Adviser-to-client template: A sell-off, a rebound, and investing through all conditions

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

After a challenging March, markets have rebounded strongly through April, with some major share market indices even testing new all‑time highs. It’s short and sharp market movements like we’ve just witnessed which provide a timely reminder that investing is a long-term game.

It’s also worth remembering that investing can feel counter‑intuitive. As humans, our brains are naturally wired for short‑term rewards and quick feedback, which is why market moves can trigger an emotional response. Investing, however, requires delaying that instant gratification in pursuit of long‑term outcomes that are inherently uncertain. Recognising this challenge is important, as it reinforces why discipline, patience and a structured investment process are so critical to long‑term success.

It’s understandable that short‑term market moves can be unsettling, however, reacting to volatility often does more harm than good for long‑term investors. Staying focused on long‑term goals, rather than day‑to‑day market noise, remains critical to achieving better outcomes over time.

So, how can we avoid overreacting to short-term noise but potentially take advantage of opportunities that present themselves when there has been a market overreaction? Morningstar apply this discipline through a valuation‑driven asset allocation approach. In simple terms, they seek to take advantage of dislocations in asset prices during periods of market volatility. Through March, markets generally fell in unison, meaning few assets became meaningfully cheaper relative to their fair value and limited opportunities emerged.

With geopolitical uncertainty still present, periods of market volatility are likely to reappear at some stage. When they do, Morningstar will be looking for signs of overreaction, where asset prices move away from fair value and become more attractively priced. That will be their signal to react.

This approach also reinforces the importance of diversification across asset classes, countries, sectors and sources of return, helping portfolios remain resilient through different market environments while staying aligned with long‑term objectives and helping to smooth out the bumps in the road somewhat.

Importantly, investors do not need to take any action during these periods. Morningstar continues to actively manage portfolios on their behalf, applying a disciplined, valuation‑aware process through both calm and volatile markets. Having that peace of mind can be especially important during times of uncertainty, as making emotional decisions in response to short‑term market moves can be one of the most damaging things an investor can do to their long‑term outcomes.

How to discuss portfolio diversification with different types of clients

By Samantha Lamas, Senior Behavioural Researcher

For financial professionals and advisors, understanding the value of portfolio diversification is taken as a given. We know a well-diversified portfolio comprising assets with different performance characteristics can lead to better risk-adjusted returns instead of relying on a single asset class.

However, when presenting a financial plan to a new client, the advisor may say something like: “We created this diversified portfolio that puts you on track to meet your goals…” and then go on to discuss another aspect of the client’s holistic plan—completely skipping over the client’s understanding of diversification in portfolio building.

For everyday investors, portfolio diversification may seem counterintuitive because it often requires adding assets that look “bad” in the short term, with benefits that only materialize over years. Others assume the concept is simple (“don’t put your eggs in one basket”) and underestimate the complexity behind selecting uncorrelated assets. Thus, an advisor speeding past a phrase like “diversified portfolio” may be committing one of the seven advisor faux pas we identified as hurting the advisor-client relationship: using financial jargon.

Moreover, spending just a little more time on concepts like portfolio diversification can help showcase your value to clients. Our research finds that investors want more than just portfolio advice: They want a coach, teacher, and a sounding board. Advisors are uniquely positioned to play these roles for investors, and that can start by tackling concepts like portfolio diversification when needed.

Now, the question is, how?

Emphasize What Portfolio Diversification Isn’t

One of the difficulties in understanding portfolio diversification is that it sounds like a familiar concept. Everyone knows the saying, “Don’t put all your eggs in one basket.” Unfortunately, this phrase cannot be applied to every situation and, when it is, it can lead to disastrous mistakes.

In our own research, we found that when presented with three exchange-traded fund options that track the S&P 500 but have different fees, many investors choose to put some assets into each option, even the most expensive option. In the real world, a decision like this could result in a portfolio with significantly higher fees and overlapping securities since each fund followed the same index.

When discussing portfolio diversification with clients, it may be worthwhile to emphasize that this diversification is not as simple as just varying your holdings. Instead, it’s about combining assets in a portfolio that tend to behave differently, in a way that still aligns with the investor’s goals and risk profile.

Reframe Talking Points to Address Client Needs

While clarity is good, it can be easy to fall into the trap of overexplaining diversification to an investor and overwhelming them with numbers and graphs. Not only is this unnecessary and probably inefficient, but it can be harmful to the advisor-client relationship—no investor wants to leave their advisor’s office feeling confused.

Instead of throwing mountains of research at a client, advisors should customize their messaging based on their understanding of the client’s values, goals, and preferences.

A simple framework that advisors can use may look like this:

1. Give a Brief Description of Portfolio Diversification

This can be a standardized section in all your conversations and should be true to how you think about this concept. As an example, this can sound like Dan Lefkovitz’s description:Diversification means the investments in your portfolio behave differently. When one asset zigs, the others zag. When developing a diversified portfolio for you, I also take into consideration your goals, time horizon, and risk preferences.

2. Explain Why It Matters to the Client

This section should be personalized to the client. Here’s where you can emphasize specific elements of portfolio diversification that can better resonate with clients based on their personal characteristics and tendencies.

To add some color to this framework and help advisors use it in practice, below are a few examples of how to reframe a portfolio diversification discussion based on common investor personas.

To the Client Who Is a Constant Worrier

Every advisor has at least one client who is in a perpetual state of worry. These clients frequently ask questions like, “How will AI impact the tech sector and my portfolio?” “Will stricter tariffs continue, and how does that impact my plan?” “Will the US dollar continue to decline, and what does that mean for me?”

These are all important questions, but they are all almost impossible to answer definitively. Instead, advisors can refer back to the powers of portfolio diversification with a focus on its ability to reduce the impact of uncertainty. When talking to these clients, advisors can emphasize that portfolio diversification is a hedge against the unknown. It is impossible to know with certainty which area of the market will suffer in the future; thus, a properly diversified portfolio guards against being overly exposed to any one area that falls out of favor, whatever that area may be.

To the Client Who Is Counting Down the Days to Retirement

Other clients may not be so worried about the day-to-day, but they may be minutely focused on their goal of retirement. For these clients, explaining portfolio diversification can be a way to increase their confidence in reaching that goal. Our research indicates that what investors value most in an advice relationship is the advisor’s ability to provide peace of mind that they are on track to reach their financial goals. In this instance, discussing portfolio diversification can be seen as an opportunity to provide that reassurance and, accordingly, emphasize your ability to provide this value.

When discussing portfolio diversification with these clients, advisors can explain how portfolio diversification allows the client to have a smoother ride as they tackle their ultimate goal. Reducing exposure to any one risk smooths out the volatility the portfolio will face while still staying on track to reach the retirement goal. That means fewer dramatic portfolio swings and fewer sleepless nights.

To the Client Who Wants to Maximize Returns

Other clients may ask why you aren’t being more aggressive in your investment picks. These are investors who are more comfortable with risk and may not see the point of prioritizing risk-adjusted returns versus just plain-old returns.

Portfolio diversification discussions can be reframed in a way that addresses their desire to pursue high-return opportunities without taking on excess risk. As Morningstar researchers put it, “Holding a diversified portfolio helps investors expand the opportunity set and ensure they do not miss out on areas that can enhance long-term returns.” While diversification isn’t designed to maximize returns, it increases the chances of capturing whatever part of the market is doing well, while limiting damage from what isn’t.

Diversification Discussions Benefit Both Sides

Diversification can be abstract, but the conversation doesn’t have to be. By avoiding jargon, correcting common misconceptions, and tailoring explanations to client motivations, advisors can make diversification intuitive and meaningful while building a stronger relationship with their client.

From the desk of the CIO: Are we seeing market recovery?

By Bryce Anderson, Senior Portfolio Manager

We’ve seen a market rebound after March sell-off

These events are not a repeat of 2022 or 1970s high inflation.

Markets have staged a rebound after the March sell-off, rewarding investors that stayed invested or topped up portfolios. The sell-off was not large enough to unearth many bargains but it did reduce speculation and injected better value as investors became more cautious. We selectively added exposure in the sell off. Morningstar portfolios continue to blend broad diversification, specific investments to mitigate more extreme scenarios and attractively priced granular opportunities like Healthcare, Consumer defensive and regions like Brazilian equities.

The big question now is whether the stand-off between the US, Israel and Iran will create a lasting and large rise in inflation and trigger economic slowdown.

In the short term, expect higher inflation. Higher oil and gas prices are clearly flowing through to higher goods prices. The longer the hit to Middle East energy production and export, the bigger the inflation impact. Governments are already stepping in to support consumers with subsidies but not to the extent seen back in 2022.

This is not a replay of the 2022 embargo on Russian exports or the start of a 1970s style stagflation. The energy supply shock from the Middle East this time is far less impactful. That’s because the world’s energy supply is way more diverse than before and rapidly increasing. The old saying that “the cure for high oil prices is high oil prices” is borne out by the hunt for alternatives that have lessened oil and gas demand and put downward pressure on prices.

The first is more efficient use of energy across economies, that started back in the 1970s and 1980s. That was followed by the search for newer oil and gas supplies culminating in shale oil, oil sands, and deep sea oil fields including those here in Australia. Our colleagues at Morningstar Equity Research and Morningstar Multi Asset Research point out that gas supplies are surging, much of it from Canada and the US. By end 2027, new natural gas supply is expected to be twice the 2024 gas output from Qatar.

Equally important is the development of solar and wind power generation and electric transport. These strategic alternatives to oil and gas can be scaled much more quickly and cheaply, so at the margin they too are sapping demand for oil and gas.

All these factors mean the probability is low of a large, sustained rise in energy costs from current levels. On top of that, the pass through of higher energy costs to prices of goods and services is muted, by rising unemployment and the impact of AI. Labour markets have far more slack in them now than back in 2022 and the Union dominated wage setting of the 1970s. So, we do not see lasting large economic slowdown or increases in interest rates as likely, especially with interest rates above inflation rates, unlike 2022 and the 1970s.

The big takeaway is that staying invested and remaining well diversified is the most reliable way to manage risk, profit from uncertainty and help investors reach their goals.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

Geopolitical tensions are continuing to dominate headlines, and the impacts are being felt here in Australia. With the numbers at the bowser climbing, we know you may be concerned about the ongoing impact of the conflict both on your investments and in a broader context. Though recent news of a ceasefire between the US, Israel, and Iran has headlines buzzing, the details can be overwhelming. But, despite the noise, we and our investment manager, Morningstar, are concentrating on the things we can control and taking a long-term approach that’s been designed to withstand volatility.

What we know so far

It’s a fast-moving situation, so let’s stick to the essentials. The US, Israel, and Iran have agreed to a preliminary 14-day pause in hostile actions to allow for broader peace talks. This includes reopening the Strait of Hormuz, a significant shipping channel, though not without conditions. While progress has been made, multiple strikes were still reported across the Gulf after the agreement was meant to take effect.

What this means for portfolios

Morningstar’s long-term investment approach has been tried-and-tested through all types of volatility, including the COVID-19 pandemic, ‘Tariff Day’ turbulence, and even the Global Financial Crisis. By choosing a well-diversified group of assets, rigorously evaluating risk, and paying close attention to the price paid for investments, the Morningstar investment team focus on building robust portfolios that are positioned to weather rapidly changing conditions.

What you should do

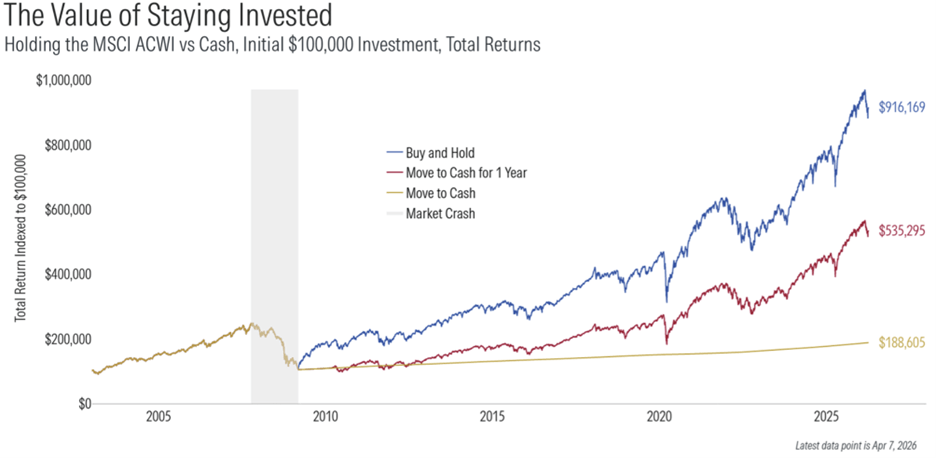

As ever, a core principle of successful investing is to stay invested. The below chart, where the grey column highlights the GFC years, shows the difference between moving to cash, moving to cash for one year, and simply holding and staying invested. The blue line – staying invested – is the clear leader.

Source: Clearnomics, MSCI, Federal Reserve. Past performance is no guarantee of future results. This is for illustrative purposes only and not indicative of any investment.

As you can see, investors who stayed invested not only endured the volatility, but continued to experience an upward trend of returns, even considering additional periods of market drops.

We’re always available to talk

Of course, it can be tricky to withstand this in the moment, so please feel free to reach out for a conversation at any time. If you have questions about your portfolio or your financial plan, I’m happy to help.

From the desk of the CIO: What we know about the oil shock

By Bryce Anderson, Senior Portfolio Manager

Key points

There has been a spike in oil and gas prices

However, the world is less driven by energy prices than in the past

We maintain a focus on risk management.

The outbreak of a wider war in the Middle East has reawakened fears of inflation as energy prices rocketed. This is a classic example of unpredictable and impactful events that continue to occur. In the short time since the start of the Iran war, equity and bonds have sold off while the US dollar and share prices rose for oil and gas companies. The market moves have not been large (at the time of writing) and have not reversed the gains chalked up in the first two months of the year.

What happens next is not knowable. There are many feasible scenarios, each with quite different economic and market impacts. These range from an imminent ceasefire that leaves the existing Iran regime intact to a “perma-crisis” of prolonged conflict that transforms economies.

Investors now face the question of how to respond. Our approach is to review the readiness of our portfolios for what may come, knowing that there is huge uncertainty. As we do this, we are looking at what markets have already priced in and the likelihood of extreme scenarios.

In a nutshell, energy prices, inflation expectations and bond prices now reflect ongoing higher oil and gas prices and no further cut in interest rates from the Bank of England. So far energy prices have risen substantially (approx. 60% and 180% for oil and European gas), but are still considerably lower than in 2022 when European gas prices peaked at over 6 times current levels and oil prices traded above $100 for about 6 months. It’s a far cry from the horror scenario of the 300%+ spike in oil prices in 1973/74 that pushed up UK inflation rates by 9%.

Thankfully, historic energy crises are not a reliable guide to the more probable future scenarios.

Firstly, the world is a lot less sensitive to moves in oil and gas prices. The Shale revolution has transformed the world’s largest economy, the United States, from an energy importer to an exporter. Plus, renewable energy meets far more of our energy needs, in terms of electricity generation and transport. It’s especially important for China, the world’s second biggest economy. Technological advances mean economies are more energy efficient, with the notable exception of power-hungry Artificial Intelligence.

Secondly, inflation is much better anchored. Global prices are being kept in check by overproduction and exports by China, the disinflationary impact of AI, reduced power of unions globally and renewed vigilance by central banks.

Thirdly, interest rates are at more sustainable levels than prior energy shocks, limiting the need for large rate rises to quash inflationary pressures. UK and US Interest rates are already higher than inflation rates and much higher than 2021 and 1972, in inflation adjusted terms.

So, we do not see a return to 1970s stagflation. There is potential for this crisis to create shocks that are more inflationary than deflationary. For this we hold a range of diversifiers such as defensive industries less impacted by business cycles, inflation-linked bonds and liquid alternative investment strategies.

The crisis, like all prior ones, will also create new opportunities. We are closely tracking how events are impacting businesses and asset prices to identify risks and spot opportunities, working closely with Morningstar’s 400-strong research team.

Should your client’s financial knowledge and experience drive risk strategy?

How financial advisers can leverage a client’s sophistication to enhance engagement.

By Nicki Potts, Director of Financial Profiling, and Ryan O. Murphy, Global Head of Behavioural Insights

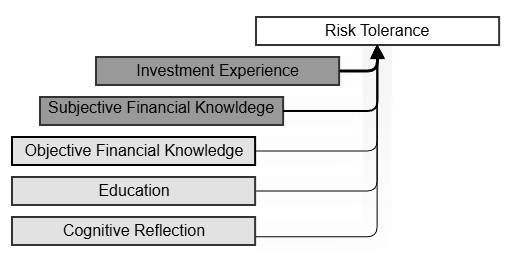

Global regulatory frameworks stress the importance of incorporating clients’ financial knowledge and investing experience into the advice process, yet research exploring the complex interplay between these constructs, risk tolerance, and risk-taking behavior is limited. Our latest research examines the influence of the factors associated with financial risk tolerance on the portfolio allocation decisions of a globally diverse sample of 1,334 investors. Participants were asked about their financial risk tolerance, experience, knowledge, and cognitive reflection. Portfolio allocation data were also collected at the time of survey completion between February and May 2023 to determine the actual investment risk level of participant portfolios.

We found that the specificity of knowledge and experience matters in risk preferences, and that using a robust risk tolerance measure alone can adequately capture the effect of knowledge and experience in financial decision-making. Does this suggest that knowledge and experience are merely redundant in the risk profiling and advice process?

Experience and Confidence Are Key Drivers of Risk Tolerance

Investing experience and financial knowledge are generally linked to positive financial behaviors, such as higher saving rates, market participation, and better debt management, leading to more informed investment decisions. Individuals with more experience and knowledge are also more likely to have higher risk tolerance and hold more risky assets. However, the domain of knowledge and experience matters. We found that broad factual knowledge alone, such as traditional education, general cognitive ability, and, to a lesser extent, general financial literacy, while useful in helping individuals conceptualize financial decisions, is less effective in helping them engage with the specific demands of financial decisions despite their analytical skills.

On the other hand, direct stock and mutual fund experience and subjective financial knowledge (self-evaluations), which are closely associated with perceived financial decision-making confidence, are shown to have the greatest influence on risk tolerance. These factors are directly related to the cognitive and emotional aspects of financial decision-making. It turns out these factors are more related than general traits such as cognitive ability or education, thus making them better predictors of financial risk tolerance. The emerging research on the importance of subjective financial knowledge, and its mediating relationship with investing experience, suggests that confidence can assist individuals in navigating complex financial situations, even when their objective knowledge is lacking, and that enhancing investing experience can further support the effect of confidence on risk tolerance.’

Practically, this means that interventions aiming to enhance risk-taking behavior may be more effective by combining opportunities for experiential learning with traditional structured learnings. For example, the use of gamified virtual portfolios to stimulate market movements might allow investors to develop a better understanding of risk and composure, increase their familiarization with the stock market, and boost their confidence. Similarly, starting new investors with a small “learning portfolio” allows them to consolidate passive learnings with firsthand experience and develop the emotional discipline that is required when real money is at stake.

Integrating Robust Risk Measures With Personalized, Context-Sensitive Advising Strategies

In our analysis, risk tolerance, when measured using a robust tool, emerged as the primary predictor of study participants’ actual allocation to risky assets, further highlighting the predictive effectiveness of closely aligned factors. That said, while the impact of knowledge and experience on risky asset preference appears to be limited once risk tolerance is accounted for, it would be imprudent for advisers to overlook the role of knowledge and experience in personalizing client engagement and advice strategy.

Advisers who adapt communication style, product offerings, and guidance strategies to the client’s level of knowledge and experience can foster greater understanding and trust in the adviser-client relationship, enhancing confidence in the advice process and investment journey. Simple changes like using more qualitative and affective framing (descriptive and context-based narratives rather than precise statistics and probabilities) and focusing on investing principles rather than products may better serve those just starting on their investing journey to better evaluate risk and rewards.

Further, clients with limited knowledge or experience may benefit from starting discussions and their investment journey with less complex financial products that better align with their knowledge and experience without necessarily altering their investment risk strategies. A suitable plan that aligns with the client’s risk tolerance and capacity, and financial goals, comes first in the investment guidance process. Then, the composition of the investments selected for implementation can be fine-tuned to the client’s level of experience and knowledge. This hierarchical approach is sensible and consistent with existing know-your-client and suitability obligations.

As financial decision-making grows more complex, the future of effective advice lies in distinguishing between what determines risk preferences and what enables clients to live with market volatility. Risk tolerance remains the most reliable predictor of risky asset ownership, but experience and confidence shape how clients perceive and interpret volatility, uncertainty, and advice itself. By prioritizing rigorous risk profiling while deliberately cultivating experience and confidence through personalized engagement, advisers can bridge the gap between optimal portfolio design and sustainable investor behavior. In doing so, they move beyond compliance-driven profiling toward advice that is both empirically grounded and retains the human touch.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

What a month it’s been. Between persistent, ‘sticky’ inflation here in Australia, a second successive interest rate rise by the RBA, and escalating geopolitical tensions in Iran and the Middle East tipped to push to $3 a litre, the macroeconomic environment is proving unpredictable, to say the least. The headline news feels relentless, and it’s understandable that you may have some questions about your investments.

First, please rest assured that your portfolios are in good hands. Our investment manager, Morningstar, have decades of experience and have weathered the gamut of precedented and unprecedented conditions with their investment principles and process to guide them. By prioritising diversification, taking a long-term view, and ensuring they’re rewarded for any necessary risk they take, they’re able to build robust portfolios designed to withstand volatility. As we often say, volatility is a feature, not a bug, of investing.

Regarding oil prices, though they’ve seen a big jump, they’re still considerably lower than in 2022 when European gas prices peaked at over 6 times the current levels. It’s also a far cry from the 300%+ spike in oil prices in 1973-74 that pushed UK inflation rates up by 9%.

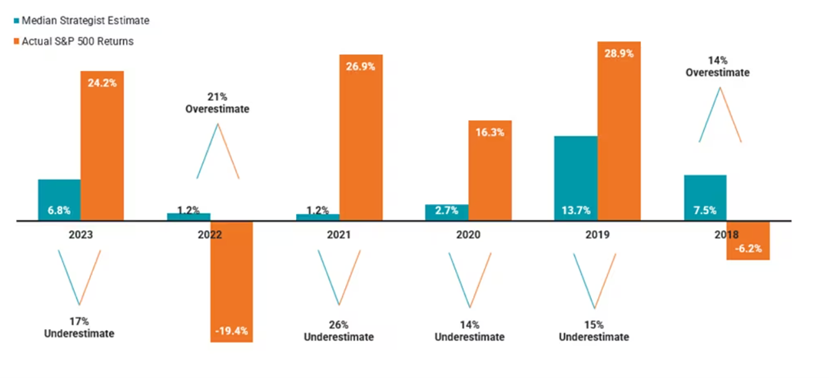

When it comes to forecasting, or attempting to make predictions about what will happen next, we often seen market strategists underestimating or overestimating where markets will finish 12 months on, even with the turmoil of events like war. In the chart below, you’ll see how these under and overestimates in markets are common. That’s why we urge investors to stay invested, trust the process, and stick to their financial plans.

Consensus S&P 500 Index estimates vs. actual returns: 2018 – 2023. Underestimates and overestimates are common. In some years—2022 and 2018—analysts even get the direction wrong.

Source: Morningstar, Inc. “12 Lessons the Market Taught Investors in 2023.” Published January 9, 2024. Indexes shown are unmanaged and not available for direct investment.

Similarly, you may be hearing some chatter around possible recession should the conflict in the Middle East become a long, protracted war. It’s worth noting that recessions are difficult to predict ahead of time, and again, speculation doesn’t necessarily mean a recession is imminent. Consulting firm Fathom Consulting found that of the 469 recessions in 194 countries between 1988 and 2019, the International Monetary Fund had predicted only four by the spring of the preceding year.

Source: Bloomberg, Fathom Consulting, and IMF. Data as of February 23, 2024. “Recession” defined as an annual contraction in real GDP. IMF Working Paper, “How Well Do Economists Predict Recessions?,” Bloomberg, “Economists Lower Recession Forecasts to 40% on US Job Growth Expectations.”

With that in mind, it’s important to remember the fundamentals of successful investing, which is to understand the difference between price and value, and to look to buy quality assets that are worth more than their price at the time of buying. This is what Morningstar are doing across multiple asset classes and markets, looking for opportunities and potential risks. And it’s not just set and forget, as they reassess these decisions every month.

With a well-diversified portfolio of assets that have been purchased at the ‘right’ price with a long-term view, we believe your investments are well positioned to withstand turbulence. Of course, if you have any questions at all, please do reach out to set up a chat.

To use this template, simply copy and paste the below text.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

Over the weekend, you’ve likely heard of the missile strikes that took place in and around Iran. As a result, we’ve witnessed tragic loss of life and an uncertain geopolitical environment, which we expect will contribute to further market volatility.

I want to take a moment to assure you that your portfolio is in safe hands, with our investment manager, Morningstar, monitoring market developments closely. The Morningstar team is guided by a set of proven investment principles and taking a long-term view while keeping a cool head in periods of turbulence is central to how they invest.

Here are some key things to know during this time:

The US has launched missile attacks across Iran in conjunction with Israel, resulting in the head of the Islamic Republic being killed

Iran has retaliated with missile attacks on neighbouring countries and Israel

The stated intention of the US is to remove Iran’s capacity to have nuclear weapons, eradicate its armed forces and remove the existing leadership

US actions occurred without Congress approval or engagement with the United Nations

What does this mean for your portfolio?

There may be some heightened volatility in markets in the near term. Given the fluid nature of the situation, markets are likely to respond to this uncertainty. In this environment, it is important for investors to maintain a long-term perspective.

What is Morningstar doing?

Morningstar’s portfolios remain diversified across different asset classes, geographical regions, and investment strategies. This, as well as a preference for flexibility in portfolios, allows them to move where the best opportunities present themselves.

Morningstar’s investment process has been tried and tested over several years and throughout a range of challenging market conditions, including COVID in 2020, the 2022 market sell-off, and last year’s ‘Liberation Day’ downturn. Through all of these, they’ve maintained a patient and measured approach, and are well-prepared to weather uncertainty.

Of course, if you have any concerns at all, please do reach out. I’m happy to answer any questions you may have about this event or your portfolio in general.

From the desk of the CIO: Keeping a cool head during geopolitical turbulence

By Matt Wacher, Chief Investment Officer, APAC

The escalation of conflict in the Middle East has unsettled markets as investors reassess the implications. Geopolitics has reemerged as a meaningful driver of returns this year, most visibly through a rotation toward cyclical and commodity-exposed assets. What initially began with US intervention in Venezuela has since broadened into a more complex and interconnected set of geopolitical risks centered on the Middle East.

As always, our focus remains on separating signal from noise and interpreting events through the lens of long-term, valuation-driven investing. Importantly, the recent selloff does not exhibit the hallmarks of a traditional growth shock. Instead, it’s better understood as a supply-side shock centered on the energy complex, with transmission to broader capital markets occurring primarily through the inflation channel.

Before examining the market reaction further, it’s worth reiterating the principles that guide our investment team during periods of heightened uncertainty—principles we most recently highlighted in our 2026 Market Outlook.

First, we avoid overreacting to headlines. Periods of market stress are often accompanied by sharp sentiment-driven selloffs, followed by equally sharp recovery rallies. History is clear: missing a small number of the market’s best days materially impairs long-term outcomes. Over the past 25 years, for example, missing just the ten best market days would have reduced cumulative returns by more than half.

Second, we rebalance portfolios and remain disciplined in our strategic allocations. Headline-driven volatility creates opportunities to rebalance by systematically trimming assets that have outperformed and adding to those that have lagged. This countercyclical process has historically added value during volatile environments.

Finally, we actively seek opportunities where market prices have moved materially ahead of changes in underlying fundamentals. Elevated uncertainty can cause investors to indiscriminately discount certain assets. Our teams take the time to rigorously assess the true impact on corporate earnings and economic fundamentals, building conviction before acting. The tariff-related volatility last April serves as a recent example that created attractive long-term opportunities.

How and why is conflict spilling into markets?

While Iran and the broader Gulf region represent a small share of global economic output and capital markets, their primary connection runs through the energy complex. Several key dynamics are relevant.

Iranian oil exports account for less than 2% of global oil production and, in isolation, are manageable. The more significant risk stems from potential disruptions to energy shipping through the Strait of Hormuz. Approximately 20% of the world’s oil consumption — over 20 million barrels per day — passes through the strait, along with roughly 20% of global-liquefied natural gas. These flows have limited alternative routes, making Europe and Asia particularly exposed. Unsurprisingly, this is where market stress has been most acute.

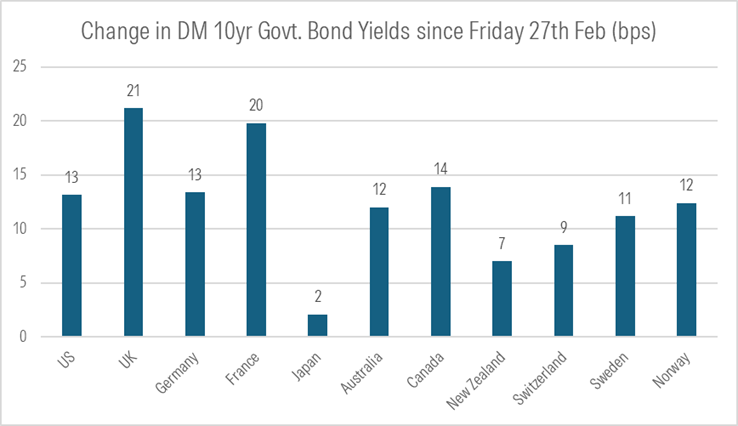

Rising energy prices have had immediate spillover effects on inflation expectations and, by extension, central bank policy. Brent crude prices moving above $80 per barrel have pushed yields higher across major government bond markets, with European yields experiencing the greatest upward pressure given the region’s heavier reliance on Middle Eastern energy supplies. Precious metals such as gold and silver have sold off as higher real yields increase the opportunity cost of holding nonyielding assets, compounded by technical pressures following strong prior performance. The US dollar has been the primary beneficiary among traditional safe-haven assets, supported by a reassessment of the timing and pace of future rate cuts.

Equity market outcomes have diverged across regions and sectors. Energy stocks have benefited, while non-US equities — particularly when currency effects are accounted for — have faced headwinds. Emerging markets have been among the most impacted, reflecting their higher beta characteristics and strong recent performance. Within US equities, technology and financials have held up better, supported by the currently isolated impact of the conflict. Similarly, credit market impacts have been resilient.

If government bonds were acting as a classic risk hedge, we would expect yields to fall. Instead, yields across most developed markets have risen since late February.

Government bonds have not provided a traditional risk hedge

Source: Bloomberg

What are we watching from here?

The situation is fluid and difficult to predict. Our investment team continues to monitor developments, ensuring portfolios remain well positioned to navigate ongoing volatility while staying anchored to our long-term investment strategy.

Several developments warrant close attention.

First, markets are sensitive to the risk that the conflict broadens into a more sustained regional confrontation. Such an outcome would carry more implications for regional energy infrastructure, extending beyond a temporary or time‑bound disruption to shipping through the Strait of Hormuz.

Related to this is the evolving narrative around the objectives and duration of US and Israeli involvement. Recent communications from the administration have suggested that planned military actions may be limited in scope and duration. However, timelines in geopolitical conflicts tend to shift. A more prolonged engagement would increase the likelihood of sustained pressure on energy prices, raising the risk of broader spillovers.

Thus far, market reactions have remained contained to energy markets and assets exposed through the inflation channel. A prolonged period of elevated energy prices, however, could begin to weigh on the growth outlook and dampen consumer sentiment. To date, there is limited evidence that this is taking hold. That said, upcoming midterm elections add another layer of complexity, as affordability concerns are already emerging as a central theme and may influence policy decisions.

Stay the course

Our investment team stands ready to act should meaningful dislocations emerge, but our primary focus remains on delivering dependable long-term investment outcomes across our strategies.

Risk assets have enjoyed a strong run over the past three years. Against this backdrop, our portfolios are allocated to areas of the market where less optimistic scenarios are reflected in prices.

History suggests that remaining disciplined — especially during periods of heightened uncertainty — has been a sound approach through volatility and beyond.

Adviser-to-client template: Why diversification still matters

For financial advisers to use with clients.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

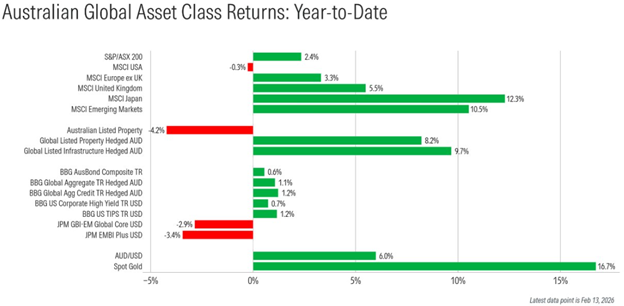

In any given year, different assets and different share markets can move in very different directions. This year has been a good reminder of why spreading your investments, also known as diversification, is so important.

As you can see below, while 2026 has seen U.S. share market deliver a negative return so far, many other markets around the world have performed extremely well. This mix of results is normal, and it highlights why relying too heavily on one market, asset or type of company can add unnecessary risk to a portfolio.

Source: Clearnomics, MSCI, Bloomberg, JP Morgan

A large part of the recent ups and downs in the US market has come from a small group of very large and very expensive U.S. technology companies. These companies have had a huge influence on U.S market movements simply because they make up such a big portion of the U.S. market. This can sometimes even spill over to markets outside of the U.S., given how large and influential these stocks have become.

Your Morningstar portfolio has generally been less invested in these highly priced tech stocks. This isn’t because they don’t believe in their long‑term potential, but because they have been trading at very high valuations. When something is expensive, it often means lower future returns and higher risk of sharp price swings, which is what we have seen with these U.S. technology companies in recent times.

Periods like the one we’re seeing now show the benefit of a valuation‑driven approach to investing. This means investing more in areas that offer good long‑term value, and less in areas that look expensive. It’s a disciplined way of aiming to deliver steadier results over time, even when certain parts of the market are experiencing turbulence.

What do you need to do?

In short, nothing. A well-diversified, multi-asset portfolio that is anchored to investment fundamentals should help to smooth out some of the market volatility, and the team at Morningstar Investment Management have constructed your portfolio to do just that.

Of course, if you still wish to talk through how your portfolio is designed to weather turbulence, or have any other questions about your financial plan, I’m always happy to help. Please feel free to reach out at any time.

From the desk of the CIO: Disruption in the age of AI

Key points

AI fears as new tools are released

The Morningstar moat framework is still vital

Emerging markets are showing more opportunities than developed markets

Investors continue to enjoy gains as markets move higher, with unfashionable countries and sectors outperforming and highly speculative assets like crypto falling sharply. The contrarian exposures in Morningstar portfolios have boosted client returns, with large gains in Brazil and Korea while Consumer Staples and UK equities also performed well.

What makes this year different from 2025 is how AI is impacting markets. A sell off in large AI hyperscalers has spread to software companies and more recently to highly profitable service industries. Behind the plunge are two fears about Artificial Intelligence, sparked by releases of better AI tools.

The first fear is that really big AI investments simply won’t pay off, as ever larger sums of capital are committed. Current estimates are close to $700bn just from Alphabet, Microsoft, Meta and Amazon. We do expect a sharp rise in AI related revenues from this spend, but there is considerable uncertainty and a risk that companies fail to execute.

The second fear is that AI will eliminate the competitive edge and profitability of service companies, especially highly valued oligopolies, if users can access new tools and data directly. So what should investors make of this?

Prior to this selloff, our view was that valuation levels of US technology stocks were unattractive versus most other industries and comparables outside the US, because share prices had outpaced their earnings growth. For these reasons, we held less US IT stock exposure than usual. Where we did own technology stocks, our positions were biased to hardware beneficiaries, such as Samsung and SK Hynix, whose earnings are directly linked to the increased AI spending, and firms like Google and Meta, which are using AI to enhance ad revenue generation. We also saw better value in dominant IT franchises in China.

So far in 2026 we have seen technology share prices fall while other markets rally. Could this now be a buying opportunity? For us, the real question is whether AI spend and its impact on competition will lead to much lower or less certain profitability and a lower “fair value”.

To answer that question we use the Morningstar moat framework to assess how AI might impact businesses. The moat concept popularised by Warren Buffett applies the idea that firms can erect competitive barriers that enhance profitability and growth by making it much harder for others to take their clients. Companies with “wide moats” are worth more than those with “narrow” or “no moats”. Morningstar Equity Research analysts base their moat ratings on 5 factors: Switching Costs; Network Effects; Intangible Assets; Cost Advantages; and Efficient Scale. Overall the broader sell-off looks overdone for companies with strong competitive advantages.

There is more of a question about the growing AI spend, its scope to push up costs and how revenues can rise enough whether by raising prices, taking market share or creating new markets. Faced with this uncertainty, we still favour other opportunities given current share prices.

For example, emerging market equities and bonds still offer better risk adjusted potential returns than developed countries, with the exception of the UK. Many emerging market countries no longer look like poorly managed, heavily indebted and politically volatile versions of developed countries. Instead, they have demonstrated greater fiscal discipline in terms of deficits and balance sheets. Their central banks have done a better job in containing inflationary pressures. Policymaking has been more predictable and transparent than the US, in many cases. There remain unique risks but at today’s prices investors are well compensated. Meanwhile global investors have large US asset exposures and are actively seeking to diversify into other sectors, currencies and geographies.

Disruption is certainly real and it includes not just the impact of AI. It also extends to re-examining the difference between emerging and developed countries and how much to hold in portfolios. We remain overweight in emerging market assets.

Use this simple trick to uncover your real financial goals

Our research shows that referring to a master list of financial goals can fine-tune your money priorities.

By Samantha Lamas and Ryan O. Murphy

What are your top investing goals? Behavioral science research suggests we tend to answer that question with whatever is on our minds at the moment, even if they’re not our true long-term financial goals.

If you recently saw a friend’s photos from Thailand, it might make you think your goal is to take epic vacations. If you went to a housewarming party last week, it could make you think you want to buy a new house. In reality, maybe you care more about leaving an inheritance to loved ones and charities. Or traveling the country in an RV. It’s not that you’re being insincere or that you don’t want to travel or get a house, but what’s easiest to recall can skew your true priorities.

Why is it important to uncover your true financial goals?

Goals chosen on impulse could lead to financial plans that don’t accurately represent what you value and desire. It’s your real goals that should guide your plan. That, in turn, can increase utility-adjusted wealth, according to financial analyst David Blanchett, previously at Morningstar. He compared a naive saving strategy of only focusing on saving for retirement with a goals-based approach that determined the ideal way to fund various goals based on your preferences and priorities. This approach can motivate you to stay on track. So, if you want to prioritize leaving money to loved ones and charities, you might decrease your spending rate in retirement to make sure you have enough money left over. If you value travel, you may be better off filling your short-term savings bucket. If you would rather buy a house, then those short-term savings can be allocated to a down-payment fund.

Whatever your goals and priorities are, having a clear idea of what you want can help you decide how to save and invest.

A simple method to identify your financial goals

First, write down your top three investing goals.

Most important

Second most important

Third most important

Next, check out the list of common investing goals below. Write down the ones that weren’t on your first list.

To be better off than my peers

To pay for personal self-improvement (go back to school, learn a skill, and so on)

To experience the excitement of investing

To start a business

To buy a house

To help pay for my kids’ college education

To stop working and do something I love

To go on a dream vacation

To relocate in retirement

To care for my aging parents

To give to charity or other causes I care about

To feel secure about my finances in retirement

To feel secure about my finances now

To leave an inheritance to my loved ones

To retire early

To pay for future medical expenses

To not be a financial burden to my family as I grow older

To manage my debt

Then, review your initial goals in step 1, consider the new goals you found in step 2, and write down your new roster of top three goals. Have your priorities changed?

If they have, you’re not alone.

How to motivate yourself to achieve your financial goals

In a study by Morningstar, our researchers tested those two ways of asking people about their goals: List your top three, then reassess after looking at the common goals, aka a master list.

In Morningstar’s study, 73% of people changed at least one of their top goals, and for many, their final list was quite different. Some people who initially thought in broad, vague terms came up with goals that were more specific and vivid. For example, they went from “retirement” to “feel secure about my finances in retirement.” “Retirement” doesn’t provide much direction or depth, but the revised goal is detailed and distinct.

The master list also helped many participants reframe their goals in terms of emotional and personal value. For example, a goal like “incidentals” became “to not be a financial burden to my family as I grow older.” That investor initially focused only on financial outcomes, which tend to be impersonal and potentially unmotivating (Locke et al. 1990).

So, when it’s time to figure out your financial direction, use a master list. This simple behavioral science tool can help you zero in on your true goals, not just the ones that are top of mind. Our report on the study includes a worksheet that takes you through the goals exercise.

This document is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear Client,

I know we say it every year, but 2025 went quickly! I hope you were able to take some time off and spend it with your loved ones before we get started in 2026. Last year was often tumultuous in markets, but as a result, it also proved many time-tested investing principles: to keep a cool head, to stay invested, and to always concentrate on an investment’s value over price. Our investment manager, Morningstar, will continue using this playbook, staying focused on the building blocks of investing.

So far, 2026 has started similarly to 2025, with the U.S. government delivering some policy decisions that have shocked markets. You’ve likely heard of many of these, including direct interventions in the defence, finance, homebuilding and mortgage industries, as well as orchestrating a regime change in Venezuela. That, plus outright attacks on Jerome Powelll, the chairman of the U.S. Federal Reserve, could all go some way to erode investor sentiment. That said, by sticking to a robust investment process and adhering to behavioural investing principles, investors can expect to navigate through this period, and periods of similar uncertainty, with confidence.

AI was also a big player in 2025, and we expect that to continue as 2026 unfolds. Morningstar’s investment team have considered how it will impact the broader economy, and expect that increased AI spending will go some way to dampening inflation, as more widespread use increases productivity and reduces costs. It’s also interesting to note parallels with the internet commerce boom of the late 1990s, which saw strong results in bonds.

And though we can’t predict exactly what curveballs 2026 will send our way, we do know that volatility is a feature, not a bug, of investing. As always, the best way to prepare is to stick with the fundamentals and tune out the noise. And, with Morningstar’s proven process, your investments are in good hands.

To that end, it would be remiss of me not to mention that Morningstar Investment Management took out two awards at the Financial Newswire Fund Manager of the Year Awards last year, and were highly commended for two more. It’s a pleasure to work with them, and if you have any questions about your portfolios, I’d be happy to answer them. For more details, refer to this article.

As the new year starts, it’s always a great time to talk about or revise your financial plan. Please feel free to reach out any time and we’ll get something on the calendar. I look forward to speaking soon.

Regards,

Adviser

Important Information

As noted previously, this document is intended to support your service proposition to clients and the commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use

Don’t Let Risk Misperceptions Cloud Your Clients’ Portfolios

By Nicki Potts and Dr. Danielle Labotka

Build knowledge and confidence to guard against the jitters.

Have you ever had a client who unexpectedly loses their nerve amid jittery markets? It’s not uncommon to see clients whose risk tolerance suggests they should be able to withstand the fluctuation in their portfolio react with a much more conservative risk tolerance. Has your risk tolerance questionnaire failed?

The culprit may not be your clients’ risk tolerance at all but rather their risk perception. Risk tolerance is an enduring psychological trait that reflects how we feel emotionally about taking risks. Risk tolerance does not tend to change, even as we transition through life stages and market cycles. Risk perception, on the other hand, is our cognitive appraisal of a given risk. Whereas risk tolerance guides how we respond to risk, risk perception determines how risky we find something in the first place. Unlike risk tolerance, risk perception can be quite fickle.

Advisers are no strangers to handling risk tolerance; good financial planning is built on balancing a client’s risk tolerance with their capacity and needs. However, advisers also need to learn how to manage their clients’ perception of risk to keep them on track. Left unchecked, poorly calibrated risk perception may lead to suboptimal behaviors both in good times (chasing returns) and bad (panic selling).

Risk perception can be challenging to manage, as it’s influenced by many external and internal factors (even cloudy weather!). Nonetheless, advisers can help clients better evaluate risk by building a solid foundation based on context, expectations, and confidence.

Defuse the Unknown by Putting Risk Into Context

It’s natural to fear the unknown, as we tend to fill in gaps in our knowledge with worst-case scenarios, making us believe something to be riskier than it is. For many everyday investors, one of the biggest determinants of how risky they perceive an investment is how familiar they are with the product in the first place. However, market volatility may affect clients’ perception of risk regardless of their familiarity with their investments. As market volatility is inherently unpredictable, it can foster feelings of dread over losing money, which can lead clients to evaluate an investment as riskier than they typically would.

Though advisers cannot control market volatility, they can educate their clients on their investments to defuse the fear of the unknown. Educating clients means not only ensuring they understand how various investment vehicles work but also what volatility means for them. Clients’ plans are built with their goals and accepted risk strategies in mind. Therefore, advisers can help clients contextualize any proposed actions in response to uncertainty by evaluating them from the standpoint of “Is this consistent with the plan we’ve agreed to?” This context can help clients anchor back on their goals, stick with their commitments, and feel confident that their plan is tailored to get them where they want to be.

Although clients can recalibrate their risk perception amid volatility, it is best to prepare them beforehand. If your clients often react adversely to market volatility, they are likely surprised. This means their expectations for what risk should look like do not align with their reality.

You can minimize risk misalignment during uncertain times by building a solid understanding of investment risk from the get-go. Clients will particularly benefit from understanding the relationship between risk and return and the range and likelihood of possible outcomes (including the possibility of extreme events). Start with a robust, stable risk tolerance measure to determine how much risk your clients are comfortable taking and are willing to accept in pursuit of their goals, while attending to their risk capacity. Then, illustrate, explore, and test the reasonableness of clients’ expectations against historical performance to identify gaps. Check in periodically with clients to manage creeping expectations and further consolidate understanding.

Risk perception can be affected by the knowledge, context, and expectations your clients have, especially when markets are in turmoil. Advisers are well-placed to arm clients with the framework they need to appropriately evaluate risk.

Improve Risk Calibration by Building and Managing Confidence

Education is the first step to helping clients better evaluate risk, but confidence also plays an important role in our judgment of risk. Clients who have confidence in their plan, their adviser, and their own knowledge will be better able to manage their risk perception. As outlined above, education helps build trust in an adviser’s expertise, making clients confident they can rely on their adviser’s guidance. Just as advisers benefit from continuing professional development, clients can fine-tune their risk assessments and improve their confidence through continued structured learning, guidance, and support.

However, advisers must also help clients recognize when overconfidence may lead their risk perception astray. In particular, cognitive biases may make us feel more confident in our conclusions than warranted. For example, a common mental shortcut is the availability heuristic, where we draw conclusions based on familiar or readily available information. That can be helpful but can also inflate our confidence. When headlines, influencers, friends, and family are feeding us the same message, we tend to forget or ignore contradictory information.

Clients may rely on numerous shortcuts when forming judgments, and advisers cannot expect to identify and provide guidance on every occasion. Instead, advisers can help their clients craft a set of decision rules they can rely on when making risk judgments to help combat overconfidence that may come from mental shortcuts. For example:

Is this information from a reliable source?

Is it supported by objective evidence?

Are there counterarguments? What are they?

Am I in the right emotional state to make decisions?

What is the likely impact on my strategy and goals?

The objective is to equip clients with tools and processes to readily make informed judgments and recognize when bias may be at play. This will help clients combat the false confidence that cognitive biases can bring and help them come back to the fundamentals of their education, where true confidence should live.

Market sentiment can affect your clients’ perception of risk in their portfolio; in turn, this can make them want to make changes to their investment strategy. But investment strategy changes should be driven by changes in things such as goals and circumstances, not market sentiment. When clients’ risk perceptions are miscalibrated, advisers should provide them with the education and confidence they need to realign their perceptions with reality. Managing clients’ knowledge, expectations, and confidence sets them up to make informed risk choices.

Though 2025 threw many challenges at investors, the great news is that it also brought many closer to reaching their goals by delivering unusually high returns. This is to be celebrated, especially as investors were tested in March as markets sold off. Staying the course by remaining invested, focusing on goals rather than media headlines, and responding to value proved the most effective way to deal with the shocks and volatility. We expect that tried-and-tested playbook to be just as effective this year.

Coping with whatever 2026 brings will require investors to know what to respond to, by staying focused on the building blocks of investing: fundamentals, probabilities and valuation. Questions to ask as conditions change include: how much will the new information really impact asset cashflows, relative to other factors that also matter? How will it change the range of scenarios and how likely they are to occur? Is the news already priced in or has there been an under or overreaction?

Last year, this approach added a lot of value. In our Morningstar managed portfolios and funds, we bought equities and sold bonds in early April as we assessed that equities were oversold on the Tariff Day news. Later in the year, we added to healthcare stocks after fears rose of adverse regulation, and we took profits in utility companies after the AI-led surge. We also added to Korean equities in the wake of the tariff fears, at very low prices.

In many ways 2026 has started out just like 2025 – a barrage of policy shocks driven by the US government. These include direct interventions in the defence, finance, homebuilding and mortgage industries, plus regime change in Venezuela. Most high profile of all is the outright attack on the chairman of the US central bank. This could erode trust and signal that much lower interest rates lie ahead, but many other factors will also play a role in driving outcomes.

We expect AI to continue playing a big role in 2026, in terms of economic, company and market behaviour. We have revised our US GDP growth forecasts on the back of increased investment spending and expect AI to dampen inflation, as adoption enhances productivity and reduces costs. There is a parallel with the growth in internet commerce that took off in the late 1990s, which was a boon for bonds.

We have also revised our fair value estimates for major corporate players including Alphabet, Nvidia, Broadcom and Apple, which benefit from the surge in spending or improvements in their own capabilities. There are also big beneficiaries outside the US such as Samsung and SK Hynix, both running in the global race to achieve AI superiority. Delivering mas sive sales and profits, they are priced more conservatively than their US counterparts.

One headwind for investors is that more optimism is embedded in share and corporate bond prices, after the rally of the past 12 months. We think returns will inevitably be lower in 2026 but can be boosted by more active than passive opportunities that look beyond major markets and industries.

Morningstar Investment Management’s fundamental, long-term approach takes a rational approach in the face of volatility and unpredictable market movements, knowing that the only thing we can trust in markets is that turbulence is a given. Ultimately, 2025 was a testament to the core principles of investing, and we expect these methods to continue holding investors in great stead in 2026.