.S. small-caps rallied aggressively as they stand to benefit meaningfully from decreased regulation and increased merger and acquisition activity. Small-caps are often acquisition targets of larger companies that are willing to pay a premium for buying their business—this makes up a component of the return small-caps have generated historically. Regulatory hurdles and costs can have an outsized impact on smaller companies as the incremental costs are often harder for them to overcome to compared to larger scale counterparts.

Growth companies across all sizes are benefiting as the business-friendly mindset Trump carries will support their growth initiatives in a variety of ways. Growth companies will also benefit from the lower corporate tax rates Republicans are likely to maintain.

Some takeaways, lessons, and reminders from today’s market reaction:

Even if an investor had high conviction that Trump would defeat Harris and Republicans would take the Senate, the scale of the market moves would likely have still been surprising. To fully benefit an investor would have been required to make large one-way bets. We can never know what would have occurred if Harris had won, but the benefit of making short term one-way bets is almost always not worth the risk as the cost of being wrong is so meaningful. Imagine if an investor believed Harris would triumph and positioned in a way that missed out today’s rally. This further supports our Prepare, Don’t Predict approach driven by fundamental analysis, scenario analysis, and robust portfolio construction.

Most initial reactions align with conventional wisdom and expectations—higher interest rates, Chinese equities lagging the rest of the world, and U.S. small-cap exceptionalism are not surprising.

Reminder that historical analysis of market performance based on election outcomes is imperfect, at best. Today’s massive rally highlights the risk in that as the rally is technically occurring under Biden’s Presidency but is clearly being driven by Trump’s victory. Time will tell how durable today’s moves are. I view them as a resetting of the baseline and in the near future investors will turn back to conventional factors such as earnings, economic data, and interest rate policy to drive their decisions.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Adviser-to-client template: Paragraphs on the US election

For financial advisers to use with clients. This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

You may be wondering how the election of Donald Trump might impact your investment portfolio. Before we dig into last night’s events, I’d like to assure you that it is business-as-usual from our side and for our investment manager, Morningstar Wealth.

Often the biggest risk in situations like this is reacting impulsively to the fears stoked by headlines in the media. But I’d like to remind you that politics and investing are two distinctly different areas, and we will continue to manage your portfolios to ensure they are diversified and robust.

US Election

Donald Trump has won the Presidency and the Senate, which on paper gives him a clear mandate to enact his fiscal and monetary policies. The House of Representatives remains up for grabs which may curb his ability to deliver on all his plans – depending on how the outcome lands.

The market reaction in the immediate aftermath of the election is commensurate with Trump’s key policies of anti-immigration and protectionism. The US dollar has rallied as investors price in the possibility of trade tariffs. US government bond yields have risen (meaning prices have fallen) driven by a higher probability of inflation as the US labour force shrinks.

However, we are mindful that there is huge uncertainty surrounding the actual policies President Trump might get behind and these moves may reverse.

Taking a Long-Term View

We will continue to monitor proceedings and will keep you informed if anything material ensues. Regarding your portfolio, it is for circumstances like this that Morningstar takes a diversified approach when managing money.

Your portfolios hold assets like financial stocks and broad equities that should perform well if inflation rises and growth backdrop consolidates. There are also positions like defensive equities and government bonds that should appreciate if the global economy loses momentum.

At the same time, the portfolios have avoided going “all in” on any potential outcome. Instead, your portfolios are robust and constructed so that they might be expected to perform well over the long run, come what may.

Last, we leave you with two key points.

- In the face of political uncertainty, it is normal to question whether you should sell, hold or buy. To our eye, the answer is simple… manage risks, stay informed and—most importantly—stay the course.

- Any turbulence in markets may create great opportunities to purchase assets that will add meaningfully to returns in the future.

We hope you find this perspective helpful and we’ll keep you updated as events evolve. As it stands, we want you to know we’re carefully monitoring proceedings, and we are here to help with any questions you may have.

Regards,

Adviser

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

The ABC Model: How Advisers Can Help Manage Client Stress

Even if someone is well-off, they are not immune to financial stress.

Investor discomfort in handling financial issues is one of the most common reasons that they hire a financial adviser, according to recent research from our team.

It’s not just about increasing returns. For example, one respondent told us, “The market can be a daunting place and [my adviser] help[s] me navigate based on my needs. I would rather trust someone with expertise than learn on my own.”

This response encapsulates the thought process of many investors who’ve hired a financial adviser. Clients recognise they don’t have the time, knowledge, or resources to make the best decisions for their finances themselves.

There’s good reason to seek out help when facing discomfort with finances. On top of being unpleasant, worrying about finances can also lead to people feeling generalised psychological distress, and people who are stressed by their finances are more likely to exhibit signs of depression.

Unfortunately, having money is not enough to resolve the strain that financial stress can put on someone’s mental well-being. People’s subjective perception of their wealth is not always linked with their monetary reality—which means that even if someone is well-off, they are not immune to the feeling the stress of their finances and the negative downstream effects.

How Do Advisers Help Diminish Stress for Clients?

To answer the question, let’s look to the ABC-X model of stress, which examines how a stressor, A, leads to a stressful (or not stressful) outcome, X. This model can help explain why different clients react differently to the same financial stressors and what advisers can do to alleviate the strain those stressors can cause.

Here’s how this model works:

- A refers to the stressor at hand, which can include anything presenting a challenge that requires a response. An important feature of stressors in this model is that they are inherently neutral. That is, they do not have to lead to bad X(outcomes). Instead, the outcomes depend on factors B and C. For example, receiving an inheritance you didn’t plan for is an A stressor, and so is a pricey medical bill.

- B refers to the resources people have to navigate the challenge. These can be an individual’s internal resources, such as their perseverance. But they can also be external resources, such as an individual’s social support and their broader safety net.

- C refers to the perceptions people have of the stressor—that is, what do they think about it? Is it horrible? Is it just another challenge to conquer? The way that a person perceives a stressor will affect how they respond to it.

In this model, any given stressor can lead to a good outcome if people have the right resources and perception of the stressor.

Financial advisers can help with both of these factors. A financial adviser is another resource that people can draw upon when they are confronted by a stressor. Advisers can help them execute actions, explain important considerations, and more.

But what may be less obvious is that advisers can also help shape investors’ perceptions of the stressor through behavioural coaching. Advisers can help clients see new opportunities in the situation, provide perspective, and help clients identify the strengths they have that can help them cope with the stressor.

Showing Prospects You Can Give Them Peace of Mind

To that end, we recommend that advisers who want to convert prospects into lifelong clients speak to their need for peace of mind from the start. This can involve highlighting how your expertise can reduce decision-making anxiety and provide clarity on different investment options. It may also include emphasizing your commitment to build a financial plan that will help them reach their goals.

But a particularly effective way to help clients see how you will help them achieve peace of mind is through storytelling—that is, providing compelling anecdotes from previous client interactions.

To do so, I recommend using the ABC-X model as a framework for your story. This framework will help you show prospects how you act as a resource and provide perspective to clients when they’re confronted with stressors.

- A: Share an anecdote about a common stressor that clients face (if you’re really advanced, you can create one anecdote for any number of common stressors and share the one most relevant with each client). When talking about the stressor, identify the challenges a previous client faced with it: What did they have to decide? Where were the opportunities available? Where were the pain points? You want to show that you understand how these stressors can make clients feel.

- B: Demonstrate how you served as a resource to clients for handling a stressor. Show them how your expertise was used to help solve the problem. For example, you might talk about how you were able to compile different options for your clients and explain the benefits and drawbacks of each. Here, you have the opportunity to highlight how your clients relied on your expertise so they didn’t have to spend the time and energy figuring it out on their own.

- C: Talk about how you informed your client’s perceptions of the event. For example, you may have reminded your client that a down market gives them the opportunity to see things as a buying opportunity instead of just as a hit to their portfolio. Here you can show clients that there are different ways to view stressors that they may not have considered without your help.

- X: Share your client’s happily ever after. How did your client ultimately handle the stressor? How did they feel? Quotes from your clients may be especially impactful here, as they give prospective clients the opportunity to hear how working with you changed how stressful the outcome was for your clients.

Since its original publication, this piece may have been edited to reflect the regulatory requirements of regions outside of the country it was originally published in. This document is issued by Morningstar Investment Management Australia Limited (ABN 54 071 808 501, AFS Licence No. 228986) (‘Morningstar’). Morningstar is the Responsible Entity and issuer of interests in the Morningstar investment funds referred to in this report. © Copyright of this document is owned by Morningstar and any related bodies corporate that are involved in the document’s creation. As such the document, or any part of it, should not be copied, reproduced, scanned or embodied in any other document or distributed to another party without the prior written consent of Morningstar. The information provided is for general use only. In compiling this document, Morningstar has relied on information and data supplied by third parties including information providers (such as Standard and Poor’s, MSCI, Barclays, FTSE). Whilst all reasonable care has been taken to ensure the accuracy of information provided, neither Morningstar nor its third parties accept responsibility for any inaccuracy or for investment decisions or any other actions taken by any person on the basis or context of the information included. Past performance is not a reliable indicator of future performance. Morningstar does not guarantee the performance of any investment or the return of capital. Morningstar warns that (a) Morningstar has not considered any individual person’s objectives, financial situation or particular needs, and (b) individuals should seek advice and consider whether the advice is appropriate in light of their goals, objectives and current situation. Refer to our Financial Services Guide (FSG) for more information at morningstarinvestments.com.au/fsg. Before making any decision about whether to invest in a financial product, individuals should obtain and consider the disclosure document. For a copy of the relevant disclosure document, please contact our Adviser Solutions Team on 02 9276 4550.

Remote Work: A Curse or a Blessing for Advisers?

Establishing clear guidelines is key to building a successful work model for employees.

The traditional office environment is undergoing a dramatic transformation. Fueled by the covid crisis, technology, and a desire by workers for flexibility, remote work has become front and center in most industries, including advisory businesses. Like any significant change, it presents unique advantages and disadvantages for both employers and employees.

Advantages of Remote Work

Employees tend to prefer remote work because it offers highly sought-after flexibility that can significantly improve their work-life balance. By avoiding a commute, employees can have more time for family, hobbies, or simply more sleep! This can lead to increased satisfaction and possibly even higher productivity. Additionally, a home office could offer a quieter and more distraction-free environment, boosting focus and productivity. Finally, remote work can be beneficial for those managing personal commitments alongside careers or those who thrive in more solitary environments.

Employers can save money from implementing a remote workforce. Cost savings can include lower rents on office space, as well as decreased spending on utilities and office supplies. Perhaps the biggest benefit is that companies can hire top talent from anywhere, not just those geographically close to their offices. This can lead to a higher-quality, more diverse workforce.

Disadvantages of Remote Work

Even though many employees prefer it, the flexibility of remote work can be a double-edged sword. Blurred lines between work and personal life can lead to longer hours and potential burnout—or home distractions could result in substandard performance. Also, the camaraderie, opportunities for on-the-job learning, and sense of belonging that come from working with colleagues can be difficult to replicate virtually.

For employers, communication, the lifeblood of a cohesive employee team, can become more difficult in a virtual setting. Without on-site operations, opportunities for spontaneous brainstorming sessions and quick hallway discussions will be lost. Remote work models make fostering a strong company culture and team building more difficult. Finally, for companies where client interaction is crucial, remote work can be a challenge. While video conferencing helps, some clients may still value in-person meetings.

A Hybrid Approach

Many companies are finding that a hybrid work model can achieve the best of both worlds. A blend of remote and in-office work can fulfill the needs of employees, employers, and clients. To ensure communication and workplace cohesiveness while providing for clients’ preferences, it is best to have a combination of full-staff and half-staff office days rotating with remote days. An example of this would be full staff days in the office on Tuesdays and Thursdays, half staff days in the office on Mondays and Wednesdays, and full remote on Fridays.

Guidelines for Building a Successful Remote or Hybrid Work Model

Regardless of the chosen model (fully remote or hybrid), a well-planned approach is essential. Here are some detailed recommendations:

Clear Expectations

Document your expectations in a handbook that fully outlines your firm’s remote work policy. This handbook should clearly define work hours, communication protocols, and guidelines for equipment use and data security:

- Work Hours: Specify daily working hours when employees are expected to be available and responsive. This helps maintain clear boundaries while offering flexibility. Consider offering some level of employee choice in determining their split between remote and in-office workdays. Note that certain roles might require more in-person collaboration, necessitating a more structured approach.

- Communication Protocols: Outline preferred communication platforms (email, instant messaging, Microsoft Teams, video conferencing), and establish response time expectations to ensure efficient information flow.

- Performance Metrics: Define clear performance metrics used to evaluate employee success in a remote or hybrid environment. This could include project deliverables (financial plans, investment reviews, and so on), number of clients served and client meetings/phone calls, and client satisfaction ratings.

- Security Measures: Outline data security measures to protect sensitive company information. This includes data encryption policies, strong password requirements, and guidelines for handling confidential information remotely. It is also best practices to provide company hardware (computers, tablets, headsets) managed by company internal or external IT specialists.

- Acceptable Use Policy: Clearly define acceptable use of company equipment and software to ensure responsible use of company resources. Employees should not be allowed to use company tools for personal purposes.

Technology

The success or failure of full or hybrid remote work depends heavily on technology. Reliable videoconferencing tools, cloud-based collaboration platforms (like Google Docs), scheduling tools, and project management software are crucial for seamless communication and information sharing between remote and in-office employees. Be sure to invest in high-quality hardware and software. Supporting a remote team requires tools that are robust and reliable.

Empowering Your Workforce

Managing a fully or partially remote workforce necessitates careful and thoughtful handling of employees. This includes training and support, fostering a culture of trust and accountability, and building teamwork.

- Training and Support: Training is imperative in the areas of communication, cybersecurity, and work-life balance techniques. Communication training should include etiquette for video conferencing, best practices for online collaboration tools, and clear writing skills for emails and instant messaging. Employees should be educated about cybersecurity best practices to protect themselves and company data from online threats, including training on phishing email identification, strong password hygiene, and secure data handling practices. Beyond “technical” areas, employees should be offered training and resources to help maintain a healthy work-life balance while working remotely.

- Fostering a Culture of Trust and Accountability: When employees are not on-site, it can be more difficult to supervise and manage them. Management should shift from monitoring activity to measuring results. Be sure to set clear performance expectations and provide regular feedback to ensure employees are on track. To do this, open communication and transparency must be encouraged between managers and employees. This will foster trust and allow for early identification and resolution of any issues. Finally, recognise and reward employees for their achievements; this motivates employees and reinforces positive behaviors.

- Building Teamwork: Remote workers require more opportunities for building rapport with their co-workers, including formal and informal options. Formal options can include regular virtual team meetings (weekly or biweekly) to discuss projects, share updates, and promote informal interaction as well as organised virtual social events, like online games, trivia nights, or online book clubs. Informally, you can encourage remote workers to schedule periodic virtual or in-person lunches and also establish an online forum or chat platform for casual communication and knowledge sharing. This allows for peer-to-peer collaboration and fosters a sense of community.

Dealing With Clients

While employees might be thrilled with the opportunity to work fully or partially remotely, clients might not mirror that enthusiasm. Beyond maintaining your client service and quality at high standards, you must work to ensure a positive client experience at all levels.

While video meetings have become commonplace, when it comes to clients, it’s important to go beyond a one-size-fits-all approach. Communication is key here. Be sure to clearly communicate the flexible meeting options you offer. During initial client contacts, determine their preferred meeting format and honour their preferences. For long-term clients, realise that the shift to full or partial remote work will be new—and possibly scary—to them. Conduct a survey to get an idea of your client base’s preferences. Ask if they prefer in-person meetings, video conferencing, or a combination of both. Gauge their comfort level with different technologies and inquire about any accessibility needs. Consider categorising clients based on meeting preferences.

Finally, be prepared to answer client questions and address any concerns they may have regarding remote interaction. In the end, it is your responsiveness and service level that will make all the difference.

Be flexible in your meeting options, including in-person, video conferences, and hybrid meetings:

- In-Person Meetings: Even if you have a fully remote workforce, you should maintain a limited office space (strategically located for client convenience) to host in-person meetings. Consider offering travel assistance (like Uber or Lyft) for key client meetings and initial consultations.

- Video Conferencing: There’s nothing worse than fuzzy or garbled video conferencing. Be sure to invest in high-quality video conferencing hardware and software with clear audio and high-definition video. Train employees on proper camera positioning, lighting setup, and professional etiquette for video conferencing. Be flexible by offering clients to choose their preferred video conferencing platform (for example, Zoom, Teams, Google Meet). Finally, provide clients with clear instructions and technical support for joining video conferences.

- Hybrid Meetings: To accommodate clients who want to participate remotely while others attend in person, you need to offer hybrid meetings. Again, be sure to use high-quality audio and video equipment to ensure clear communication for both remote and in-person participants.

Today’s employees no longer want to work in an office five days a week. To remain competitive and to attract and retain top talent, employers must be willing to adopt at least a hybrid remote work model. The success of this model depends on clear communication, flexibility, and a commitment to creating a positive work environment for both remote and in-office employees. To ensure the arrangement meets the evolving needs of your business, employees, and clients, be sure to regularly evaluate and refine your hybrid work policy.

*Sheryl Rowling, CPA, is a columnist for Morningstar. Morningstar acquired her Total Rebalance Expert software platform in 2015. The opinions expressed in her work are her own and do not necessarily reflect the views of Morningstar.